Executive Summary

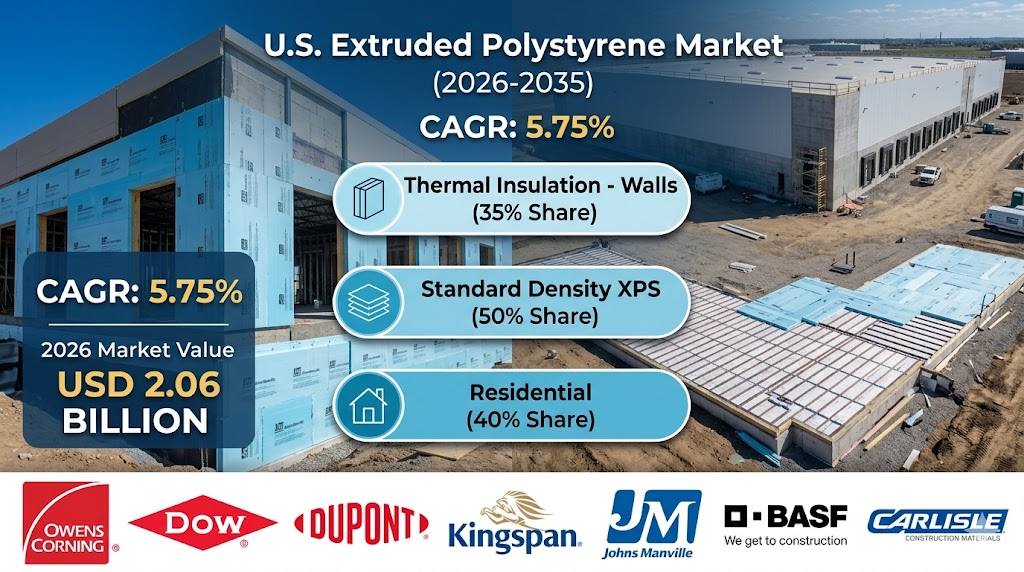

The United States extruded polystyrene (XPS) market is positioned for significant capital deployment. Driven by mandatory energy efficiency building updates and shifting dynamics in thermal preservation, the market reached a valuation of USD 2.06 billion in 2026, advancing from USD 1.95 billion in 2025. Extensive market tracking projects the market to climb to USD 3.41 billion by 2035. This trajectory mirrors a highly consistent Compound Annual Growth Rate (CAGR) of 5.75% over the 2025–2035 forecast matrix, heavily sustained by cold chain infrastructure development and standard building code modifications.

Market Overview: The Essential Polymer in Advanced Insulation

Extruded Polystyrene ($XPS$) represents a highly dense, rigid, closed-cell foam structural insulation. The material is chemically synthesized through a continuous extrusion process that yields an exceptional surface profile immune to moisture infiltration, boasting a high compressive structural threshold.

Why Is the Market Important?

In modern structural engineering, thermal containment and moisture control are vital parameters. XPS serves as a primary performance layer across building foundations, commercial green roofs, perimeter sub-grade walls, and structural insulated panels ($SIPs$) due to its resilience against water degradation. Furthermore, its high structural load capacity makes it critical for specialized deep-freeze warehouses and civil roadway beds exposed to sub-zero freeze-thaw degradation cycles.

Market Dynamics: Growth Accelerators and Functional Bottlenecks

What Are the Key Factors Driving the Market?

-

Expansion of Cold Chain Logistics Infrastructure: A rapid surge in temperature-controlled pharmaceutical storage and specialized food distribution centers has driven immediate volume demands for sub-floor XPS configurations.

-

The Proliferation of Green Building Standards: Tightening international energy codes ($IECC$) force commercial and residential property developers to specify superior insulation values to curb Scope 2 operational building emissions.

-

Innovations in Manufacturing Technologies: Advanced physical cell texturing improves long-term thermal resistance, promoting rapid industrial adoption over outdated composite foam variants.

What Are the Crucial Market Challenges?

The industry faces notable headwinds from alternative heavy-performance insulation substrates. High-density mineral wool and polyisocyanurate ($PIR$) deliver highly competitive alternative options in specialized applications due to their inherent fireproof superiority. Additionally, the premium initial raw material and installation costs associated with high-performance XPS foam boards can serve as a near-term capital barrier for lower-tier residential building contracts.

What Are the Key Market Trends?

-

Widespread Shift Toward Bio-Based and Recycled Formulations: Industry participants are actively allocating research capital to create biodegradable and bio-sourced expanded and extruded alternatives to satisfy state-level plastic usage restrictions.

-

The Surging Demand for High-Density Customization: Structural infrastructure projects increasingly mandate ultra-high compressive strength boards to secure longevity under heavy mechanical stresses, such as railway beds and foundation lines.

What Recent Government Initiatives Are Reshaping the Landscape?

Federal tax incentives—specifically designed around energy-efficient commercial building tax deductions and enhanced residential energy property credits—continue to reshape procurement patterns. State-mandated net-zero insulation requirements force the immediate replacement of degraded traditional building insulation materials with certified, low-emission XPS boards.

Segmental Insights: Analyzing Application, Density, and Thickness

Which Segment Accounted for the Largest Market Share?

The operational footprint of the U.S. extruded polystyrene market is segmented by technical application, density layer, thickness classification, and faced material type:

-

By Application: Thermal insulation for walls dominated the landscape in 2024 with a 35% market share, directly attributed to standard vertical structural envelope installations. Concurrently, the packaging segment is advancing at the fastest CAGR due to booming e-commerce transport requirements.

-

By Product Type: Standard density configurations accounted for a dominant 50% market share in 2024.

-

By Board Thickness: Medium boards (ranging between 1 to 2 inches) led structural procurement with a 45% market share.

Leave a Reply