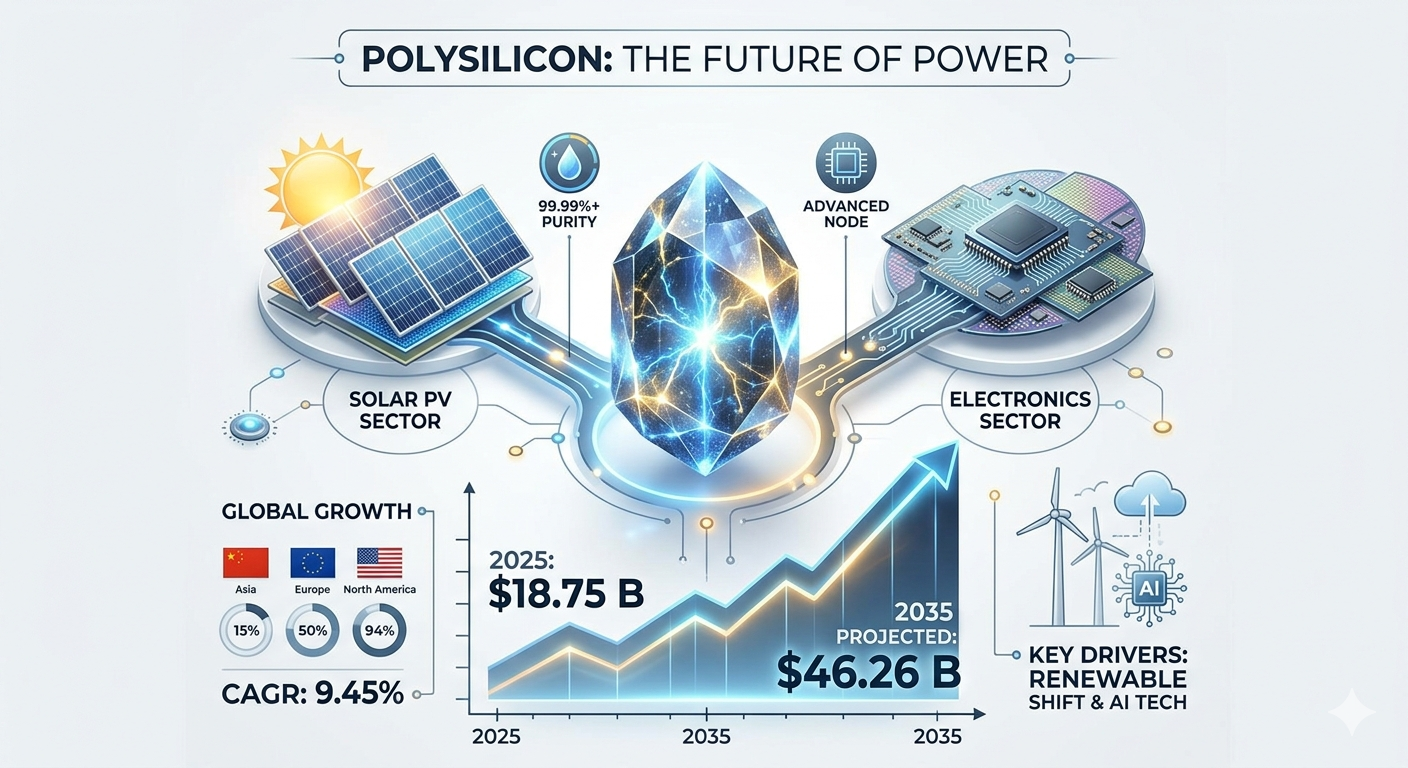

The global polysilicon market represents a critical foundational pillar for both the renewable energy landscape and the advanced microelectronics ecosystem. Valued at USD 18.75 billion in 2025, the market is estimated to reach USD 20.52 billion in 2026. Driven by an unprecedented acceleration in solar photovoltaic (PV) infrastructure and structural expansions in semiconductor fabrication facilities, the market is projected to reach USD 46.26 billion by 2035. This growth reflects a compound annual growth rate (CAGR) of 9.45% over the forecast period from 2026 to 2035. Concurrently, global production volume is expected to scale from 3.45 million tons in 2025 to 8.06 million tons by 2035, exhibiting a volumetric CAGR of 8.85%.

Market Overview

Polycrystalline silicon (polysilicon) serves as the quintessential highly purified precursor material required to produce crystalline silicon ingots, wafers, and subsequent integrated circuits or solar cells. The market encompasses the complete thermodynamic purification value chain, transforming crude metallurgical-grade silicon (MG-Si) through specialized chemical deposition methods into ultra-pure elemental structures. To maintain functional integrity, the material must meet strict purity thresholds: solar-grade polysilicon requires a purity level greater than or equal to 99.9999% (6N), while electronic-grade configurations must achieve an ultra-high purity benchmark of 99.999999999% (11N) to eliminate crystal lattice defects in advanced node logic and memory manufacturing.

Market Dynamics

What Are the Key Factors Driving the Market?

The ongoing global transition toward sustainable energy stands as the primary structural driver of this market. Governments worldwide are enforcing strict decarbonization mandates, driving immense institutional capital into utility-scale solar installations. Additionally, downstream manufacturing trends are shifting rapidly toward high-efficiency photovoltaic architectures, notably Tunnel Oxide Passivated Contact (TOPCon) and Heterojunction Technology (HJT). These advanced cell types require significantly higher volumes of ultra-pure N-type solar-grade polysilicon feedstock.

What Structural Restraints Inhibit Market Expansion?

The primary operational bottleneck is the extreme energy intensity of conventional chemical vapor deposition processes. Polysilicon manufacturing requires substantial electricity inputs, leaving producer margins highly vulnerable to localized power grid price shocks. Furthermore, compliance with strict environmental regulations and carbon border adjustment mechanisms requires heavy capital investments in emissions-scrubbing systems. Additionally, volatile costs for raw materials like high-purity quartz and trichlorosilane (TCS) continue to compress operational margins across the industry.

What Lucrative Opportunities Exist for Industry Players?

Significant commercial opportunities are emerging from the deep integration of artificial intelligence (AI) computing infrastructure and next-generation electric vehicles (EVs). These sectors require an expansive volume of memory chips, advanced microprocessors, and power semiconductors. This demand is encouraging primary producers to expand their capacities for specialized electronics-grade silicon. Furthermore, the rising deployment of machine learning algorithms to simulate and optimize chemical vapor deposition (CVD) reactor mechanics enables modern plants to dramatically reduce production cycles and energy footprints.

Why Is the Polysilicon Market Critical?

Polysilicon serves as the absolute point of origin for dual trillion-dollar secular megatrends: clean electrification and global computing. Without the baseline scalable production of ultra-pure granular or chunk silicon, the manufacturing of advanced microchips, 5G networking modules, and solar photovoltaic systems would stall. It is a critical component of national industrial strategies, prompting regions to heavily incentivize localized processing to protect their supply chains from geopolitical disruptions.

Key Market Trends

-

Onshoring Ingot and Wafer Supply Chains: Solar module manufacturers are increasingly integrating vertically, setting up synchronized wafer-to-module processing plants right next to domestic polysilicon refining hubs.

-

Adoption of Fluidized Bed Reactor (FBR) Technology: Granular polysilicon production via FBR methods is rising rapidly as an alternative to traditional processes, offering up to an 80% reduction in thermal energy consumption.

-

Transition Toward Circular Economy Frameworks: Advanced closed-loop chemical recycling systems are becoming industry standard, designed to reclaim and reprocess silicon kerf loss and end-of-life PV modules.

Market Recent Government Initiatives

Governments worldwide are establishing robust funding mechanisms and strict trade policies to secure domestic polysilicon supply lines. In the United States, targeted direct funding, tax credits, and the active enforcement of Section 301 tariffs—imposing a 50% tariff on imported Chinese polysilicon and wafers—aim to revitalize domestic facilities like REC Silicon’s Moses Lake hub.

Simultaneously, the European Union’s Net-Zero Industry Act (NZIA) integrates non-price criteria regarding environmental sustainability and supply chain resilience into public procurement and renewable energy auctions, effectively discouraging reliance on single-source, high-emission foreign material. In response, China’s Ministry of Commerce (MOFCOM) continues to enforce defensive anti-dumping duties on solar-grade imports from the US and South Korea, shielding its massive domestic refining clusters.

Market Benefits of Using Advanced Grades

Upgrading to next-generation polysilicon processing variants delivers substantial performance advantages to downstream manufacturers. Utilizing ultra-high-purity N-type or advanced node electronic grades minimizes internal carrier recombination velocities within final devices. For solar modules, this translates to heightened conversion efficiencies and reduced light-induced degradation (LID). For semiconductor foundries, ultra-pure raw materials significantly minimize wafer defects during sub-3nm lithography processes, optimizing chip yield per wafer and lowering long-term manufacturing costs.

Market Segments & Predictive Insights

The global polysilicon marketplace is segmented by grade, end-use application, production technology, and geographic region, showing a distinct concentration of volume and revenue across specific product categories.

By Grade Insights

The solar grade segment dominated the market in 2025, capturing an 87.0% share of total revenue due to the massive scale of international green energy installations. However, the electronics grade segment, which held a 13.0% market share in 2025, is projected to expand at the fastest CAGR of 9.80% through 2035. This accelerated growth is driven by the global buildout of advanced chip foundries specializing in dense memory architectures and high-performance logic chip design.

By End-Use Insights

The solar PV cells/modules segment led the market with an 86.0% revenue share in 2025, supported by robust commercial, residential, and utility-scale solar projects. In comparison, the semiconductors segment accounted for an 11.0% revenue share in 2025 and is projected to register the fastest growth with a 10.0% CAGR from 2026 to 2035. This momentum is supported by the increasing electronics content in automotive platforms and industrial automation systems.

By Production Technology Insights

The Siemens process remains the dominant production standard, accounting for 76.0% of the market share in 2025 because of its proven track record in delivering high-purity yields. Conversely, Fluidized Bed Reactor (FBR) technology accounted for an 18.0% share in 2025 and is projected to experience the fastest CAGR of 11.20% up to 2035. This rapid growth is driven by its lower operational energy demands and ability to produce free-flowing granular polysilicon. Upgraded Metallurgical-Grade (UMG) silicon accounted for the remaining 6.0% market share.

Regional Performance Metrics

The comprehensive operational metrics across the primary geographic territories are compiled in the detailed data table below.

Polysilicon Market Regional Performance Indicators (2025–2035)

Competitive Landscape

The competitive environment is characterized by intense consolidation, where the top ten global chemical producers control a significant majority of total refining volume. Strategic focus has shifted from simple capacity additions toward high-value technology investments, such as onshoring electronic-grade production lines and scaling granular FBR output. To navigate strict international trade tariffs, major players are engaging in asset acquisitions, joint ventures, and geographic diversification. This includes establishing new operations in regions with competitive energy costs, such as the Middle East.

Top Key Companies Profiled

1. Wacker Chemie AG

-

About: Wacker Chemie AG is a leading global chemical manufacturer headquartered in Munich, Germany, with a highly specialized focus on high-purity silicone and hyper-pure polycrystalline silicon materials.

-

Products: Electronic-grade hyper-pure silicon chunks, solar-grade monocrystalline feedstock, and specialized trichlorosilane intermediate chemicals.

-

Market Capitalization: Approximately EUR 4.87 billion (as of mid-2026).

2. Daqo New Energy Corp.

-

About: Daqo New Energy Corp. is a leading, low-cost manufacturer of high-purity polysilicon, utilizing advanced automated Siemens processing configurations primarily centered in China.

-

Products: Ultra-pure N-type solar polysilicon chunks, standard P-type monocrystalline solar feedstock, and high-density silicon blocks.

-

Market Capitalization: Approximately USD 1.10 billion (as of mid-2026).

3. OCI Holdings (OCI Company Ltd.)

-

About: Headquartered in South Korea, OCI Holdings is a global green energy and chemical specialist with diversified manufacturing installations spanning Southeast Asia and North America.

-

Products: Semi-conductor grade polysilicon, hyper-pure solar polysilicon, fumed silica, and ultra-pure electronic chemicals.

-

Market Capitalization: Approximately KRW 5.57 trillion (as of mid-2026).

Recent Strategic Developments by Major Companies

-

February 2026 Plant Launch: United Solar Holding officially launched operations at its advanced polysilicon production facility in the Sohar Freezone in Oman. Supplied by equipment specialist Shuangliang Hydrogen, the facility features an annual production capacity of 100,000 tonnes, leveraging competitive regional energy assets.

-

February 2026 M&A Transaction: Top-tier photovoltaic module and polysilicon manufacturer Tongwei Co., Ltd. announced a definitive plan to acquire a 100% equity stake in competitor Qinghai Lihao Clean Energy Co., Ltd. The deal utilizes a structured mix of share issuances and cash to consolidate regional high-purity N-type silicon output.

Future Future Outlook

The polysilicon market is moving toward an automated, highly specialized future. Over the next decade, standard, undifferentiated chemical refining is expected to transition into intelligent, data-driven manufacturing processes. As global computing infrastructure expands alongside international clean energy targets, the demand for ultra-pure N-type solar grade and sub-3nm semiconductor grade material will remain critical. Companies that successfully adopt low-energy production technologies, such as Fluidized Bed Reactors, and utilize AI-driven process automation will be best positioned to lead the global supply chain.

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Leave a Reply