The U.S. textile market size was estimated at USD 402.18 billion in 2025 and is expected to be worth around USD 652.00 billion by 2035, growing at a CAGR of 4.95% from 2026 to 2035. In terms of volume, the U.S. textile industry is projected to grow from 19.04 million tons in 2025 to 28.59 million tons by 2035, exhibiting a compound annual growth rate (CAGR) of 4.15% over the forecast period from 2026 to 2035.The growth of the market is driven by technological advancements, growing consumer demand for sustainable and high-quality products, and the expansion of e-commerce.

Market Size and Volume Projections

The structural expansion of the domestic textile industry is driven by advanced automation, supply chain localization efforts, and a surging consumer demand for sustainable fabrics.

-

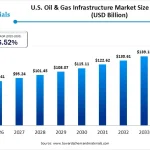

2025 Baseline Market Size: Estimated at USD 402.18 billion.

-

2026 Market Size: Projected to hit USD 422.09 billion.

-

2035 Forecasted Valuation: Anticipated to reach USD 652.00 billion, progressing at a revenue CAGR of 4.95% from 2026 to 2035.

-

Physical Volume Metrics: In terms of production output, the industry is poised to expand from 19.04 billion square meters in 2025 to 28.59 billion square meters by 2035, exhibiting a volume CAGR of 4.15%.

-

Pricing Trends: In 2025, the average manufacturing cost stood at USD 14.92 per kg against an average selling price of USD 22.56 per kg, with a projected pricing CAGR of 3.29% through 2035.

Strategic Market Share Breakdown

The market is segmented by product types, foundational raw materials, and specialized end-use applications.

1. By Product Type (2025 Revenue Share)

-

Natural Fibers (36%): Held the leading share in 2025. These materials (cotton, wool, silk) dominate apparel and home furnishings due to their breathability and natural biodegradability.

-

Polyester (34%): Follows closely due to its cost-effectiveness and versatility. The adoption of recycled polyester (rPET) from plastic bottles is a major driver.

-

Nylon (18%): Widely utilized for high-performance sportswear, industrial fabrics, and automotive applications due to its superior elasticity and chemical resistance.

-

Others (12%): Includes specialized blends and experimental polymers.

2. By Raw Material (2025 Revenue Share)

-

Cotton (39%): Serves as a primary cornerstone of the sector, supported by expanding consumer demand for ethical sourcing and organic eco-labels.

-

Chemical (31%): Synthetics like polyester and nylon dominate bulk manufacturing lines due to their adaptability and mass-production efficiency.

-

Wool (12%) & Silk (8%): Represent stable premium tiers, with silk expanding specifically within luxury fashion and niche home design segments.

-

Others (10%): Encompasses alternative organic and bio-based polymers.

3. By Application (2025 Revenue Share)

-

Household (33%): Commands the top spot, driven by interior decor trends in bedding, upholstery, carpets, and antimicrobial home fabrics.

-

Technical Textiles (29%): High-growth segment engineered purely for performance, durability, and insulation. It serves critical functions across the automotive, healthcare, aerospace, and defense sectors.

-

Fashion (28%): Represents the primary consumer-facing engine, heavily accelerated by e-commerce expansion and circular textile integration.

-

Others (10%): Cover alternative industrial application methods.

Macro Trade and Supplier Ecosystems

The United States maintains a robust global trade footprint. In 2024, the U.S. exported USD 24.7 billion worth of textiles, ranking as the 14th most exported domestic product overall.

-

Primary Export Destinations: Major volume corridors flow to Mexico ($6.07B), Canada ($4.32B), and China ($2.1B). Secondary specialized lanes target India, Pakistan, and South Korea.

-

Global Export Standings: On a volume scale, the top three global exporters are India (10,096 shipments), China (6,660 shipments), and the United States (4,863 shipments).

-

Leading Supplier Concentration: Out of 20,310 total domestic suppliers, a small cluster of massive shipping entities controls over half of the market share. Tyson Fresh Meats Inc. leads with 29% of the market share (7,914 shipments), followed by Deere and Company at 14% (3,765 shipments), and Helvetia Container Line at 10% (2,651 shipments).

Regulatory and Innovation Initiatives

The modern market operates within tight environmental and geopolitical boundaries:

-

Supply Chain & Human Rights Enforcement: The U.S. Customs and Border Protection (CBP) enforces the Uyghur Forced Labor Prevention Act (UFLPA) to mandate strict traceability, alongside the Berry Amendment which requires 100% domestic sourcing for military and national defense textiles.

-

The Circular Economy Shift: Recent 2025 initiatives highlight this transition. Major brands signed a Memorandum of Understanding in California to launch Textile Pro, designed to handle waste logistics in compliance with Extended Producer Responsibility (EPR) laws.

-

Material Science Breakthroughs: Technical producers are aggressively launching lighter, stronger composites (such as Avient’s new generation of Dyneema Woven Composites) and eliminating toxic chemistries, such as Milliken & Company becoming the first to introduce 100% non-PFAS materials for all layers of firefighter turnout gear.

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Leave a Reply