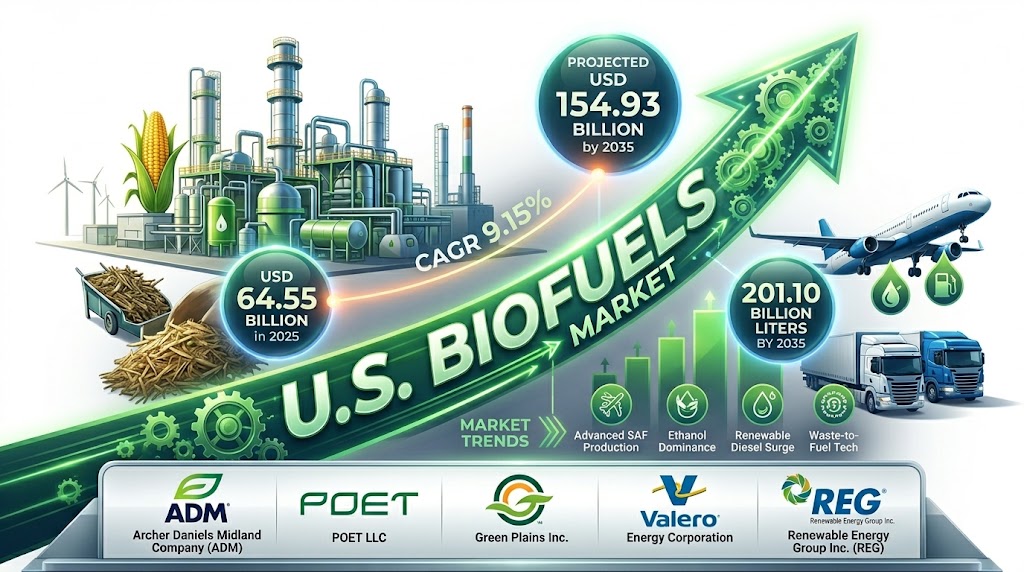

The United States energy sector is undergoing a rapid transition toward low-carbon fuels, driven by industrial decarbonization and federal energy security mandates. Market data places the baseline U.S. biofuels market size at USD 64.55 billion in 2025. Propelled by federal initiatives and a surge in the domestic production of drop-in renewable diesel and sustainable aviation fuel (SAF), the market is projected to grow from USD 70.46 billion in 2026 to USD 154.93 billion by 2035. This represents a steady CAGR of 9.15% in revenue.

In terms of physical production volume, the industry is projected to expand from 89.85 billion liters in 2025 to 201.10 billion liters by 2035, exhibiting a volume CAGR of 8.39%. This massive scaling is accompanied by an average manufacturing price of USD 0.89 per liter against an average selling price of USD 1.26 per liter in 2025, with a pricing CAGR projected at 4.88% through 2035.

Market Overview & Dynamics

Why Is The U.S. Biofuels Market Important?

Biofuels derived from agricultural feedstocks, waste biomass, and algae serve as a crucial lever for reducing liquid fossil fuel dependence and lowering greenhouse gas emissions across difficult-to-electrify transport sectors. The strategic significance of this market rests on its immediate compatibility with existing internal combustion infrastructure.

Unlike complete vehicle electrification, which requires an entirely new charging infrastructure, drop-in biofuels like renewable diesel and SAF utilize existing pipelines, fuel terminals, and engine systems without modification. Backed by federal mandates like the Environmental Protection Agency’s (EPA) Renewable Fuel Standard (RFS) and regional low-carbon fuel standards, biofuels act as an immediate bridge to help the transport, aviation, and manufacturing sectors meet their near-term decarbonization targets.

What Are the Key Factors Driving The Market?

The structural expansion of this sector is propelled by three primary drivers:

-

Favorable Federal Policy and Tax Incentives: Structural frameworks like the Inflation Reduction Act (IRA) provide substantial blender’s credits and clean fuel production incentives (§45Z) tied directly to a fuel’s carbon intensity (CI) score.

-

Decarbonization Mandates in Heavy Transport: Commercial shipping, logistics fleets, and legacy rail systems are turning to high-blend biodiesel and renewable diesel to satisfy corporate ESG metrics.

-

The Commercial Scaling of Next-Gen Feedstocks: Rapid technical advancements in processing non-food cellulosic residues and waste oils allow producers to scale output while avoiding direct competition with food crops.

What Are the Key Market Trends & Technological Shifts?

The domestic biofuel industry is shifting away from simple first-generation processing toward highly efficient, multi-feedstock biorefineries.

-

Transition to Advanced & Cellulosic Biofuels: Manufacturers are increasingly utilizing advanced enzymes and catalytic upgrading technologies to efficiently break down lignocellulosic biomass, such as corn stover and wood residues, into ultra-low-carbon intensity fuels.

-

The Sustainable Aviation Fuel (SAF) Infrastructure Boom: Driven by the federal SAF Grand Challenge—which targets 3 billion gallons of domestic SAF production by 2030—energy companies are heavily investing in alcohol-to-jet (ATJ) and hydroprocessed esters and fatty acids (HEFA) processing lines.

-

AI Integration and Agricultural Bio-Engineering: Artificial intelligence is being deployed to optimize real-time fermentation kinetics and streamline supply chain logistics. Concurrently, genetic engineering is introducing novel concepts, such as scientists modifying Camelina sativa to serve as a hyperaccumulator of nickel for phytomining while simultaneously producing low-CI biofuel feedstocks.

Trade, Value Chain, & Data Presentations

What Does the U.S. Biofuel Trade Flux Indicate?

Customs and trade lane data reveal that the United States maintains a strong position in global energy trade. U.S. biofuel exports reached an annual valuation of USD 5.13 billion, moving 606,484 metric tons of product. In terms of support infrastructure, the U.S. exported 188 shipments of fuel dispensing equipment (primarily to India, Mexico, and Costa Rica) alongside 69 shipments of industrial fuel components.

A historical look at the 2022 baseline highlights the sheer scale of domestic fuel operations: fuel ethanol led the market with 15.36 billion gallons produced and 14.02 billion gallons consumed internally, while biodiesel and renewable diesel together contributed over 3.1 billion gallons to the domestic fuel supply.

Key Market Data Summary

The following table summarizes the core metrics defining the U.S. biofuels industry over the coming decade:

| Report Attribute | Baseline & Forecast Metrics |

| 2025 Base Year Value | USD 64.55 Billion / 89.85 Billion Liters |

| 2026 Market Size Value | USD 70.46 Billion / 97.39 Billion Liters |

| 2035 Projected Revenue | USD 154.93 Billion / 201.10 Billion Liters |

| Market Revenue CAGR | 9.15% (2026 – 2035) |

| Average Selling Price (2025) | USD 1.26 per Liter (4.88% Pricing CAGR) |

| Dominant Application (2025) | Transportation Fleet Blending (57% Share) |

What Is the Biofuels Regulatory Landscape?

The biofuels market operates under a complex matrix of federal oversight and state-level incentives that govern compliance and credit values.

| Regulatory Body / Agency | Key Enacted Programs | Core Focus Areas & Market Impact |

| U.S. EPA | Renewable Fuel Standard (RFS), Clean Air Act | Mandates annual Renewable Volume Obligations (RVOs) and manages the generation and trading of RIN credits. |

| U.S. Department of Energy (DOE) | Bioenergy Technologies Office (BETO) | Directs R&D funding for advanced algae-based, lignocellulosic, and waste-to-fuel commercial demonstration projects. |

| U.S. Department of Agriculture (USDA) | Rural Energy for America (REAP), BioPreferred | Provides grants and loan guarantees for rural biorefineries and supports domestic feedstock cultivation. |

| IRS / Dept. of the Treasury | Inflation Reduction Act (IRA) Credits | Manages the §45Z Clean Fuel Production Credit, tying tax incentive values directly to lifecycle GHG reduction scores. |

| Federal Aviation Administration (FAA) | SAF Grand Challenge, ASCENT | Coordinates with the DOE and EPA to certify novel aviation fuel pathways under ASTM D7566 requirements. |

| California Air Resources Board (CARB) | Low Carbon Fuel Standard (LCFS) | Establishes market mechanisms that reward low carbon intensity fuels, a model adopted by Washington and Oregon. |

Segmental Insights

Why Did the Ethanol Segment Dominate Product Markets in 2025?

The ethanol segment led product markets in 2025, commanding a 28% revenue share. This dominant position is primarily due to the widespread use of E10 blends (10% ethanol and 90% gasoline) as a standard automotive fuel across the United States. Produced at scale from corn feedstocks, ethanol serves as an affordable octane booster that significantly lowers lifecycle tailpipe emissions. The infrastructure for corn ethanol is highly mature, supported by extensive midwestern refining networks and long-standing federal blending mandates.

At the same time, the biodiesel (20% share) and green/renewable diesel (21% share) segments are growing rapidly due to rising demand for drop-in replacements for petroleum diesel in commercial transport and logistics fleets. In contrast, solid biomass alternatives like wood pellets (8% share) are carving out a steady, specialized niche, growing at a projected 4.65% CAGR as a carbon-neutral heating fuel for industrial applications and residential energy generation.

Which Feedstock Segment Formed the Foundation of the Industry?

The corn and sugarcane segment dominated feedstock markets, capturing 49% of total revenue in 2025. This large share is sustained by the massive scale of U.S. corn production, which provides a steady, high-yielding sugar source for automated industrial fermentation.

Concurrently, the waste oils and fats segment has reached a 27% market share, driven by its low carbon intensity scores under LCFS frameworks, which makes it a highly attractive feedstock for renewable diesel and SAF. To ensure long-term market growth without competing for agricultural land, the cellulosic material segment (16% share) and next-generation algae segment (8% share) are receiving substantial federal R&D funding, positioning them as essential feedstocks for future aviation and marine fuels.

What Are the Market’s Recent Government Initiatives?

Recent federal and state policy shifts are designed to accelerate the commercialization of ultra-low-carbon fuels:

-

The RFS Volume Adjustments: The EPA’s updated multi-year Renewable Volume Obligations (RVOs) establish clear, expanding blending quotas for advanced and cellulosic categories, providing long-term market certainty for project investors.

-

The Transition to §45Z Clean Fuel Production Credits: Administered by the IRS, this structural shift rewards domestic producers by tying financial incentives directly to verified reductions in a fuel’s lifecycle carbon intensity.

-

State-Level Clean Fuel Expansion: The adoption of Low Carbon Fuel Standards across western and northeastern states has created high-value regional markets, accelerating investments in specialized renewable natural gas (RNG) and waste-to-fuel production plants.

Competitive Landscape: Top Companies Profiled

Green Plains Inc.

-

About: Based in Omaha, Nebraska, Green Plains Inc. is a leading industrial biorefining enterprise operating automated production plants across the U.S. Midwest.

-

Products: Focuses on low-carbon ethanol, high-protein animal feed ingredients, and renewable corn oil. To optimize its supply chain efficiency, Green Plains selected Eco-Energy LLC in April 2025 as its exclusive marketing and logistics partner.

-

Financial Profile: Publicly traded; a key player driving low-carbon intensity fuel innovations.

POET LLC

-

About: Headquartered in Sioux Falls, South Dakota, POET stands as the world’s largest producer of bioethanol, operating an extensive, highly integrated network of biorefineries.

-

Products: Produces large volumes of fuel-grade ethanol, proprietary Dakota Gold® distillers grains, and specialized JIVE® asphalt rejuvenators derived from renewable corn oil.

-

Financial Profile: Privately held corporation; handles significant shares of domestic agricultural processing.

Archer Daniels Midland Company (ADM)

-

About: A global food processing and agricultural commodities giant based in Chicago, Illinois, with a deep footprint in renewable fuel production.

-

Products: Operates industrial-scale wet and dry corn milling complexes that produce fuel ethanol, biodiesel, and sustainable agricultural feedstocks.

-

Financial Profile: Publicly traded (NYSE: ADM); heavily invested in advanced carbon capture and storage (CCS) systems to lower its lifecycle fuel emissions.

Gevo Inc.

-

About: An advanced renewable fuels innovator headquartered in Englewood, Colorado, that specializes in low-carbon technology pathways.

-

Products: Utilizes advanced fermentation and alcohol-to-jet (ATJ) conversion technologies to produce commercial-grade sustainable aviation fuel (SAF), isobutanol, and renewable premium gasoline.

-

Financial Profile: Publicly traded (NASDAQ: GEVO); integrates renewable energy and carbon capture directly into its production processes.

What Is the Future of the Market?

The future of U.S. biofuels will be defined by the widespread commercialization of sustainable aviation fuel (SAF) and the integration of carbon capture technologies into existing biorefineries. Over the next decade, first-generation ethanol facilities will increasingly transition into zero-emission manufacturing platforms by routing their fermentation biogenic $CO_2$ streams directly into deep-well underground geological storage.

As commercial airlines scale up their use of SAF to meet binding net-zero targets, demand for low-CI waste feedstocks and advanced alcohol-to-jet processing will rise significantly. This shift will ensure that biofuels remain a cornerstone of the U.S. energy landscape through 2035, serving as a vital complement to the broader transition toward electrification.

Single Relevant Follow-Up Question

Would you like to expand this analysis to include a detailed forecast of the U.S. Sustainable Aviation Fuel (SAF) production capacity upgrades, or should we examine the financial impact of the §45Z tax credit structure on biorefinery profit margins?

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Leave a Reply