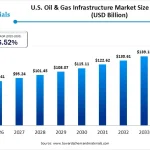

The U.S. chemical distribution market functions as the operational backbone of North American industrial supply chains. Validated data fixes the market size at USD 29.11 billion in 2025. Propelled by digital supply chain integration and a profound structural pivot toward advanced specialties, the market is positioned to expand from USD 31.30 billion in 2026 to an anticipated USD 60.16 billion by 2035. This trajectory represents a steady Compound Annual Growth Rate (CAGR) of 7.53% over the 2026–2035 forecast window.

Market Overview & Dynamics

Why Is The U.S. Chemical Distribution Market Important?

Chemical distributors serve as critical tier-one supply chain intermediaries, bridging the gap between asset-heavy chemical producers and fragmented mid-to-downstream industrial end-users. In the United States—a global epicentered force in advanced chemical processing—distributors do not merely transport freight; they de-risk the supply chain. By managing highly volatile freight logistics, offering localized chemical storage, and assuming strict regulatory reporting burdens, distributors insulate core domestic manufacturing, pharmaceutical synthesis, and agricultural production from severe single-source component failures.

What Are the Key Factors Driving The Market?

The rapid evolution of this sector stems from three overlapping market drivers:

-

Downstream Technical Evolution: Advanced manufacturing paradigms require highly precise, micro-engineered formulations. This shifts the distributor’s role from basic bulk breaking to active technical co-development.

-

Logistical Optimization & AI Automation: The implementation of predictive logistics networks directly addresses legacy inefficiencies, maximizing fleet asset utilization and minimizing inventory overhead.

-

Chemical Sourcing Realignment: Volatile geopolitical climates have forced a structural shift toward localized, highly resilient supply networks, accelerating regional chemical distribution infrastructure investments.

What Are the Key Market Trends & Technological Shifts?

The modern chemical distribution framework is undergoing a profound structural evolution, moving rapidly away from legacy analog models.

-

The Shift to Speciality Formulations: Distributors are aggressively moving up the value chain by prioritizing high-margin specialty chemicals over low-margin commodities. Success in this domain relies on providing advanced technical selling, on-site blending, and custom laboratory formulations.

-

Digitalization and AI Integration: The industry is deploying AI-driven inventory management, automated warehouse distribution grids, and IoT-enabled real-time chemical tracking to optimize complex storage parameters.

-

Green Chemistry and ESG Priorities: Escalating regulatory mandates and evolving corporate environmental targets are accelerating the distribution of bio-based surfactants, eco-friendly solvents, and sustainable chemical alternatives.

Trade, Value Chain, & Data Presentations

What Does the U.S. Chemical Trade Flux Indicate?

Global trade lane data reveals clear, diverging trends between specialty imports and organic export volumes. Over the trailing twelve months (TTM) running from mid-2024 to mid-2025, inbound U.S. specialty chemical shipments contracted by 8%, settling at 82 key shipments. This contraction highlights an ongoing domestic push to mitigate overseas supply chain dependencies.

Conversely, U.S. organic chemical exports surged dramatically, posting an impressive 217% growth rate with 4,357 distinct outbound shipments. This export boom was driven primarily by strong demand from rapidly growing industrial manufacturing sectors in India, Brazil, and Belgium.

Key Market Data Summary

The following structural breakdown maps the core metrics defining the U.S. chemical distribution outlook:

| Report Attribute | Baseline & Forecast Metrics |

| 2025 Base Year Value | USD 29.11 Billion |

| 2026 Market Size Value | USD 31.30 Billion |

| 2035 Projected Revenue | USD 60.16 Billion |

| Market Growth Rate | CAGR of 7.53% (2026 – 2035) |

| Dominant Product Segment (2025) | Commodity Chemicals (71% Revenue Share) |

| Fastest Growing Segment | Application-Specific Specialty Chemicals |

What Is the Comprehensive U.S. Chemical Distribution Value Chain?

The domestic chemical distribution value chain transforms raw, bulk-synthesized compounds into highly precise, certified industrial ingredients.

What Is the Chemical Distribution Regulatory Landscape?

Distributors operate within a complex, multi-agency regulatory matrix designed to enforce safety, security, and traceability at every stage of the supply chain.

| Regulatory Body | Key Enacted Regulations | Core Focus Areas & Impact |

| U.S. EPA | TSCA (Lautenberg Act Reform), FIFRA, EPCRA | Enforces strict, pre-market chemical safety reviews and emission compliance controls for newly introduced chemical mixtures. |

| OSHA | HazCom Standard, Process Safety Management (PSM) | Dictates mandatory GHS-aligned labeling, explicit safety data sheets (SDS), and hazardous workplace handling protocols. |

| U.S. DOT | Hazardous Materials Regulations (HMR) | Controls the packaging, multi-modal classification, and transport documentation of chemical freight across state lines. |

| DHS | CFATS (Chemical Facility Anti-Terrorism Standards) | Imposes strict inventory tracking and risk-based site security protocols on distributors storing high-risk chemical agents. |

Segmental Insights

Which Segment Accounted for the Largest Market Share?

The commodity chemicals segment dominated the market, commanding a commanding 71% revenue share in 2025. Commodity chemicals encompass high-volume, standardized industrial compounds—such as mineral acids, major chemical solvents, basic polymers, and foundational industrial salts. These materials are heavily consumed across core infrastructure, automotive manufacturing, heavy agriculture, and civil construction projects.

Because commodities are highly standardized, competition centers almost entirely on logistics cost-efficiency. Success in this segment requires vast scale, automated bulk terminal storage, highly optimized freight pathways, and long-term, high-volume contract pricing frameworks.

Why is the Specialty Chemicals Segment Growing the Fastest?

While commodities provide foundational volume, the specialty chemicals segment is projected to grow at the fastest rate through 2035. Specialty chemical formulations—such as advanced catalytic additives, functional coatings, structural adhesives, and highly pure cosmetic or pharmaceutical active ingredients—are valued for their performance characteristics rather than their molecular weight.

This rapid growth is fueled by demanding technological advancements in next-generation electronics manufacturing, automotive lightweighting, and specialized pharmaceutical synthesis. Specialty distribution requires dedicated technical sales teams, application testing laboratories, and custom compounding capabilities, allowing distributors to command significantly higher margins.

What Are the Market’s Recent Government Initiatives?

Federal and state initiatives are reshaping chemical distribution networks, driving a dual focus on environmental compliance and supply chain security:

-

The TSCA Modernization Rollout: Ongoing EPA rulemakings under the Lautenberg Chemical Safety Act have significantly slowed the commercial introduction of legacy PFAS-containing formulations, forcing distributors to source and scale alternative chemical technologies.

-

Infrastructure and Jobs Act Investments: Substantial federal capital injections into regional infrastructure have driven unprecedented demand for industrial construction chemicals, polymers, and protective coatings.

-

The CHIPS and Science Act Infrastructure: The expansion of domestic semiconductor fabrication facilities has created highly profitable, localized corridors for ultra-high-purity specialty process chemicals, driving distributors to build specialized cleanroom distribution warehouses.

Competitive Landscape: Top Companies Profiled

Univar Solutions Inc.

-

About: Headquartered in Downers Grove, Illinois, Univar Solutions stands as a premier global chemical distributor. The company operates a sophisticated, deeply integrated network of distribution centers across North America.

-

Products: Offers a comprehensive, world-class portfolio spanning both high-volume commodity chemicals and highly specialized ingredients for life sciences, personal care, pharmaceutical synthesis, and industrial coatings.

-

Market Capitalization / Financial Footprint: Private (Acquired by Apollo Global Management; records annual revenues exceeding USD 11 billion).

Brenntag North America

-

About: As the North American operating division of Germany-based Brenntag SE, this entity leverages global supply chains to deliver precise, localized chemical management solutions.

-

Products: Maintains a highly diversified portfolio split cleanly between Brenntag Essentials (industrial commodities) and Brenntag Specialties (advanced performance materials, polymers, and active ingredients).

-

Market Capitalization: Approximately USD 10.4 Billion (Parent entity Brenntag SE).

IMCD US

-

About: A leading specialist in the sales, marketing, and distribution of highly technical specialty chemicals and food ingredients, backed by an extensive network of application laboratories.

-

Products: Focuses exclusively on high-margin specialties, including advanced pharmaceutical excipients, personal care active compounds, complex plastic additives, and structural coatings.

-

Market Capitalization: Approximately USD 8.2 Billion (Parent entity IMCD N.V.).

Helm US Corporation

-

About: A prominent branch of the global, family-owned HELM AG organization, Helm US excels at combining asset-light international chemical trading with reliable, localized distribution channels.

-

Products: Specializes in bulk industrial chemicals, crop protection products, pharmaceutical active pharmaceutical ingredients (APIs), and specialized human nutrition compounds.

-

Market Capitalization: Privately held parent enterprise (HELM AG).

What Is the Future & Recent Developments of the Market?

The competitive landscape is consolidating rapidly as major players pursue strategic acquisitions to expand their geographic reach and build out their specialty technical capabilities.

1.Lindsay Goldberg Acquires EMCO Chemical Distributors:November 2025.

What Is the Future of the Market?

The future of U.S. chemical distribution lies at the intersection of logistical intelligence and green chemistry. Over the next decade, standard transactional distribution will give way to “Distribution-as-a-Service” (DaaS) models. Under this paradigm, tier-one distributors will integrate directly with their customers’ enterprise resource planning (ERP) systems via automated APIs, triggering automated chemical deliveries based on real-time factory output.

Furthermore, as strict environmental mandates continue to reshape industrial chemistry, distributors who possess the laboratory assets to help mid-market manufacturers transition from legacy synthetic formulations to bio-based alternatives will secure the highest market share and dominate the landscape through 2035.

Leave a Reply