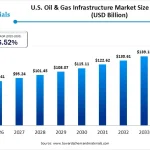

The U.S. oil & gas market size is valued at USD 149.81 billion in 2026 and is structurally projected to reach USD 224.94 billion by 2035, expanding at a Compounded Annual Growth Rate (CAGR) of 4.62% during this forecast period.

In terms of physical output volume, the market is positioned to scale from 47.55 billion barrels of oil equivalent (BOE) to 61.05 billion BOE by 2035, demonstrating a volume-based CAGR of 2.53%. This variance between value and volume expansion reflects structural efficiencies, higher-value downstream asset conversion, and a premium placed on export-ready Liquefied Natural Gas (LNG) infrastructure.

Market Overview: Why is the U.S. Oil & Gas Market Important?

The U.S. hydrocarbon sector serves as an indispensable pillar of both global energy architecture and domestic macroeconomic stability. Its importance can be viewed through three distinct dimensions:

-

Geopolitical & Energy Independence: Over the past decade, advancements across major basins have transformed the U.S. from a net energy importer into a dominant global exporter of crude petroleum and natural gas. This reduces domestic exposure to volatile foreign supply chokepoints.

-

Industrial Feedstock Security: Beyond power generation, the sector acts as the primary feed provider for advanced chemical manufacturing, electronics, automotive components, and industrial infrastructure.

-

Economic Multiplying Effect: The industry drives hundreds of billions of dollars in capital expenditure, generates extensive corporate and property tax revenues for regional economies, and supports deep labor markets across upstream engineering, midstream logistics, and specialized field services.

Market Dynamics: What Are the Key Factors Driving the Market?

1. What is Market Growth and Its Core Velocity?

The market’s momentum is driven by a combination of recovering industrial baseloads, a rapid expansion in data center electricity demand, and structural growth in the heavy transport sector. High-density compute clusters and logistics networks require dependable, dispatchable energy, solidifying natural gas as a critical component of the power grid alongside rising renewable integration.

2. Growing Petrochemical Infrastructure

The relationship between upstream wet gas extraction and midstream chemical manufacturing has reached unprecedented integration. Sustained access to low-cost ethane and propane from domestic shale formations has prompted heavy investment along the U.S. Gulf Coast. The expansion of these multi-billion-dollar cracking facilities drives continuous, high-volume demand for natural gas and natural gas liquids (NGLs).

3. Technological Advancements & AI Integration

The contemporary oilfield is defined by digital transformation. The industry is rapidly adopting high-performance computing, artificial intelligence, and predictive maintenance protocols. These tech layers minimize unscheduled downtime, optimize subterranean reservoir targeting, and improve drilling precision—significantly lowering lifting costs per barrel.

What Are the Key Market Trends Shifting the Industry?

Accelerated LNG Export Infrastructure

The reconfiguration of global trade lanes has turned LNG exports into a critical growth segment. Driven by international demand for secure, lower-emission transitional fuels, the U.S. has scaled up its liquefaction facilities and maritime export terminals.

Unconventional & Deepwater Extraction Synergies

While onshore multi-stage hydraulic fracturing across major shale plays accounts for the majority of domestic production, operators are increasingly focusing on offshore assets. Advancements in subsea robotics, ultra-deepwater pressure management, and real-time reservoir modeling are driving a major resurgence in Gulf of Mexico exploration.

What Are the Market’s Recent Government Initiatives?

Regulatory frameworks are shifting from restrictive mandates toward market-incentivized compliance and asset integrity management:

-

Federal Bureau of Land Management (BLM) Lease Sales: In mid-2025, the BLM launched historic oil lease sales in the eastern U.S., opening up fresh geographical acreage in the Appalachian Basin and Southeastern states. This provides proximity to major eastern refining centers.

-

Standardization of Abandoned Well Management: Regulatory focus has intensified around legacy assets. In early 2025, new structural insurance mechanisms were commercialized to systematically plug abandoned wells, allowing operators to generate verifiable carbon credits and offset environmental liabilities.

-

Infrastructure Permitting Reforms: Federal support for natural gas transmission lines and cross-state compression stations has streamlined midstream approvals, directly supporting regional volume expansion.

Market Disruption: Challenges & Production Constraints

Despite robust growth markers, the U.S. market faces complex, structural cost hurdles:

The Cost Challenge: High lifting and production costs remain a primary barrier to unrestricted expansion.

The structural complexity of multi-stage horizontal drilling requires significant upfront capital. Furthermore, modern environmental guidelines require sophisticated, capital-intensive water management systems to process, recycle, and safely dispose of large volumes of co-produced oilfield wastewater. Accessing remote or environmentally sensitive geographies also incurs premium logistics expenses, compressing corporate margins during downward commodity price cycles.

What Are the Benefits of Utilizing Advanced Upstream & Midstream Systems?

Transitioning traditional extraction assets to modern, digitally integrated systems yields immediate operational returns:

-

Enhanced Recovery Rates: Advanced horizontal completion techniques yield higher initial production rates and extend the lifecycle of mature wells.

-

Reduced Carbon Intensity: Real-time AI monitoring enables early leak detection, lowering fugitive methane emissions across expansive pipeline infrastructure.

-

Optimized Resource Allocation: Predictive maintenance scheduling identifies downhole component fatigue before a failure occurs, keeping equipment running and preventing costly, emergency interventions.

Market Segments & Deep Portfolio Insights

The U.S. oil & gas landscape is diversified across several highly specialized segments, each showing distinct growth dynamics and capital allocations.

Which Segment Accounted for the Largest Market Share?

The Upstream segment held the dominant volume share at 44.47% in 2024, driven by aggressive multi-stage drilling in tier-one acreage. However, over the forecast period, the Midstream segment is projected to achieve the most rapid growth momentum, expanding at a 2.97% CAGR as digital pipeline networks, automated storage nodes, and new LNG export terminals come online.

Comprehensive Sector Allocations & Projections

The following structural data maps the expected volumetric changes across the primary segments of the hydrocarbon value chain:

| Segment Dimension | Volume Share 2024 (%) | Market Volume 2024 (Billion BOE) | Volume Share 2034 (%) | Market Volume 2034 (Billion BOE) | CAGR Projection (2025–2034) |

| Upstream (Exploration & Production) | 44.47% | 20.68 | 39.56% | 21.41 | 0.39% |

| Midstream (Pipelines, Storage, LNG) | 25.32% | 11.77 | 28.32% | 15.33 | 2.97% |

| Downstream (Refining & Marketing) | 30.21% | 14.05 | 32.12% | 17.38 | 2.40% |

| Total Ecosystem | 100.00% | 46.50 | 100.00% | 54.12 | 1.53% |

Granular Segment Insights

-

Regional Dominance: The South region maintains a dominant 51% market share, supported by the Permian Basin’s deep reserves and mature logistical links. Concurrently, the Northeast region is experiencing the fastest growth rate, driven by structural demand and ongoing development in the Marcellus and Utica shale plays.

-

Resource Focus: Natural Gas continues to hold the largest market share (54%), underpinned by extensive domestic utility frameworks. Conversely, Liquefied Natural Gas (LNG) is the fastest-growing sub-segment, driven by global export demand and international trade commitments.

-

Extraction Methodologies: Unconventional techniques (horizontal drilling and fracturing) comprise 65% of active operations. Meanwhile, Offshore deepwater projects represent the fastest-accelerating technical segment, supported by specialized deepwater policies and improved subsea infrastructure.

-

End-Use Profiles: The Transportation sector commands a 42% share of end-use consumption. However, the Petrochemical Feedstock segment is growing at the highest relative CAGR, driven by continuous corporate investment along the U.S. Gulf Coast.

-

Asset Deployment: The Permian Basin remains the largest single regional asset, controlling 44% of production value. The Marcellus Shale is growing at the fastest rate due to steady improvements in rig configuration and lateral drilling efficiencies.

-

Technology Layers: Hydraulic fracturing leads active technologies with a 41% share. However, AI & Predictive Maintenance applications are growing at the fastest rate as operators work to minimize operational downtime and reduce lifting costs.

Competitive Landscape: Top Market Leaders

The U.S. market is led by a mix of major integrated global corporations, nimble independent exploration and production (E&P) firms, and midstream logisticians.

ExxonMobil Corporation

-

About: Headquartered in Spring, Texas, ExxonMobil is one of the world’s largest publicly traded energy and chemical corporations, operating across the entire hydrocarbon value chain.

-

Products: Crude petroleum, natural gas, advanced petrochemical olefins, aromatics, performance polymers, and specialty lubricants.

-

Market Cap: ~USD 590 billion to 640 billion (varying by mid-2026 equity valuations).

Chevron Corporation

-

About: Based in San Ramon, California, Chevron runs extensive upstream and downstream operations, with a strong strategic focus on the Permian Basin and deepwater assets in the Gulf of Mexico.

-

Products: Liquefied natural gas, crude oil, diesel, aviation fuel, petrochemical additives, and low-carbon alternative fuels.

-

Market Cap: ~USD 350 billion to 375 billion (mid-2026 financial assessments).

ConocoPhillips

-

About: Operating as a pure-play independent upstream company, ConocoPhillips focuses on exploring and producing unconventional and conventional reservoirs globally.

-

Products: Unconventional tight oil, deepwater crude, pipeline-quality natural gas, and natural gas liquids (NGLs).

-

Market Cap: ~USD 136 billion.

Occidental Petroleum (Oxy)

-

About: An international energy company with major assets in the Permian Basin, Occidental is also a leader in carbon management and enhanced oil recovery (EOR) infrastructure.

-

Products: Permian crude oil, basic chemicals, vinyls, performance polymers, and carbon-capture engineering services.

-

Market Cap: ~USD 52 billion to 64 billion.

EOG Resources, Inc.

-

About: EOG is a major independent crude oil and natural gas exploration and production company focused on premium, low-cost domestic shale plays.

-

Products: Light sweet crude oil, condensate, natural gas liquids, and dry natural gas.

-

Market Cap: ~USD 77 billion.

What is the Future of the Market & Strategic Outlook?

The future of the U.S. oil & gas market will be defined by structural efficiency rather than simple volumetric expansion. Over the 2026–2035 forecast period, capital allocation will likely focus on asset digitization, automated production platforms, and zero-emission midstream logistics.

As international markets continue to prize low-carbon energy solutions, domestic producers who successfully integrate carbon capture, utilization, and storage (CCUS) into their operational models will be well-positioned to command a market premium. The structural resilience of the U.S. market, combined with its robust legal frameworks and world-class pipeline networks, ensures that the country will remain a cornerstone of global energy security for decades to come.

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Leave a Reply