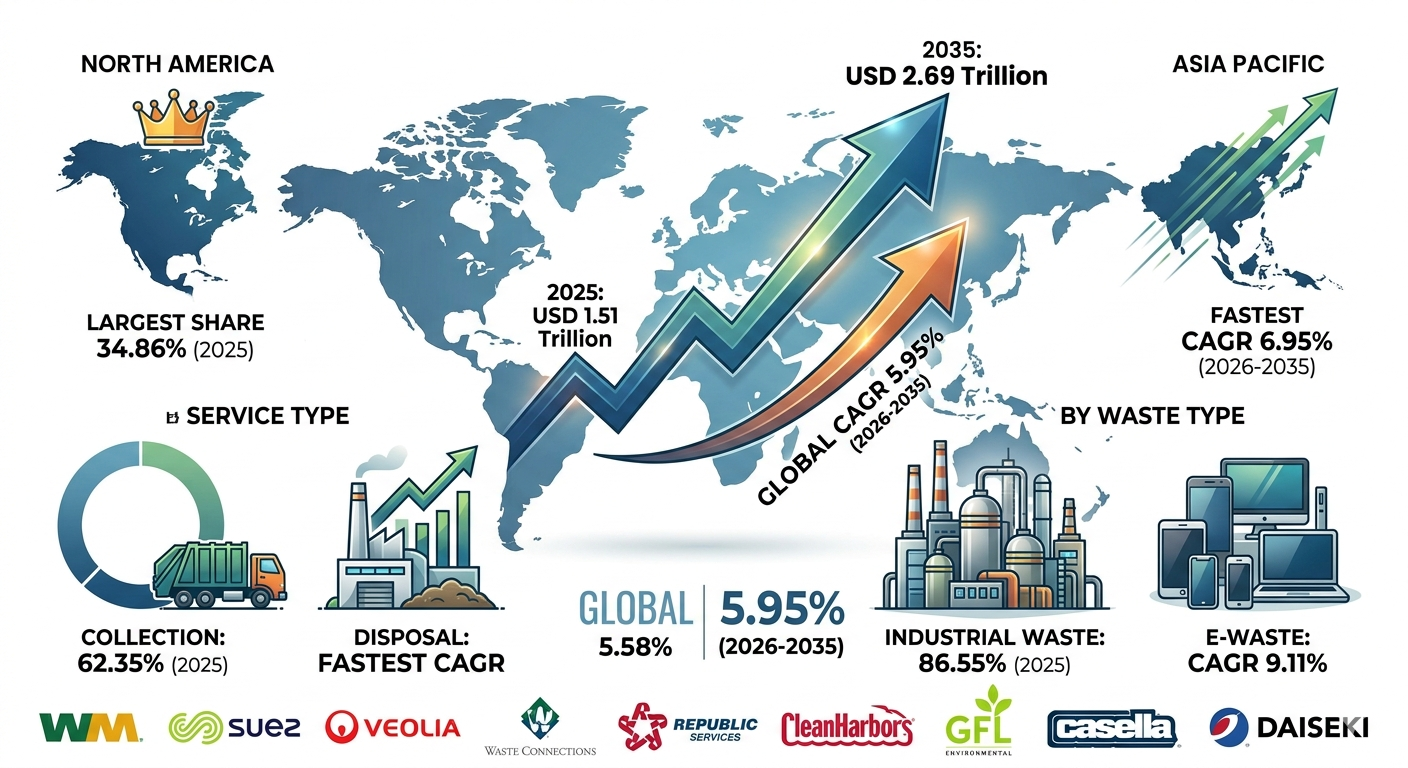

The global landscape for industrial and municipal treatment frameworks is undergoing a profound structural transition, heavily driven by advanced resource recovery protocols and aggressive circular economy initiatives. Globally valued at USD 1.51 trillion in 2025, the global waste management market is predicted to expand from USD 1.60 trillion in 2026 to an estimated valuation of approximately USD 2.69 trillion by 2035. This trajectory represents a steady Compound Annual Growth Rate (CAGR) of 5.95% over the forecast period. Based on these systemic acceleration vectors, mid-term industry forecasting models project the global market value to reach USD 2.26 trillion by the year 2032, expanding under rigorous regulatory compliance demands and high volumes of industrial output.

Market Overview

What is the Global Waste Management Market?

The global waste management market comprises the systematic framework of collection, transportation, processing, recycling, and final disposal of residual materials generated by human and industrial actions. Modern operations have evolved from simple logistics and containment practices into highly engineered chemical, material, and biological recovery ecosystems. The system treats a broad spectrum of inputs including municipal solid waste, hazardous industrial manufacturing streams, and specialized tech-refuse. It relies heavily on optimized routing, advanced materials separation, thermal conversion processes, and strict chemical stabilization techniques to mitigate ecosystem degradation while maximizing material loop closure.

Market Dynamics

What Are the Key Factors Driving the Market?

Industrial scale-up and rigid manufacturing environmental regulations stand as the primary catalysts driving this trillion-dollar industry forward. Globally, the accelerating shift toward the minimization of hazardous chemical waste and the establishment of environmentally benign manufacturing bases have altered standard corporate operating procedures. Factories and chemical processing plants are producing waste volumes that vastly outpace municipal sectors, requiring highly specialized handling, treatment, and neutralizing technologies. Additionally, rapid urbanization across emerging corridors presents an unprecedented structural challenge, requiring massive capital investments in modern automated collection grids and highly optimized intermodal logistics lines.

Market Growth and Projections

What is Market Growth Across Key Geographies?

Geographic growth reveals a distinct bifurcated expansion dynamic between mature, infrastructure-heavy western regions and rapidly scaling developing industrial zones. North America dominated the global waste management landscape with a commanding market share of 34.86% in 2025, a leading position secured by extensive automation, dense regulatory mandates, and highly sophisticated integrated collection infrastructures. Conversely, the Asia-Pacific region is emerging as the fastest-growing geographical theater, projected to expand at an accelerated CAGR of 6.95% from 2026 to 2035. This regional surge is propelled by intense industrialization, expanding commercial chemical manufacturing hubs, and aggressive urbanization metrics across major developing nations.

Key Market Trends

What is the Technological Focus of Emerging Market Trends?

The prominent trend reshaping the modern marketplace is the rapid integration of advanced sorting automation and waste-to-energy technologies designed to maximize raw material extraction and energy yields. Facilities are increasingly moving away from legacy mechanical sorting, adopting instead artificial intelligence-driven optical sorters and advanced robotic arms capable of differentiating polymer grades and metallurgical properties in real time. Concurrently, traditional landfill methods are being replaced by highly efficient anaerobic digestion units and thermal mass-burn technologies. This shift transforms post-industrial residual streams into secondary raw chemical ingredients or feeds them directly back into localized electrical grids.

Market Segments Analysis

Which Segment Accounted for the Largest Market Share?

An granular analysis by Service Type and Waste Type highlights the immense scale and structural changes taking place across individual operational divisions.

-

By Service Type: The Collection segment dominated the baseline year of 2025, commanding a significant 62.35% revenue share. This leadership stems from its status as the foundational, asset-intensive logistically demanding phase within any modern recycling framework. However, the Disposal segment is poised to exhibit the fastest growth profile with an estimated CAGR of 7.88% from 2025 to 2035, driven by the rollout of sophisticated waste-to-energy plants and deep geological encapsulation structures.

-

By Waste Type: The Industrial Waste segment held clear structural dominance in 2025, claiming a massive 86.55% market share due to the sheer material volume generated by chemical processing, heavy metallurgy, and manufacturing sectors. Meanwhile, the specialized E-waste segment is projected to register the highest growth rate, expanding at a sharp CAGR of 9.11% from 2026 to 2035 as consumer electronics replacement frequencies escalate globally.

Strategic Data Presentation

Where Should Key Sector Metrics Be Structured?

To accurately model operational investments and evaluate capital allocation strategies across segment interfaces, engineers and market research analysts should utilize highly scannable, structured data matrices rather than dense narrative descriptions.

| Analytical Segment Category | Primary Share Metrics (2025) | Projected Growth Dynamics (CAGR, 2026–2035) | Primary Systemic Growth Drivers |

| North America Region | 34.86% Market Share | Stable Infrastructure Re-investment | Advanced collection grids; rigid compliance monitoring |

| Asia-Pacific Region | Developing Infrastructure Base | 6.95% CAGR (Fastest Regional Sector) | Rapid urban migration; intense industrial manufacturing expansion |

| Collection Service | 62.35% Market Share | Asset Optimization Focus | High capital costs for specialized logistics fleet tracking |

| Disposal Service | Infrastructure Expansion Base | 7.88% CAGR (Fastest Service Sector) | High demand for advanced waste-to-energy plants and landfills |

| Industrial Waste | 86.55% Market Share | Production Volume Alignment | Stringent corporate protocols for handling industrial byproducts |

| E-Waste Type | High-Value Recovery Segment | 9.11% CAGR (Fastest Waste Sector) | Rapid product lifecycles; high electronic components obsolescence |

Benefits of Using Advanced Management Systems

What is the Material and Financial Benefit of Integration?

Transitioning to advanced, software-enabled treatment systems yields profound efficiency gains, cost reductions, and verifiable compliance alignment for major manufacturing facilities. Utilizing Internet-of-Things (IoT) fill-level sensors coupled with predictive algorithmic routing lowers logistics fleet fuel burn metrics, reducing corporate greenhouse gas footprints. Within chemical and material processing plants, deploying advanced separation protocols allows companies to recover expensive catalysts, purifying solvents, and heavy polymer fractions directly from the waste stream. This effectively transforms a traditional corporate liability center into a highly profitable source of secondary circular raw materials.

Market Recent Government Initiatives

What is the Legislative Landscape Governing Global Waste?

Government bodies are rapidly implementing strict regulatory standards to mandate circular processing and limit unchecked environmental dumping. In North America, strict environmental protection updates mandate heavy monitoring of landfill methane emissions alongside aggressive state-level extended producer responsibility (EPR) frameworks targeting packaging and printed paper. Across the European theater, the ongoing execution of the Circular Economy Action Plan forces strict minimum recycled material contents into new polymer products. In India, updated Electronic Waste and Plastic Waste Management Rules enforce clear quantitative collection targets for original manufacturers, driving massive corporate investments into domestic recycling ecosystems.

Competitive Landscape: Top Companies Profiled

What Are the Core Operational Frameworks of Industry Leaders?

WM Intellectual Property Holdings, L.L.C. (Waste Management)

-

About: Headquartered in Houston, Texas, WM operates as the premier provider of comprehensive environmental solutions in North America, managing vast logistics networks and advanced material recovery facilities.

-

Products & Services: Comprehensive solid waste collection, transfer, technical material recycling, resource recovery, and highly engineered landfill gas-to-energy processing operations.

-

Market Capitalization: Approximately USD 92.40 billion (Evaluated Q2 2026).

Republic Services, Inc.

-

About: A dominant force in US environmental services, Republic Services focuses heavily on digitized collection systems and expanding its advanced polymer recycling centers.

-

Products & Services: Municipal and industrial non-hazardous solid waste collection, recycling center operations, specialized hazardous waste treatment, and environmental consultation services.

-

Market Capitalization: Approximately USD 66.37 billion (Evaluated Q2 2026).

Waste Connections, Inc.

-

About: Operating across the US and Canada, Waste Connections deploys an integrated strategy focused on secondary, non-competitive markets and localized disposal asset ownership.

-

Products & Services: Solid waste collection, intermodal transfer rail operations, recycling materials recovery, and specialized oilfield waste discharge processing systems.

-

Market Capitalization: Approximately USD 55.82 billion (Evaluated Q2 2026).

Clean Harbors, Inc.

-

About: The leading provider of industrial environmental services, hazardous waste management, and chemical disposal operations across North America.

-

Products & Services: Chemical packaging, biological destruction, hazardous material incineration, industrial cleaning, and specialized emergency spill response solutions.

-

Market Capitalization: Approximately USD 14.95 billion (Evaluated Q2 2026).

Market Recent Developments by Major Companies

What Strategic Actions are Redefining Corporate Capabilities?

The leading global market players are aggressively pursuing horizontal acquisitions and vertical investments in advanced polymer sorting and chemical recycling infrastructure. A prime example is Waste Management’s systemic investment throughout late 2025 and early 2026 into automated materials recovery facilities, outfitting processing centers with AI-driven optical sorters to achieve high-purity polymer outputs. Concurrently, Republic Services has expanded its dedicated recycling center network, opening specialized polymer hubs designed to process post-consumer plastics into food-grade circular resins. These moves demonstrate an industry-wide pivot toward high-value, technical material recovery as organizations seek to secure reliable, long-term streams of circular raw feedstocks.

Future of the Market

What Long-Term Structural Shift Will Define the Industry?

The future of the waste management market lies in its complete transformation from a linear logistics-focused containment model into a fully realized material-refining industry. Over the next decade, traditional open-air landfilling will be restricted worldwide, replaced by highly integrated closed-loop manufacturing campuses where processing centers sit adjacent to chemical recycling plants. Molecular-level depolymerization and high-efficiency plasma gasification will become standard industrial protocols, allowing facilities to break down mixed waste into elemental synthesis gas and virgin-quality chemical building blocks. Consequently, the sector will evolve into an indispensable hub for secondary raw material sourcing, fundamentally altering global supply chain dynamics.

Why Is the Market Important?

At its core, this market operates as the primary systemic safeguard protecting global ecosystems from catastrophic chemical accumulation while securing the critical material chains required for modern industrial manufacturing. Without highly optimized processing systems, the massive volume of modern industrial and hazardous e-waste would cause permanent soil contamination and irreversible ecological destruction. From a strategic macroeconomic perspective, as primary mineral deposits and petroleum reserves face long-term depletion, this sector provides a highly vital secondary deposit of technical materials. By recovering valuable rare-earth elements, critical metals, and high-performance polymers, the industry mitigates resource scarcity risks and drives sustainable, decoupled economic growth.

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Leave a Reply