Executive Summary

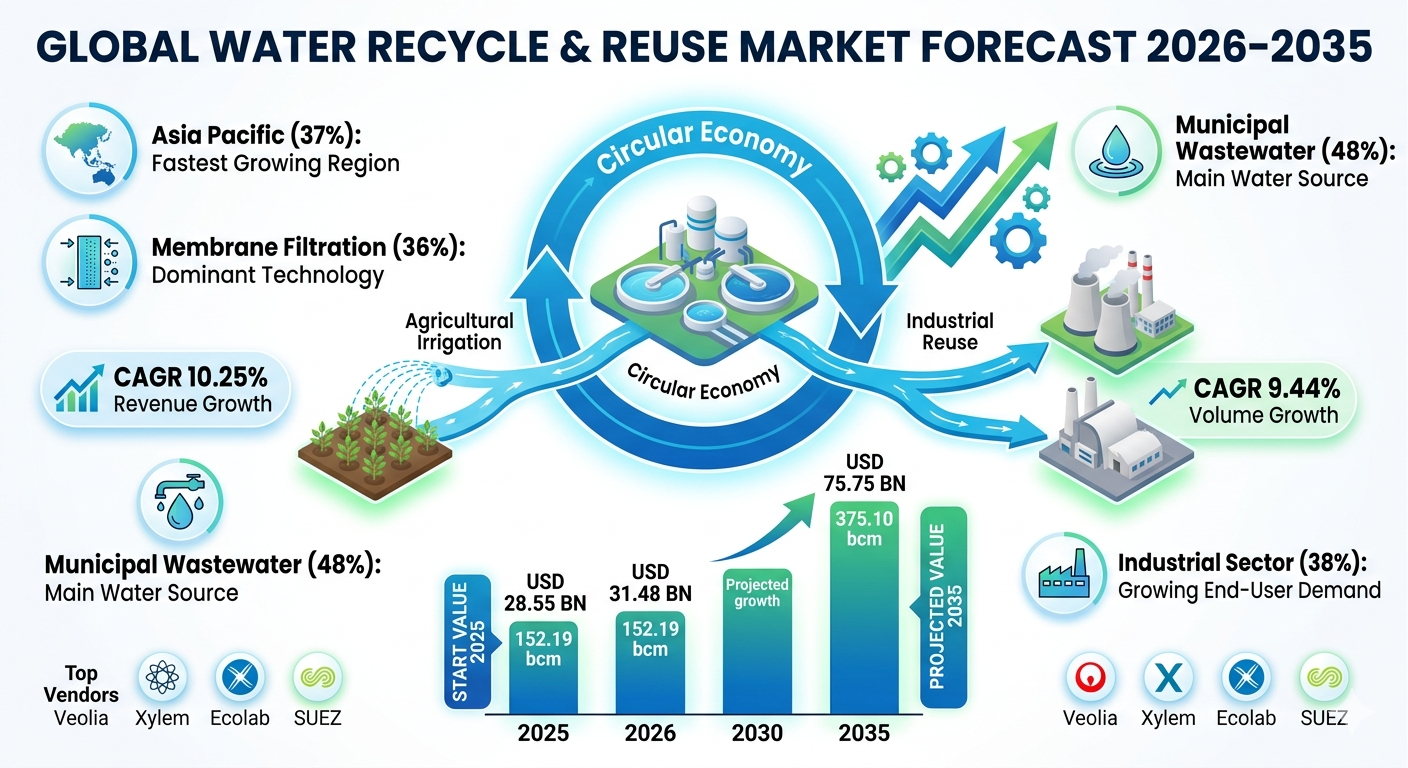

The global water recycle and reuse market is experiencing a period of significant structural growth. Valued at USD 28.55 billion in 2025, the market is estimated to reach USD 31.48 billion in 2026. Driven by an urgent global need for clear, highly efficient water management frameworks, the industry is projected to reach USD 75.75 billion by 2035. This rapid expansion represents a steady CAGR of 10.25% over the forecast period from 2026 to 2035.

In terms of physical capacity, the market volume is projected to scale from 152.19 billion cubic meters in 2025 to 375.10 billion cubic meters by 2035, growing at a volume CAGR of 9.44%. This significant volume expansion underscores a widespread global movement toward closed-loop industrial recycling, infrastructure modernization, and sustainable agriculture irrigation.

Market Overview: What Is the Water Recycle and Reuse Market?

What Is the Core Scope of Water Recycling?

The water recycle and reuse market involves using advanced equipment, physical barriers, chemical processes, and biological systems to treat wastewater so it can be safely used again. Rather than discharging secondary effluent into natural ecosystems, these advanced treatment systems reclaim wastewater for non-potable and potable applications alike.

This industry has shifted away from basic, single-stage treatment methods toward advanced purification systems capable of filtering out microscopic impurities, trace chemicals, industrial toxins, and pathogens. This makes reclaimed water highly reliable and safe for agriculture, industrial processes, and municipal reuse.

Why Is Market Growth Accelerating?

The market’s rapid growth is driven by accelerating water stress worldwide. Rising global populations, shifting weather patterns, and widespread pollution are continuously reducing the availability of fresh water. This scarcity has made traditional fresh water sourcing costly and unreliable for large-scale operations. Consequently, using recycled water has become a financial necessity, offering predictable operation costs and helping industries avoid the high prices associated with sourcing fresh water.

Market Dynamics: Drivers, Restraints, and Opportunities

What Are the Key Factors Driving the Market?

The main factor driving market growth is severe global water stress, coupled with strict wastewater discharge regulations. Industrial sectors are facing intense scrutiny to reduce their overall freshwater intake and limit environmental pollution.

Additionally, manufacturing industries are experiencing rapid production expansions worldwide. Heavy industrial plants require millions of gallons of water daily for cooling towers, boiler feeds, and processing lines. By installing dedicated, on-site recycling plants, these heavy factories can significantly lower operational expenses, shield themselves from local water shortages, and ensure a reliable, continuous water supply.

What Is Hindering Market Adoption?

The primary restraint limiting faster market growth is the high initial cost required to build modern water recycling infrastructure. Setting up advanced membrane filtration networks, automated biological reactors, and distribution pipelines requires significant initial capital.

This high cost barrier often prevents small businesses and rural communities from adopting advanced water recycling systems. Furthermore, managing these complex systems requires specialized engineering skills and trained operators, which are often scarce in developing areas.

Where Do the Primary Opportunities Exist?

Technological innovations are making water recycling systems more cost-effective, energy-efficient, and accessible. These advancements provide significant market opportunities, particularly in developing economies facing severe water shortages.

As the costs of reverse osmosis membranes drop and automated, modular decentralized treatment systems become available, water recycling is becoming viable for smaller communities and decentralizing industrial parks. This enables them to deploy efficient water recycling infrastructure without requiring massive public funding.

Market Benefits of Using Reclaimed Water

Implementing advanced water recycle and reuse systems delivers clear, long-term operational advantages:

-

Substantial Cost Reductions: Reusing treated water significantly lowers industrial spending on expensive municipal fresh water supplies and reduces wastewater discharge fees.

-

Operational Resilience: On-site recycling plants insulate manufacturing facilities from seasonal water shortages, changing weather patterns, and local rationing.

-

Enhanced Environmental Compliance: Closed-loop systems help businesses meet strict wastewater regulations, avoiding costly environmental fines and legal liabilities.

-

Minimized Ecological Footprint: Diverting wastewater away from natural ecosystems helps protect local water bodies from chemical and thermal pollution.

Key Market Segments: Detailed Analytical Breakdown

The global water recycle and reuse market features highly diverse treatment technologies, operational sources, applications, and structural configurations.

Which Segment Accounted for the Largest Market Share?

By technology, the membrane filtration segment dominated the market, holding a 36% share in 2025. This technology is highly preferred because it provides excellent purification by filtering out fine suspended particles, dissolved chemical pollutants, and microscopic organisms. It is also projected to grow at the fastest CAGR of 11.20% through 2035.

By source, municipal wastewater led the market with a 48% share in 2025. This large share is driven by the vast, continuous volume of wastewater generated daily by urban households, schools, and commercial offices. Reclaiming this water is critical for modern urban sanitation and pollution control.

| Market Attribute Dimension | Segment Dominant Champion (2025 Share) | High-Growth Velocity Segment (Projected CAGR) |

| Geographic Region | Asia Pacific (37%) | Asia Pacific (11.60% CAGR) |

| Treatment Technology | Membrane Filtration (36%) | Membrane Filtration (11.20% CAGR) |

| Wastewater Source | Municipal Wastewater (48%) | Industrial Wastewater (10.90% CAGR) |

| Functional Application | Agricultural Irrigation (34%) | Industrial Reuse (10.70% CAGR) |

| System Configuration | Centralized Treatment (58%) | Decentralized Systems (10.90% CAGR) |

| Facility Capacity | Large Scale (>100k $m^3$/day) (43%) | Medium Scale (10k–100k $m^3$/day) (10.80% CAGR) |

| Primary End-User | Municipal Authorities (46%) | Industrial Sector (10.80% CAGR) |

Operational Analysis by Category

-

Biological Treatment (26% Market Share in 2025): Highly valued for its eco-friendly design, this method utilizes specialized microorganisms to break down organic pollutants naturally, requiring less energy and generating fewer chemical by-products.

-

Industrial Wastewater Source (32% Market Share in 2025): Projected to grow at a fast CAGR of 10.90%. This growth is driven by expanding heavy manufacturing facilities that must treat complex chemical wastewater to comply with local environmental rules and lower sourcing costs.

-

Agricultural Irrigation Application (34% Market Share in 2025): The largest application segment, as farmers increasingly use treated reclaimed water to maintain crop production during prolonged dry periods and water shortages.

-

Industrial Reuse Application (28% Market Share in 2025): Expected to grow at a rapid CAGR of 10.70%, fueled by heavy demand for process water, cooling towers, and boiler feed water inside automated factories.

-

Decentralized Systems (42% Market Share in 2025): Growing at a fast CAGR of 10.90%. These systems offer excellent flexibility because they can be installed directly at the source, reducing the need for costly, long-distance pipeline networks.

Regional Analysis: Asia Pacific and North America

How Will Asia Pacific Dominate the Global Market?

The Asia Pacific region led the global market with a 37% share in 2025. Its regional market value is projected to grow from USD 10.56 billion in 2025 to USD 28.41 billion by 2035, expanding at the fastest CAGR of 11.60%. This rapid expansion is driven by fast-growing cities, high population densities, and severe water shortages across emerging economies.

In China, the government is investing heavily in large-scale urban water recycling infrastructure and setting strict pollution controls for its large manufacturing sectors. This strong regulatory environment has made China a key regional hub for advanced water recycling installations.

What Is Driving Long-Term Growth in North America?

North America held a 21% market share in 2025, supported by strong environmental awareness and advanced treatment infrastructure. The United States market is growing steadily due to widespread water stress in arid western states. Both municipalities and industrial sectors in the US are investing heavily in advanced water recycling systems to ensure long-term resource security, optimize operations, and comply with state and federal environmental rules.

Market Recent Government Initiatives

National regulatory bodies are establishing comprehensive frameworks to accelerate the adoption of recycled water:

-

United States: In April 2026, the Environmental Protection Agency (EPA) released its Water Reuse Action Plan (WRAP) 2.0. This update focuses specifically on scaling up water recycling across the industrial, technology, and energy sectors, including developing targeted recycling solutions for AI data center cooling and critical mineral extraction facilities.

-

Europe: The European Commission’s Regulation (EU) 2020/741 on minimum requirements for water reuse mandates strict, harmonized water quality classes (A to D). This regulation ensures safe agricultural irrigation while driving circular economy goals across industrial manufacturing processes.

-

China: The Ministry of Ecology and Environment (MEE) implemented its national-level Regulations on Water Conservation. This framework mandates a 25% wastewater reuse rate in water-scarce urban centers and requires water-saving technological retrofits for high-intensity industrial enterprises.

Competitive Landscape: Top Vendors and Offerings

The global water recycle and reuse market is highly competitive, led by prominent environmental engineering firms, water technology providers, and industrial chemical specialized conglomerates.

Veolia Environnement S.A.

-

About: Headquartered in Paris, France, Veolia is a global leader in environmental services and resource management, operating extensive water and wastewater recovery networks for municipal and industrial clients globally.

-

Products: High-capacity ultrafiltration systems, advanced biological treatment matrices, industrial closed-loop recycling installations, and smart water network optimization systems.

-

Market Capitalization: Approximately EUR 24.6 billion (USD 26.5 billion) (as of May 2026).

Xylem Inc.

-

About: Based in Washington, D.C., Xylem Inc. is a leading global water technology provider focused on solving complex water challenges through smart utility infrastructure and advanced data analytics.

-

Products: Intelligent pumping systems, membrane bioreactors (MBR), advanced UV disinfection systems, ozone treatments, and real-time smart water quality monitoring sensors.

-

Market Capitalization: Approximately USD 26.92 billion (as of May 2026).

Ecolab Inc.

-

About: Operating primarily through its specialized Nalco Water division, Ecolab is a global leader in water management and hygiene services, providing integrated digital and chemical solutions to optimize industrial operations.

-

Products: Custom chemical treatment formulations, water saving automation systems, precise coagulants, advanced oxidation processes, and digital water risk management platforms.

-

Market Capitalization: Approximately USD 70.67 billion (as of May 2026).

Market Recent Developments by Major Companies

Strategic technology integrations are accelerating the deployment of advanced water treatment infrastructure. In April 2026, SUEZ Water Technologies & Solutions and Salinity Solutions launched a major collaborative pilot initiative in southern France. This project deploys a specialized Hybrid Batch Reverse Osmosis system designed to treat municipal wastewater for agricultural and industrial reuse. By utilizing Salinity’s innovative Hy Batch™ technology, the pilot significantly reduces the energy required for reverse osmosis, solving a major historical challenge for membrane filtration systems.

At the same time, major engineering providers are actively embedding advanced IoT sensor arrays into automated decentralized systems. This allows operators to track effluent purity in real time, helping them maintain strict regulatory compliance.

Future of the Market: A Forward-Looking Perspective

The global water recycle and reuse market is moving toward complete automation and integration with digital infrastructure. Driven by rising water scarcity and strict municipal regulations, water treatment is shifting from a standard utility process into an advanced, data-driven manufacturing operation.

The next decade will see widespread adoption of intelligent, decentralized water systems powered by predictive AI analytics. These systems will automatically adjust chemical dosing and membrane pressures based on real-time changes in incoming wastewater quality. Furthermore, the rapid growth of water-intensive sectors, such as AI data center cooling and green hydrogen production, will create new demand for highly reliable, on-site recycling loops. Companies that combine advanced membrane filtration with energy-efficient processing technologies will be well-positioned to lead the global water industry.

Leave a Reply