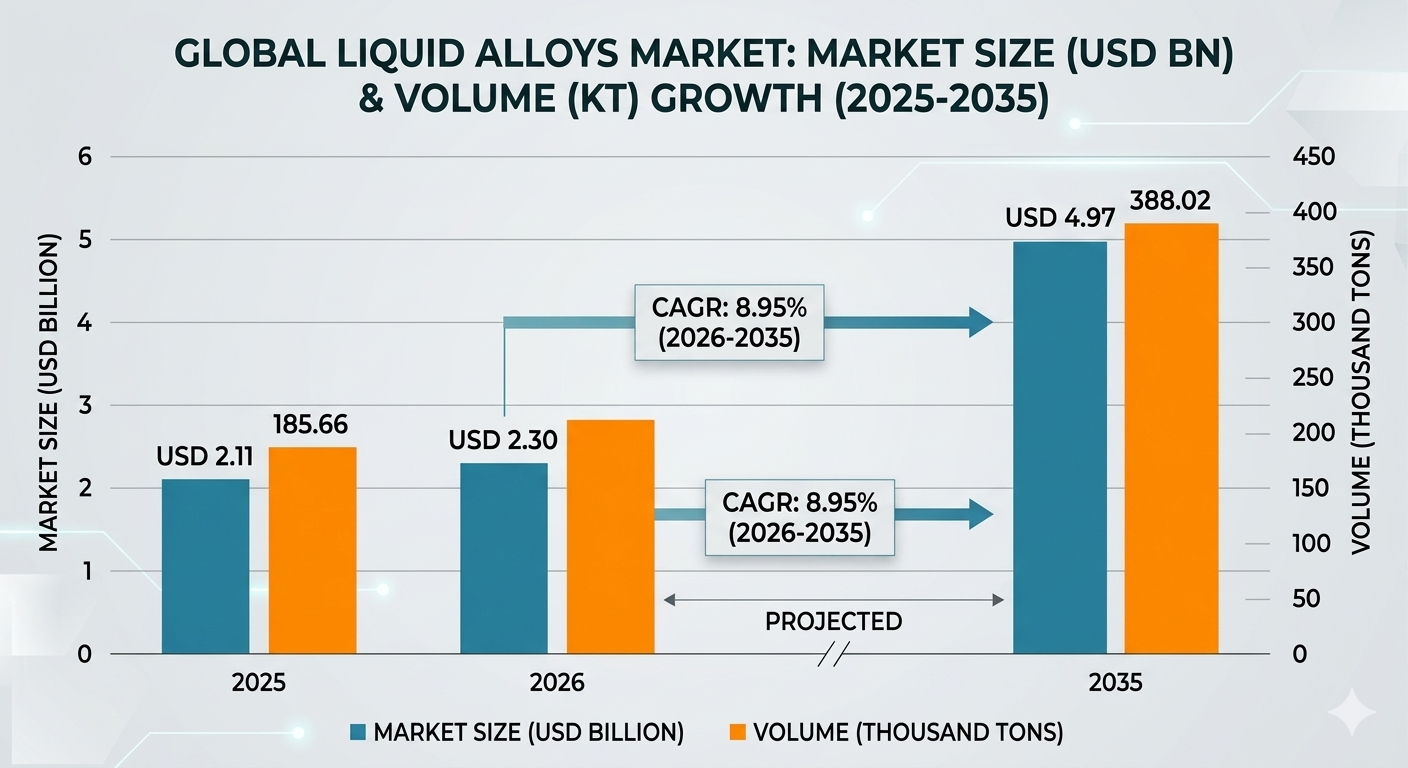

The global liquid alloys market is entering an era of unprecedented expansion, driven by the intense miniaturization of electronics and the demand for superior thermal regulation. Valued at USD 2.11 billion in 2025, the market is projected to surge to USD 4.97 billion by 2035, growing at a robust CAGR of 8.95%. While the market is set to reach approximately USD 3.65 billion by 2032, the long-term forecast through 2035 underscores the critical shift toward high-performance, safer metal technologies that replace legacy mercury-based components.

Market Overview

Why is the Liquid Alloys Market Important?

Liquid alloys represent a sophisticated frontier in materials science, engineered to maintain a fluid or semi-fluid state at significantly lower temperatures. These advanced materials—primarily composed of gallium, indium, tin, and bismuth—are pivotal in managing the extreme thermal challenges posed by modern, high-density computing and compact electronic designs. As industries move toward flexible, wearable, and high-performance technologies, liquid alloys have transitioned from niche scientific interest to essential industrial components.

What is Market Growth?

The market is scaling rapidly, with production volumes expected to increase from 185.66 thousand tons in 2025 to 388.02 thousand tons by 2035, maintaining a consistent CAGR of 8.95%. This growth is catalyzed by the proliferation of artificial intelligence, semiconductor advancements, and the transition toward cleaner, mercury-free industrial solutions.

Market Dynamics & Driving Factors

What Are the Key Factors Driving the Market?

-

Next-Generation Electronics: The miniaturization of components in smartphones, laptops, and servers creates significant heat dissipation challenges that only liquid alloys can efficiently mitigate.

-

Flexible and Soft Robotics: The rise of wearable health monitors and soft robotics necessitates materials that provide electrical conductivity while remaining physically adaptable and lightweight.

-

Electric Vehicle (EV) Advancements: As EVs demand high-efficiency battery cooling and power electronics, liquid alloys are becoming standard in advanced thermal management systems.

What Are the Market Benefits of Using Liquid Alloys?

Liquid alloys offer distinct advantages: superior thermal and electrical conductivity, high environmental safety compared to traditional heavy metals, and the ability to maintain stability across a wide temperature range. Furthermore, their fluid nature allows for seamless integration into compact devices, providing efficient cooling where rigid heat sinks cannot fit.

Key Segments & Trends

The market is currently pivoting from rigid systems toward smart, flexible architectures. Gallium-based alloys currently dominate the landscape, holding a 48% market share in 2025, due to their excellent conductivity and safety profile.

-

Electronics Dominance: The electronics and semiconductor segment held 42% of the market in 2025, with growth spurred by the need for advanced heat control in high-performance processors.

-

Regional Trends: The Asia Pacific region is the market leader with a 38% share, bolstered by massive semiconductor manufacturing hubs in China, Japan, and South Korea.

-

Technological Shift: Encapsulated liquid metals are gaining traction (10.6% CAGR) as they provide the stability of solid components with the performance benefits of liquid alloys.

(Suggested Data Table: Include a summary table detailing revenue growth, volume in thousand tons, and pricing CAGR from 2025 to 2035).

Competitive Landscape & Recent Developments

The competitive landscape is defined by innovators focused on high-purity chemical processing and specialized thermal interface solutions. A notable recent development occurred in February 2026, when Johnson Controls acquired Alloy Enterprises to strengthen its leadership in data center thermal management, reflecting the industry’s critical focus on cooling infrastructure.

Top Companies Profiled

-

Indium Corporation: A premier global materials supplier for electronics assembly. They specialize in gallium and indium chemistries used in advanced thermal interface products.

-

Liquidmetal Technologies, Inc.: A pioneer in non-crystalline, zirconium-based bulk metallic glasses that provide exceptional elasticity and strength.

-

Texa Metals & Alloys Pvt. Ltd.: An India-based supplier focused on low-melting-point formulations and custom non-ferrous metallic solutions for regional manufacturing.

Market Recent Government Initiatives

Global regulatory bodies are actively standardizing the trade and usage of metal alloys to ensure environmental safety:

-

United States: The EPA mandates strict reporting under the Toxic Substances Control Act (TSCA), particularly regarding mercury-added products, to reduce hazardous industrial footprints.

-

European Union: The REACH Regulation imposes rigorous registration requirements for metal imports, pushing industry players toward “Zero Pollution” objectives and the phase-out of legacy heavy metals.

-

China: Aligned with global safety standards via GB 26572-2025, the government restricts hazardous substances in electronic products, mandating strict labeling and environmental protection during the manufacturing of liquid alloys.

Future Perspective

The future of liquid alloys is intrinsically linked to the evolution of AI, quantum computing, and flexible healthcare technology. As manufacturers seek to push the boundaries of miniaturization, the demand for non-traditional, highly efficient conductive materials will intensify. Players that prioritize safer, gallium-based chemistries and invest in encapsulated delivery forms are poised to capture significant value. By 2035, liquid alloys will likely function as the invisible backbone of high-performance thermal management, enabling the next generation of power-dense, compact electronic ecosystems.

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Leave a Reply