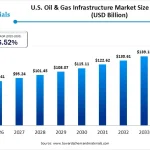

The United States bioplastics industry is transitioning from a niche environmental alternative into a baseline requirement for high-performance circular economies. Validated market data sets the baseline U.S. bioplastics market size at USD 3.72 billion in 2025. Driven by massive domestic agricultural feedstock advantages and aggressive state-level mandates against fossil-fuel-derived polymers, the market is positioned to rise from USD 4.44 billion in 2026 to a projected USD 21.84 billion by 2035. This rapid expansion represents an extraordinary Compound Annual Growth Rate (CAGR) of 19.35% over the 2026–2035 forecast period.

Market Overview & Dynamics

Why Is The U.S. Bioplastics Market Crucial for the Chemical Industry?

Bioplastics—defined as macromolecular materials synthesized entirely or partially from renewable biomass resources such as corn starch, sugarcane, cellulose, and agricultural residue wastes are replacing traditional petroleum plastics across high-volume supply chains. Their structural importance lies in their dual-track functional utility: they replicate the exact water resistance, tensile strength, and oxygen barrier protection of legacy polymers while decoupling manufacturing from crude oil dependencies. By integrating bioplastics, consumer-facing enterprises and industrial manufacturers can insulate themselves from petroleum price volatility, directly lower corporate Scope 3 carbon emissions, and comply with strict municipal single-use plastic bans.

What Are the Key Factors Driving The Market?

The market’s high growth trajectory is sustained by three structural drivers:

-

Abundant Domestic Renewable Feedstock Networks: The intensive cultivation of industrial corn, soybeans, and sugarcane across agricultural states ensures a stable, reliable source of foundational raw materials.

-

The Federal BioPreferred Purchasing Framework: Government procurement policies mandate that federal agencies prioritize bio-based alternatives, creating a reliable baseline market demand.

-

Corporate Decarbonization Pressures: Fortune 500 consumer packaged goods (CPG) companies are actively modifying their global structural designs to meet ambitious net-zero carbon targets and improve brand equity.

What Are the Key Market Trends & Technological Shifts?

The modern bioplastics landscape is undergoing a major technological transformation, moving beyond basic compounding to advanced molecular engineering.

-

AI-Driven Material Discovery: Artificial intelligence is accelerating the discovery of new bioplastics by predicting material performance before physical synthesis. AI models optimize fermentation kinetics, reduce trial waste, and predict how molecules will break down over time. A prominent example is the strategic partnership between B2En and Reborn Materials, which uses AI platforms to pioneer specialized bio-plastic functional variations.

-

Catalytic Processing and Molecular Tuning: Manufacturers are refining advanced catalytic processes to improve the heat resistance and structural integrity of bio-based resins. This allows bioplastics to match the performance of engineering-grade polyolefins.

-

Upcycling Agricultural and Industrial Waste: Production is shifting toward next-generation feedstocks, utilizing forestry byproducts, organic municipal waste, and agricultural residues like cotton gin trash to avoid competing with food crop land.

Trade, Value Chain, & Data Presentations

What Does the U.S. Bioplastics Trade Imbalance Indicate?

An analysis of customs data reveals that the United States is currently a heavy net importer of both functional bioplastics and raw biodegradable polymers. Over recent trade periods, the U.S. exported 15 shipments of finished bioplastics while importing 159 shipments. This trend is even more pronounced in raw biodegradable plastic resins, where the U.S. exported only 19 shipments compared to 476 inbound shipments. This trade deficit highlights a critical market gap: while domestic consumer demand is rising exceptionally fast, domestic chemical processing and polymerization capacity must expand significantly to achieve true regional self-sufficiency.

Key Market Data Summary

The following matrix details the core performance metrics defining the U.S. bioplastics market through 2035:

| Report Attribute | Baseline & Forecast Metrics |

| 2025 Base Year Value | USD 3.72 Billion |

| 2026 Market Size Value | USD 4.44 Billion |

| 2035 Projected Revenue | USD 21.84 Billion |

| Market Growth Rate | CAGR of 19.35% (2026 – 2035) |

| Dominant Application Segment | Rigid & Flexible Packaging (61% Market Share) |

| Fastest Growing Application | Automotive & Transportation Components |

Regional Dynamics: State-by-State Analysis

Different states leverage unique localized assets to drive the national bioplastics market forward.

Leave a Reply