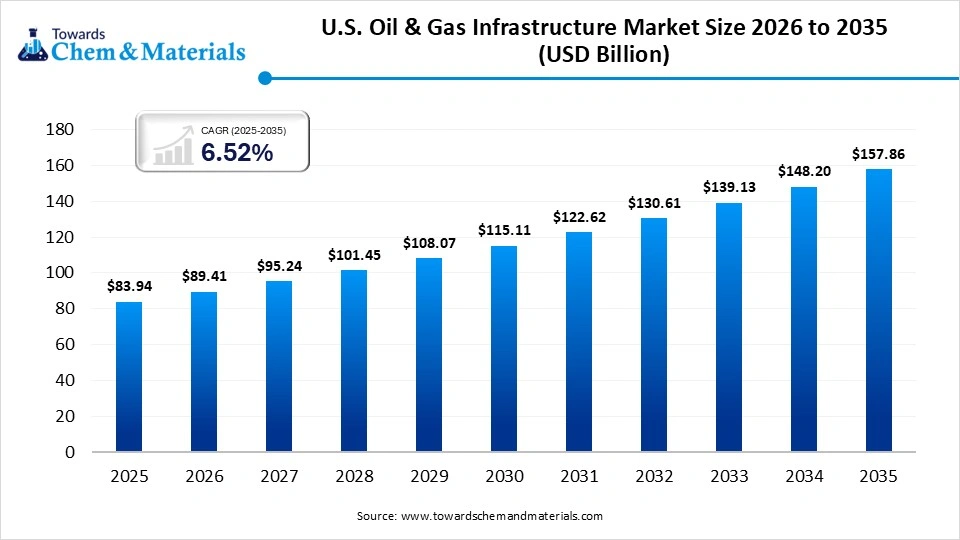

The U.S. oil & gas infrastructure market size is expected to grow from USD 83.94 billion in 2025 to USD 89.41 billion in 2026 and is forecast to reach USD 157.86 billion by 2035 at a 6.52% CAGR over 2026-2035. The booming natural gas, increasing energy demand, and focus on energy independence drive the market growth.

Executive Summary: High-Level Market Forecast

An evaluation of domestic energy logistics shows sustained capital deployment across midstream assets and cryogenic marine terminals.

-

2025 Market Valuation: USD 83.94 Billion

-

2026 Market Valuation (Current Year): USD 89.41 Billion

-

Projected Market Value (by 2035): USD 157.86 Billion

-

Compound Annual Growth Rate (CAGR): 6.52% (2026–2035)

By the year 2032, the domestic infrastructure landscape is systematically on track to eclipse a market valuation of USD 131 billion. This growth trajectory highlights an aggressive infrastructure expansion driven by an international demand for liquefied natural gas (LNG), a resilient domestic industrial base, and a focus on complete North American energy independence.

Market Dynamics: Drivers, Restraints, and Opportunities

What Are the Key Factors Driving the Market?

The growth of this market is driven by expanding industrial demand, growing residential heating requirements, and a surge in LNG export capacity. As the domestic population increases and residential construction expands, the demand for natural gas to power residential appliances, HVAC heating systems, and electricity grids rises steadily.

Concurrently, a growing transportation sector across maritime, road, and aviation logistics requires a continuous, high-volume supply of refined petroleum products. This consistent consumption forces operators to continually expand, debottleneck, and optimize their pipeline networks and storage capacities.

What Limits the Expansion of Energy Infrastructure?

The primary market challenge stems from high initial development costs and complex regulatory approval processes. Constructing large-scale pipelines, cryogenic terminals, and processing facilities requires massive upfront capital investments, intricate supply chain sourcing, and specialized heavy machinery.

Furthermore, operators must navigate rigorous environmental reviews, land-acquisition legal hurdles, and public opposition. These challenges can extend project timelines by years, exposing developer capital to changing macroeconomic conditions and fluctuating global crude oil and gas prices.

Where Do the Greatest Market Opportunities Lie?

The ongoing global transition toward lower-carbon energy sources represents a major commercial opportunity for midstream developers. Because natural gas produces lower carbon emissions than coal or heavy fuel oil, it serves as a critical bridge fuel for power generation worldwide.

This shift creates an immediate opportunity to construct advanced gas processing and liquefaction plants, expand export-oriented pipeline networks, and integrate digital twins and IoT sensors. These technologies help monitor infrastructure in real time, minimize methane emissions, and optimize overall operational efficiency.

Regulatory Landscape and Policy Shifts

What Is the Status of Market Recent Government Initiatives?

Federal energy policies are reshaping the operational requirements for U.S. infrastructure operators. The U.S. Department of Energy (DOE) and the Federal Energy Regulatory Commission (FERC) are balancing emission-reduction goals with the need to ensure domestic energy security.

Recent federal actions prioritize upgrading legacy pipelines to prevent methane leaks and streamline permitting processes for infrastructure that incorporates carbon capture and storage (CCS) tie-ins. Additionally, international trade partnerships and export authorizations are driving the rapid development of large-scale LNG terminals along the U.S. Gulf Coast to supply global markets

Infrastructure Benefits & Operational Value

Why Is This Market Important to Modern Industry?

Oil and gas infrastructure serves as the central circulatory system of the modern industrial economy. It bridges the geographic gap between remote production basins and dense municipal or industrial end-users.

Without a well-maintained network of pipelines, compressor stations, and processing facilities, energy markets would suffer from severe regional price imbalances. Furthermore, production basins would face localized supply gluts, and major manufacturing sectors would lack the reliable feedstocks needed to sustain automated operations.

What Are the Primary Benefits of Strategic Infrastructure?

-

Logistical Cost Efficiency: Moving energy through pipelines remains far cheaper and safer than transporting oil or compressed gas via rail or road networks.

-

Market Stabilization: Large-scale underground storage facilities balance out seasonal demand spikes, protecting consumers from extreme price volatility.

-

Global Export Capability: Advanced marine liquefaction terminals convert domestic natural gas into a mobile global commodity, strengthening the U.S. trade position.

Segmental Insights & Deep-Dive Analysis

Which Segment Accounted for the Largest Market Share?

Evaluating the market by sector shows that the midstream segment leads the industry, commanding a 43% revenue share due to the country’s vast 3-million-mile pipeline network.

When looking at infrastructure types, interstate pipelines hold the largest position at 38%, acting as the primary cross-country routes for long-distance energy transport.

In terms of fuel types, natural gas accounts for 47% of infrastructure utilization, favored for its affordability in industrial processing and domestic power generation.

Materially, high-strength carbon steel represents 56% of the market because it is readily available and durable enough to handle high-pressure pipeline and refinery environments.

Finally, independent midstream operators lead the ownership segment with a 44% share, outperforming integrated oil majors by focusing exclusively on toll-based storage and transport services.

What Are the Key Emerging Trends in Sub-Segments?

While legacy assets hold the largest current shares, the fastest-growing sectors reflect a clear shift toward international exports and advanced materials. The LNG export facilities segment and gas processing/liquefaction plants are growing rapidly, driven by billions of dollars in private equity and joint-venture investments along the Gulf Coast.

Fuel trends show the LNG & NGLs segment expanding quickly due to growing demand from foreign buyers and the global petrochemical sector. To improve asset lifespans, operators are increasingly using composites and corrosion-resistant alloys over traditional steel. This trend is particularly evident in offshore platforms and gathering lines, where these materials help lower long-term maintenance costs.

Structural Market Breakdown

The following data matrix outlines the current market breakdown, highlighting the dominant segments and the high-growth vectors shaping the industry.

U.S. Oil & Gas Infrastructure Market Segment Matrix

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Leave a Reply