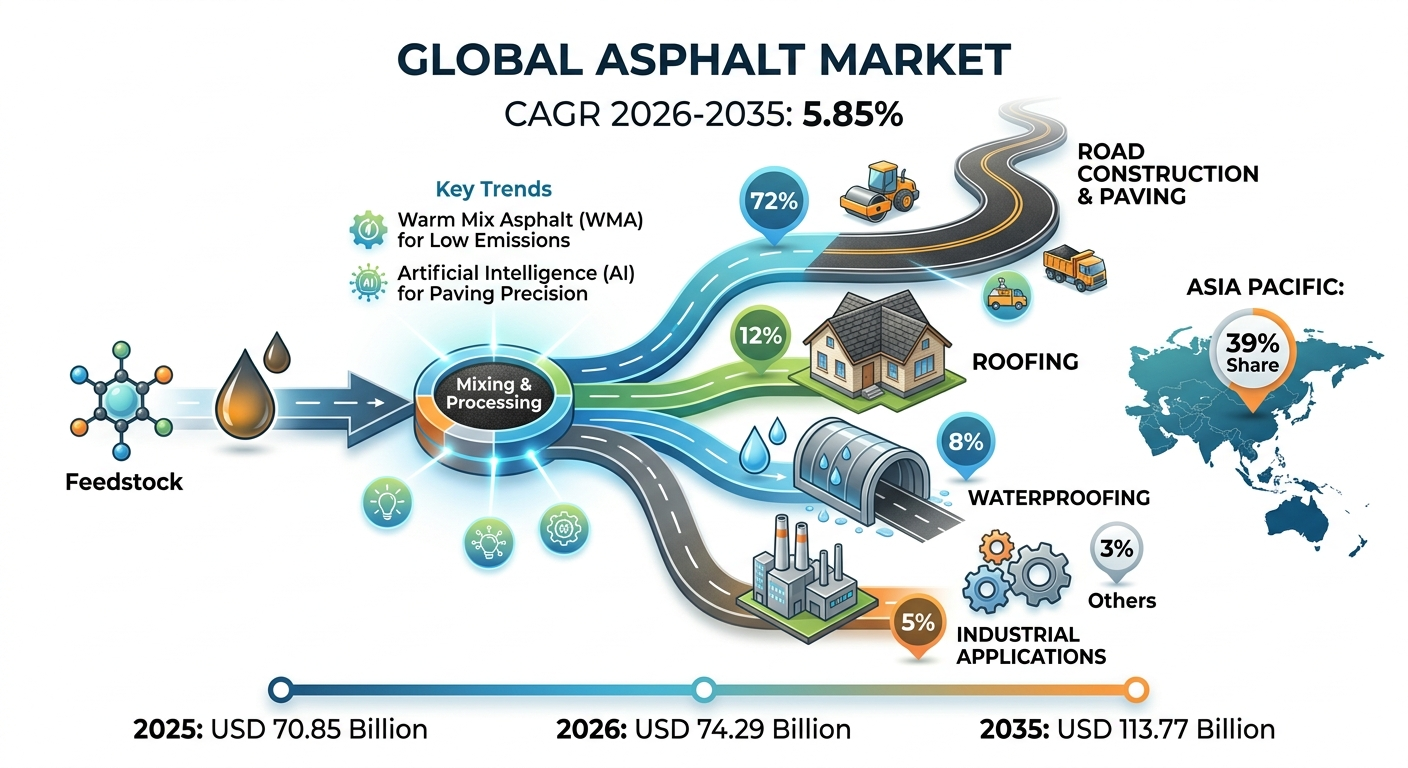

The global asphalt market is undergoing a structural expansion, serving as the primary infrastructure backbone for modern roadway, aviation, and building envelope systems. Valued at USD 70.85 billion in 2025, the market is estimated to reach USD 74.29 billion in 2026 and is projected to expand to USD 113.77 billion by 2035. This trajectory represents a steady compound annual growth rate (CAGR) of 5.85% over the forecast period from 2026 to 2035.

In terms of material volume, market consumption is anticipated to climb from 145.11 million tons in 2025 to 220.02 million tons by 2035, growing at a volume CAGR of 5.25%. The foundational growth of this sector is heavily driven by rising public sector infrastructure investments, rapid urbanization across developing nations, and an industry-wide push for climate-resilient paving options.

Market Overview

Why Is the Asphalt Market Important?

Asphalt—derived primarily from heavy crude oil refining and petroleum residues—is highly valued for its intense tensile strength, load-bearing capacity, and natural moisture resistance. It serves as an essential material for heavy civil engineering projects. Without high-grade liquid binders and asphalt concrete mixes, modern shipping corridors would suffer from rapid structural decay, airport runways would fail to bear heavy landing impacts, and building foundations would lack efficient waterproofing seals against groundwater infiltration.

Furthermore, asphalt stands as one of the most recyclable industrial materials on earth. The growing integration of Reclaimed Asphalt Pavement (RAP) allows the construction industry to achieve circular economy targets while noticeably lowering overall aggregate production costs.

What Is the Core Structure of the Asphalt Market?

The asphalt industry operates through a tightly integrated global supply chain. The process starts with crude oil extraction and petrochemical refining to secure high-viscosity petroleum residues. These binders are then chemically modified or combined with mineral aggregates in advanced mixing plants to produce high-durability surface coatings.

The industry connects raw refinery operations directly with state highway departments, commercial roofing contractors, and large-scale industrial builders. Currently, the baseline of physical volume consumption is anchored by traditional road rehabilitation projects. Concurrently, the highest value growth is shifting toward specialty polymer-modified binders designed to handle extreme climate changes and severe vehicular stress.

Market Dynamics

What Are the Key Factors Driving the Market?

-

Aggressive Government Infrastructure Budgets: Public funding initiatives are allocating significant financial resources for building expressways, rural transit routes, and highway networks.

-

Rapid Urbanization in Developing Regions: Ongoing population shifts toward cities across emerging economies are expanding the construction of residential and commercial parking structures, local roads, and public spaces.

-

Rapid Transition to Polymer-Modified Binders: To combat pavement rutting, cracking, and weathering, engineering entities are rapidly adopting polymer-modified asphalt to enhance elasticity and asset lifespans.

What Are the Primary Restraints Limiting Asphalt Market Growth?

-

Heavy Carbon and Greenhouse Gas Footprints: Traditional hot-mix manufacturing generates high localized emissions, drawing tight scrutiny and strict operating permit challenges from environmental safety regulators.

-

Raw Material Volatility and Feedstock Vulnerability: Because liquid asphalt is a byproduct of heavy crude oil processing, global fluctuations in energy markets directly disrupt production margins and supply contracts for mixing plants.

What Are the Key Market Trends?

The definitive trend steering the modern market is the rapid rise of Warm Mix Asphalt (WMA) technologies. WMA allows for lower mixing and compaction temperatures, directly cutting fuel consumption and plant emissions.

Concurrently, artificial intelligence is reshaping the supply chain. Industrial players are using IoT sensors and machine learning models to analyze historic paving performance, allowing them to optimize specific mix designs prior to on-site application.

Market Segments & Insights

Which Segment Accounted for the Largest Market Share?

The Hot Mix Asphalt (HMA) segment, the Penetration Grade product segment, and the Road Construction & Paving application segment dominated their respective areas, holding 48%, 41%, and 72% of global market shares in 2025. HMA’s top position is a direct result of its excellent load-bearing capabilities on heavy-traffic highways, while road construction remains the main consumer of global bitumen volumes.

2025 Market Share Breakdown

| Segment Category | Sub-Segment Name | 2025 Revenue Share (%) | Key Drivers & Performance Attributes |

| Material Type | Hot Mix Asphalt (HMA) | 48% | Exceptional load-bearing capacity and durability under heavy vehicle traffic. |

| Material Type | Warm Mix Asphalt (WMA) | 16% | Lower fuel consumption and reduced emissions; fastest type CAGR at 6.1%. |

| Material Type | Polymer Modified (PMA) | 15% | Enhanced elasticity and superior resistance to extreme ambient temperatures. |

| Material Type | Cold Mix Asphalt (CMA) | 10% | Highly cost-effective and versatile for emergency winter pothole repairs. |

| Product Grade | Penetration Grade | 41% | Main baseline standard for transportation infrastructure networks. |

| Product Grade | Performance Grade (PG) | 27% | Micro-level grading tailored to specific regional climates; 5.9% CAGR. |

| Application | Road Construction & Paving | 72% | Dominant volume driver fueled by aging highway resurfacing and new highways. |

| Application | Roofing & Waterproofing | 20% | High demand for reflective shingles and building foundation vapor seals. |

| End-Use Industry | Transportation Infrastructure | 68% | Driven by major public transit projects and airport runway developments. |

| Geographic Region | Asia Pacific | 39% | Leading global manufacturing and paving zone; fastest regional growth. |

What Is the Segment Growth Outlook?

The Warm Mix Asphalt (WMA) segment is projected to achieve the fastest product CAGR of 6.1% through 2035 due to its extended compaction window and strong alignment with clean air standards.

From an application perspective, moisture-resistant building materials and industrial coatings are expanding rapidly. Meanwhile, the transportation infrastructure end-use industry will continue to account for the highest total spending, driven by massive investments in international airport runways and high-speed toll road corridors.

Regional Insights

How Did Asia Pacific Dominate the Asphalt Market?

The Asia Pacific region dominated the global arena with a 39.0% revenue share in 2025 and is projected to expand at the fastest regional CAGR of 6.00% through the forecast period. Valued at USD 27.63 billion in 2025 and on track to reach USD 44.94 billion by 2035, the region’s top position is driven by extensive highway network expansions and new airport construction projects.

China is pushing national green infrastructure mandates, which has significantly expanded the localized adoption of low-temperature asphalt technologies. Meanwhile, India is heavily investing in rural road connectivity and regional expressways, providing a consistent demand baseline for high-grade bitumen binders.

North American and European Regional Dynamics

North America held 24.00% of the market share in 2025, reaching USD 17.00 billion, driven by federal infrastructure spending packages and extensive roadway expansions across growing states like Texas and Florida.

Europe maintained a 22.00% revenue share in 2025, heavily influenced by strict EU decarbonization goals that favor sustainable asphalt alternatives and smart manufacturing plants. Latin America (8% share) and the Middle East & Africa (7% share) are growing steadily, driven by bio-based additive usage in Brazil and massive luxury real estate and airport projects like NEOM in Saudi Arabia.

Benefits of Using Advanced Asphalt Solutions

-

Exceptional Long-Term Pavement Durability: Advanced polymer-modified and hot-mix asphalt types provide high load-bearing strength, preventing early ruts on high-traffic highways.

-

Significant Reductions in Energy Costs: Using warm-mix asphalt technologies allows plants to operate at lower temperatures, leading to decreased fuel consumption and fewer greenhouse gas emissions.

-

High Weather and Thermal Resistance: Specialized asphalt grades offer excellent elasticity, preventing road cracking during freezing winters and avoiding melting or bleeding during extreme summer heatwaves.

-

Cost-Effective Sourcing and Sustainability: Asphalt mixtures seamlessly support reclaimed asphalt pavement integration, allowing companies to reuse old materials, limit landfill waste, and lower initial aggregate processing costs.

Competitive Landscape

Top Companies in the Asphalt Market

Exxon Mobil Corporation (US)

-

About: A leading publicly traded international energy and chemical corporation, processing upstream crude resources into high-performance industrial products.

-

Products: AC penetration grade binders, polymer-modified bitumen, and heavy asphalt base stocks.

-

Market Capitalization: Valued at approximately USD 621.42 billion as of June 2026.

Marathon Petroleum Corporation (US)

-

About: A prominent downstream energy company operating an extensive refining network and supplying high-quality paving materials across North America.

-

Products: Slurry seal binders, industrial roofing flux, and multi-grade commercial paving asphalt.

-

Market Capitalization: Valued at approximately USD 76.80 billion as of June 2026.

Shell plc (UK/NL)

-

About: A global group of energy and petrochemical companies focusing on advanced chemical synthesis and sustainable low-temperature binding solutions.

-

Products: Shell Cariphalte polymer-modified binders, specialty industrial emulsions, and eco-friendly paving products.

-

Market Capitalization: Valued at approximately USD 243.55 billion as of June 2026.

CEMEX S.A.B. de C.V. (MX)

-

About: A major global building materials company providing high-quality construction aggregates and asphalt concrete mixes worldwide.

-

Products: Commercial hot-mix asphalt, high-durability paving concrete, and customized building foundation coatings.

-

Market Capitalization: Valued at approximately USD 17.28 billion as of June 2026.

China Petroleum & Chemical Corporation / Sinopec (CN)

-

About: A dominant energy and chemical enterprise in the Asia-Pacific region, driving high-volume bitumen processing for major civil engineering projects.

-

Products: Heavy-duty performance grade asphalt, specialized anti-rutting binders, and airport runway paving mixes.

-

Market Capitalization: Valued at approximately USD 91.50 billion equivalent as of mid-2026.

What Is the Status of Recent Strategic Developments?

The competitive landscape highlights an active focus on building alliances and creating unified networks for infrastructure materials:

-

December 2025: Arisinfra Solutions signed a formal Memorandum of Understanding (MoU) with JS Infra Solutions to pursue strategic collaborations within the asphalt and road infrastructure materials sector. Operating directly at the project execution layer, JS Infra Solutions is recognized as one of the top ten high-volume asphalt mixing producers in the Mumbai region, strengthening the raw supply chain across fast-growing municipal zones.

What Is the Regulatory Landscape Governing Asphalt Production?

Environmental agencies and government bureaus enforce strict compliance rules to reduce emissions and ensure consistent pavement quality:

-

United States: The EPA enforces strict Clean Air Act Title V operating permits for asphalt plants. These regulations cap volatile organic compounds (VOCs), sulfur dioxide, and particulate matter to minimize localized air pollution near urban centers.

-

Germany: Paving operations must comply with TA Luft (Technical Instructions on Air Quality Control). This standard mandates strict emission limits for carcinogenic elements, organic substances, and nitrogen oxides during asphalt synthesis.

-

China: The Ministry of Ecology and Environment (MEE) executes ultra-low emission baselines for heavy industries. All asphalt plants in key economic zones must install enclosed raw storage yards, fabric filter baghouses, and continuous emission monitoring systems (CEMS).

What Are the Recent Government Initiatives Supporting the Market?

Governments around the world are passing sweeping infrastructure bills that directly drive asphalt market volumes. In North America, federal funding initiatives for roadway rehabilitation focus on highway resurfacing and bridge refurbishments. State mandates in these regions are increasingly requiring a high percentage of Recycled Asphalt Pavement (RAP) within mixing batches to reduce carbon footprints.

Similarly, the European Union’s green infrastructure funding supports low-temperature warm-mix asphalt projects. In Asia, India’s rural connectivity initiatives are investing heavily in expanding transit routes, which sustains strong demand for penetration grade materials across rural belts.

What Is the Future of the Market?

The future of the asphalt industry will be shaped by the growth of bio-based binders and the widespread use of automated, smart mixing technologies. Over the next ten years, traditional petroleum residues will increasingly be blended with waste rubber-modified additives and bio-resins to meet corporate net-zero goals.

At the same time, the integration of autonomous paving equipment and real-time thickness monitors will improve paving accuracy. While traditional hot mix asphalt will still be required for heavy-duty highway foundations, long-term market value will favor warm mix alternatives and smart performance-graded mixtures. This shift will redefine modern highway design and sustainable infrastructure durability through 2035.

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Email: [email protected]

Leave a Reply