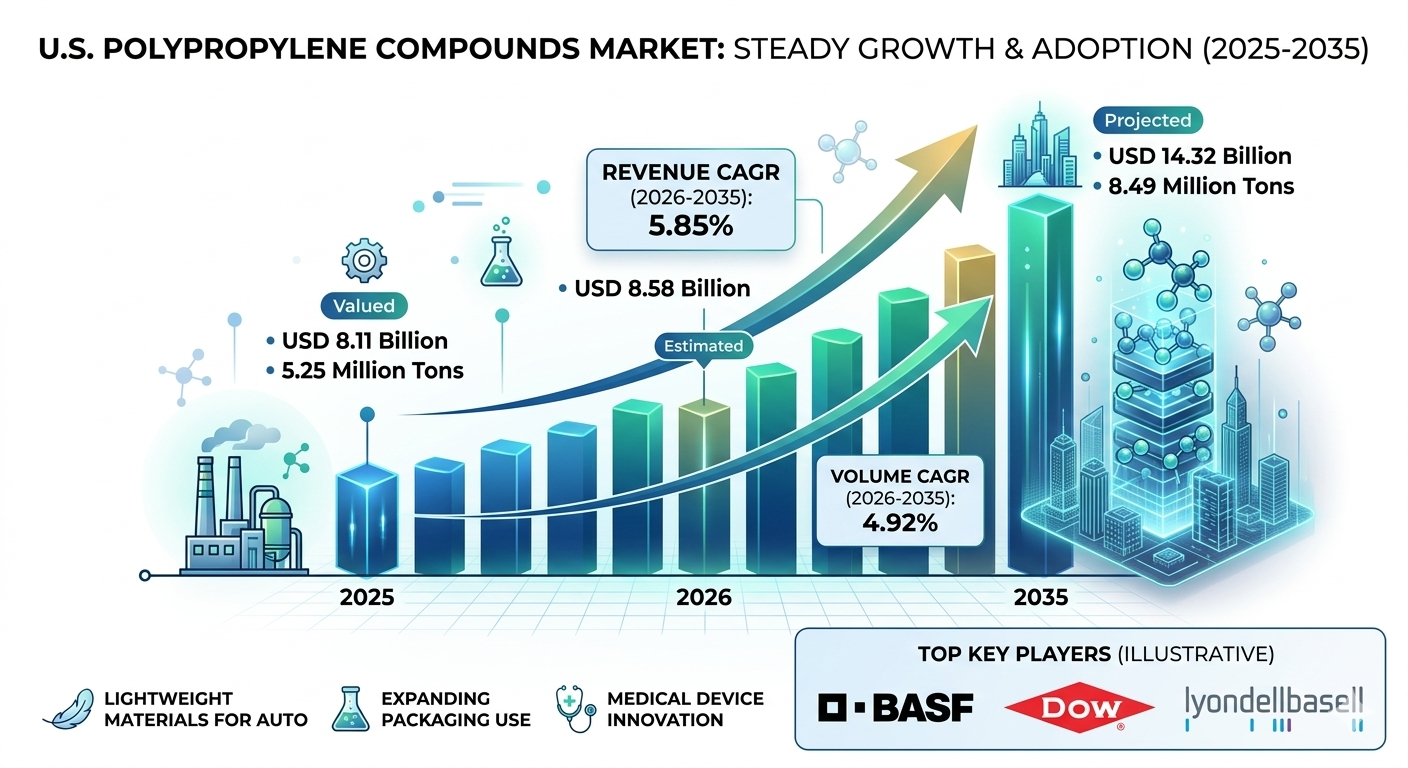

The U.S. polypropylene (PP) compounds market is undergoing a profound structural transformation, driven by industrial engineering demands and rigorous lightweighting initiatives across heavy manufacturing sectors. Valued at USD 8.11 billion in 2025, the market is estimated to reach USD 8.58 billion in 2026. Projections indicate a robust trajectory, with the market expected to expand to USD 14.32 billion by 2035, exhibiting a compound annual growth rate (CAGR) of 5.85% over the forecast period from 2026 to 2035. Utilizing an analytical benchmark for mid-term evaluation, the market value is anticipated to reach approximately USD 12.01 billion by 2032, advancing steadily alongside critical infrastructural and manufacturing shifts.

From a volumetric perspective, demand is anticipated to climb from 5.25 million tons in 2025 to 8.49 million tons by 2035, reflecting a steady volume-based CAGR of 4.92%. This sustained upward trajectory underscores a highly consistent market evolution, fueled by the accelerating substitution of traditional metals and engineering plastics with cost-effective, high-performance polyolefins.

Market Overview: What is the Current State of the Industry?

The U.S. polypropylene compounds market operates as a core foundation for modern material science, bridging bulk petrochemical production with highly specialized end-user requirements. Compounding transforms standard polypropylene resins by incorporating glass fibers, talc, minerals, impact modifiers, and pigments to significantly enhance mechanical, thermal, and chemical capabilities.

Currently, the domestic market is characterized by intense innovation in polymer formulation, shifting dynamically to satisfy the stringent tolerances of automated manufacturing. This growth is anchored by expanding high-speed downstream processing facilities in the American Midwest and South, making custom PP compounding vital to maintaining competitive manufacturing supply chains.

Market Dynamics: What Are the Key Factors Driving the Market?

The market dynamics of this sector are propelled by several multi-industry structural drivers:

-

The Weight Optimization Imperative: Original Equipment Manufacturers (OEMs), particularly in automotive transportation, face intensifying pressure to maximize fuel economy and electric vehicle battery efficiency. Compounded PP serves as an optimal solution to shed vehicle weight without compromising passenger safety.

-

Cost-to-Performance Superiority: Amid fluctuating metal prices and expensive engineering plastics like polyamides, compounded polyolefins deliver equal or superior mechanical durability at a fraction of the raw material cost.

-

Advancements in Custom Formulations: Breakthroughs in coupling agents and nucleating additives have drastically expanded the thermal stable threshold of standard PP, allowing it to penetrate high-heat environments like under-the-hood automotive components and localized electronics arrays.

Market Insights: Why Is the Polypropylene Compounds Market Important?

Polypropylene compounding provides the critical chemical engineering bridge required to solve modern design challenges. Standard resin lacks the rigid structural performance needed for heavy industrial applications, but advanced compounding elevates these materials to compete directly with die-cast aluminum and structurally reinforced structural alloys.

Financially and operationally, it enables scalable, high-speed injection molding production runs that minimize cycle times and down-stream assembly costs. For modern manufacturing systems to remain lean, agile, and efficient, customized polyolefin compounds provide a crucial, highly reproducible baseline material.

Benefits of Using: What are the Primary Structural Advantages?

Integrating advanced polypropylene compounds into production workflows yields distinct operational, engineering, and commercial advantages:

-

Exceptional Strength-to-Weight Ratio: Delivers high tensile strength and high impact resistance while lowering absolute component mass.

-

Superior Processing Efficiency: Demonstrates lower melt temperatures and excellent flowability, accelerating cycle times in complex injection molding tooling.

-

Chemical and Environmental Resilience: Exhibits highly stable resistance to harsh chemical exposure, industrial solvents, moist environments, and oxidative degradation.

-

Design Freedom and Integration: Allows engineers to consolidate complex multi-part component assemblies into unified single-piece injection-molded geometries.

Key Market Trends: What Technological Shifts are Reshaping the Market?

The defining trend reshaping the market is the integration of post-consumer recycled (PCR) content directly into premium automotive and electronic grade compounds without suffering mechanical degradation. Producers are leveraging complex compatibilizers to blend recycled mechanical streams with virgin resin matrix systems safely.

Concurrently, there is an accelerating demand for ultra-high-flow, long-glass-fiber-reinforced (LGF-PP) materials. These advanced compounds are increasingly replacing structural sheets and heavy structural stampings, providing superior energy absorption profiles and high dimensional stability under continuous thermal loading conditions.

Key Segments & Trends: Which Segment Accounted for the Largest Market Share?

The automotive sector continues to dominate the market share landscape, commanding over one-third of the total domestic volume. The ongoing transition to electric vehicle architectures has accelerated the deployment of high-performance PP formulations inside battery enclosures, interior door structural pillars, and complex dash assemblies.

Beyond transportation, the rigid and flexible packaging segment maintains a highly mature, volume-intensive market share, driven by strict food-contact safety standards and high-clarity requirements. In the building and construction sector, compounded polypropylene is rapidly gaining ground, replacing legacy polyvinyl chloride (PVC) and copper configurations in modern commercial piping, moisture barriers, and architectural cladding systems due to its superior environmental footprint and structural resilience.

Market Recent Government Initiatives: What Regulatory Factors Impact Growth?

Federal and state initiatives play an active role in driving polypropylene compound adoption across the United States. Under the Department of Transportation’s updated corporate average fuel economy standards, domestic automakers must continually optimize fleet weight, providing a powerful regulatory push for compound integration.

Furthermore, the U.S. Environmental Protection Agency’s strict directives on reducing volatile organic compound (VOC) emissions from interior components have pushed compounders to develop specialized low-emission, low-odor polypropylene lines. Federal investments directed toward expanding regional recycling networks via infrastructure acts are also securing more consistent pipelines of high-purity PCR resins to support sustainable compounding lines.

Competitive Landscape: Strategic Moves by Key Players

The U.S. competitive arena is defined by backward-integrated petrochemical giants and agile specialty compounders aggressively expanding their portfolios to meet custom industrial demands. Rather than competing purely on a commoditized volume basis, market leaders are securing long-term positions through targeted joint ventures, regional production capacity expansions, and dedicated engineering centers designed to co-develop custom formulations alongside major manufacturing OEMs.

Strategic emphasis is heavily directed toward regional accessibility, minimizing supply chain disruptions by positioning compounding lines within close geographic proximity to automotive manufacturing hubs in the Southeast and Midwest.

LyondellBasell Industries

-

About the Company: Headquartered in Houston, Texas, LyondellBasell stands as one of the world’s largest plastics, chemical, and refining entities, driving polyolefin innovation globally.

-

Products: Hostacom (advanced mineral-reinforced compounds), Hifax (high-impact thermoplastic olefins), and Circulen (compounds featuring high-purity recycled content).

-

Market Cap (May 2026): USD 22.22 billion.

ExxonMobil Corporation

-

About the Company: A premier multinational energy and chemical technology developer, leveraging massive upstream feedstock integration to produce highly consistent base resins and specialized performance compounds.

-

Products: Exceed, Achieve, and Santoprene thermoplastic vulcanizates, alongside automated engineering polypropylene resins engineered for ultra-high melt strength.

-

Market Cap (May 2026): USD 620.96 billion.

SABIC (Saudi Basic Industries Corporation)

-

About the Company: A global leader in diversified chemical manufacturing with massive commercial operations across the U.S., focusing deeply on engineering-grade thermoplastic formulations.

-

Products: Stamax (long glass fiber reinforced polypropylene) and SABIC PP compounds tailored for structural automotive dashboards and heavy structural enclosures.

-

Market Cap (May 2026): USD 45.60 billion.

Avient Corporation

-

About the Company: A specialized, highly agile provider of premier polymer materials, customized formulations, additive color masterbatches, and sustainable chemical solutions.

-

Products: Maxxam (custom engineered PP formulations), OnForce (long-fiber reinforced polyolefins), and specialized bio-filled composite arrays.

-

Market Cap (May 2026): USD 3.15 billion.

Data Presentation: Market Metric Highlights and Strategic Projections

To optimize manufacturing roadmaps, engineering teams must cross-reference volumetric demands with long-term compound performance characteristics. The following structured data table charts the essential historical and projected metrics tracking the expansion of the domestic industry

Leave a Reply