Executive Summary

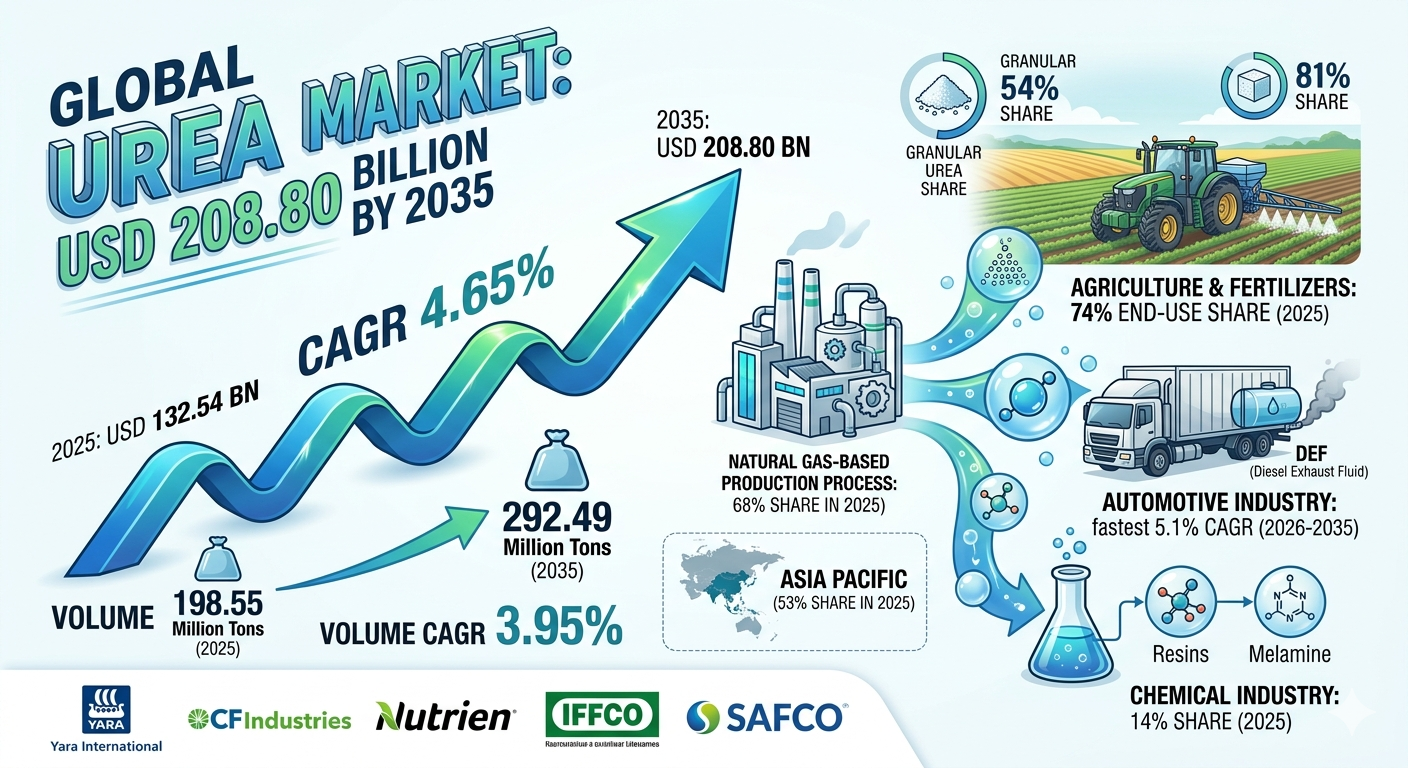

The stabilization and expansion of global crop yields remain fundamentally anchored to nitrogen-based chemical processing inputs. The global urea market size was estimated at USD 132.54 billion in 2025 and is projected to reach USD 208.80 billion by 2035. Over the forecast period from 2026 to 2035, this critical commodities sector is poised to grow at a Compound Annual Growth Rate (CAGR) of 4.65%.

In terms of material volume, the industry is anticipated to scale from 198.55 million tons in 2025 to 292.49 million tons by 2035, exhibiting a volumetric CAGR of 3.95%. This long-term macroeconomic progression is primarily driven by escalating international demand for high-nitrogen fertilizers to sustain staple farming infrastructures, balanced with high-growth specialty segments in automotive emission control and bio-based industrial synthesis.

Market Overview & Architectural Significance

Why Is Market Importance Critical to Global Agriculture?

The urea market represents a non-negotiable cornerstone for global food security, serving as the planet’s primary solid nitrogen-based crop nutrient (boasting a concentrated 46% nitrogen payload). In an era marked by shifting climatic patterns and rapidly shrinking arable land per capita, maximizing the yield per hectare of essential staple crops—specifically rice, wheat, and corn—is impossible without scalable urea deployment.

Beyond its foundational 70%+ structural integration into farming, urea functions as a primary chemical intermediate. It serves as a core component in the formulation of modern industrial adhesives, animal feed supplements, and specialty Diesel Exhaust Fluids (DEF) that actively lower toxic nitrogen oxide ($NO_x$) emissions within high-displacement internal combustion powertrains.

What Is Market Growth Materializing From?

Market growth is materializing from a synchronized expansion across both developing agricultural boundaries and modern industrial sectors. Demographically, surging population densities across the Asia-Pacific and African continents mandate aggressive fertilizer application rates, heavily supported by government subsidy networks to isolate localized crop prices from global inflation shocks. Concurrently, stricter regulatory ceilings placed on heavy-duty diesel engines globally are forcing an exponential rise in automotive-grade prill consumption for AdBlue/DEF fluid production.

Technical Framework and In-Depth Market Dynamics

What Are the Key Factors Driving The Market?

-

Surging Global Food Security Requirements: Expanding crop production to feed an escalating global populace relies heavily on urea due to its high nutrient concentration and unparalleled cost-efficiency compared to alternative ammoniacal options.

-

Mandatory Adoption of Automotive Emission Defoamers: Rapidly growing heavy-duty transport fleets and stringent emission rules (such as Euro VI and BS VI) require high-purity urea-water solutions (DEF/AdBlue) to fuel Selective Catalytic Reduction (SCR) setups.

-

Agronomic Pivot Toward Controlled-Release Technologies: The development and premium adoption of sulfur-coated, polymer-coated, and water-soluble urea variants dramatically improve nitrogen use efficiency, limiting environmental runoff.

What Are the Primary Restraints Limiting Expansion?

-

Feedstock Natural Gas Volatility & Environmental Restraints: Conventional urea production depends entirely on the reaction of carbon dioxide and ammonia synthesized via energy-dense natural gas cracking. This introduces massive operational margin exposures to fuel price spikes. Furthermore, strict ecological mandates regulating nitrogen runoff into aquatic ecosystems and ammonia air emissions place severe operational limits on legacy processing assets.

What Is the Core Future Opportunity in the Sector?

-

Decarbonization Through Green and Blue Ammonia Engineering: Transitioning existing synthetic infrastructures toward utilizing green ammonia (hydrogen derived via water electrolysis using renewable energy grids) aligns directly with global ESG compliance. This shift allows manufacturing entities to command strong price premiums while shielding their supply chains from carbon border adjustment taxes.

Key Market Trends & Advanced Technological Shifts

What Is the Impact of Sustainable Technical Shifts?

The urea landscape is undergoing an extensive structural realignment away from carbon-heavy, legacy industrial processes. The primary emphasis has shifted toward integrating “green” and “blue” ammonia manufacturing loops, which actively capture and utilize byproduct carbon dioxide right at the assembly source.

Simultaneously, nanotechnology is making significant commercial inroads, highlighted by the successful integration of liquid nano-urea solutions. These liquid formulations allow direct foliar spraying, allowing plants to absorb nutrients straight through their leaves. This technique drastically cuts down the traditional volume requirements of bulk solid fertilizers while minimizing underground soil contamination.

What Is the Role of Modern Logistics and Digitalization?

Digital procurement, localized micro-plant configurations, and advanced e-commerce distribution channels are rapidly reshaping last-mile farm deliveries. Precision agriculture setups use real-time soil sensor networks to determine exact nutrient deficiencies. This allows distributors to deliver customized granular blends directly to agricultural cooperatives, helping prevent the over-application of fertilizers.

Segmental Architecture & Dominant Market Shares

Which Segment Accounted for the Largest Market Share?

The Granular Urea segment dominated the marketplace, commanding 54% of the global revenue share in 2025, and is anticipated to post the fastest product growth at a 4.8% CAGR. This dominance is underpinned by its superior physical robustness, reduced caking tendencies, and optimized suitability for bulk mechanized blending and variable-rate pneumatic spreading systems compared to legacy prilled alternatives.

-

Prilled Urea (32% Share in 2025): Remains a highly cost-effective, rapidly dissolving choice preferred across standard agricultural broadcasting and industrial chemical processing lines.

-

Liquid Urea (14% Share in 2025): Expanding steadily at a 4.9% CAGR, heavily propelled by the adoption of fertigation and precision foliar spray techniques.

Application, End-Use, and Production Breakdown

-

Fertilizers & Agriculture (72% and 74% Shares in 2025): The undisputed structural anchors of the global demand curve, driven by intensive cultivation requirements for staple grain crops.

-

Automotive Industry (7% End-Use Share in 2025): Registering the fastest sector expansion with a 5.1% CAGR, powered directly by the global enforcement of diesel SCR exhaust mandates.

-

Natural Gas-Based Production (68% Share in 2025): Continues its absolute dominance due to its highly optimized cost-to-volume ratio, although the Biomass-Based segment (5% share) is growing the fastest at a 5.8% CAGR due to decarbonization targets.

Global Urea Market Value, Volume, and Pricing Forecast

| Attribute | 2025 (Base Year) | 2026 (Forecast Start) | 2035 (Target Forecast) | Sector CAGR (2026–2035) |

| Market Value (USD) | $132.54 Billion | $138.70 Billion | $208.80 Billion | 4.65% |

| Market Volume (Tons) | 198.55 Million | 206.39 Million | 292.49 Million | 3.95% |

| Avg. Mfg Price / Ton | $220 | — | — | Pricing CAGR: |

| Avg. Selling Price / Ton | $330 | — | — | 2.85% |

Regional Analysis: Geographic Consolidation

How Did Asia-Pacific Dominate the Urea Market?

The Asia-Pacific region represents the core engine of the global urea market, securing a massive 53% market share in 2025. Valued at USD 70.25 billion in 2025, the regional market is on track to hit USD 111.71 billion by 2035, progressing at a steady 5.0% CAGR.

This absolute dominance is fueled by the vast agricultural foundations of China and India, coupled with extensive government subsidy networks that keep urea affordable for smallholder farmers. India’s aggressive focus on expanding domestic production through its New Investment Policy (NIP), alongside the rollout of commercial nano-urea facilities, is actively working to reduce the region’s reliance on imports.

North American Growth Metrics

North America held a 16% market share in 2025. This regional market is heavily shaped by highly consolidated, large-scale commercial farming operations that utilize premium granular configurations. Production here is highly cost-competitive, backed by steady access to cheap domestic shale gas reserves. This abundant supply acts as a reliable buffer against foreign import vulnerabilities.

Market Recent Government Initiatives

Global state policies heavily dictate market accessibility and chemical composition metrics:

-

India (Department of Fertilizers): Maintains strict regulatory controls via the Fertilizer Control Order (FCO) and channels substantial fiscal subsidies directly into local manufacturing loops to achieve absolute import independence.

-

European Union (European Commission): Enforces the stringent Nitrates Directive and Fertilising Products Regulation (EU 2019/1009). These frameworks place definitive ceilings on total nitrogen soil application rates while actively promoting eco-labeled, low-carbon fertilizer options.

-

China (Ministry of Agriculture and Rural Affairs): Implements targeted fertilizer zero-growth policies and strict registration laws aimed at optimizing nitrogen use efficiency and curbing widespread agricultural pollution.

Competitive Landscape & Top Companies

The global competitive landscape is defined by large-scale consolidation, with top companies investing heavily in low-carbon production assets and international supply chain logstitics. Below is an analytical overview of key market participants:

1. CF Industries Holdings, Inc.

-

About: A prominent global manufacturer of hydrogen and nitrogen products, headquartered in Deerfield, Illinois, USA. The company operates massive, highly integrated production networks across North America.

-

Products: Granular urea, Ammonia, Urea Ammonium Nitrate (UAN), and high-purity Diesel Exhaust Fluid (DEF).

-

Market Capitalization: Approximately USD 19.74 Billion (as of May 2026).

2. Nutrien Ltd.

-

About: Headquartered in Saskatoon, Canada, Nutrien is a premier global provider of crop inputs and services, managing an unmatched agricultural retail network that serves over half a million producers globally.

-

Products: Standard and premium coated granular urea, anhydrous ammonia, nitrogen solutions, potash, and phosphate nutrients.

-

Market Capitalization: Approximately USD 33.83 Billion (as of May 2026).

3. Yara International ASA

-

About: Based in Oslo, Norway, Yara is a world-leading crop nutrition and industrial nitrogen firm. The company is deeply committed to driving a fit-for-future business model centered on sustainable green ammonia synthesis.

-

Products: YaraVera® urea fertilizers, legal-grade AdBlue emissions fluid, controlled-release crop nutrients, and digital precision farming tools.

-

Market Capitalization: Approximately NOK 133.42 Billion (~USD 12.5 Billion) (as of May 2026).

What Is the Status of Recent Strategic Market Developments?

-

May 2026: S&P Global Commodity Insights (Platts) announced the upcoming launch of a daily FOB Nigeria granular urea price assessment. This index specifically targets spot volumes of 30,000 to 50,000 metric tons shipping from key West African hubs like Lekki and Onne, bringing vital transparency to this rapidly growing nitrogen export hub.

-

October 2025: United Capital Fertilizer completed a landmark USD 641 million investment to launch Zambia’s first-ever domestic urea manufacturing facility. This asset is strategically designed to boost regional food security and eliminate import dependency, with a Phase 2 expansion already planned to double output for neighboring export markets.

Future Horizon: The Strategic Outlook

The future of the global urea market will be defined by a careful balance between ensuring global food security and meeting strict decarbonization targets. While standard solid prilled configurations will likely maintain their volume dominance in developing agricultural hubs, long-term commercial success will favor manufacturers that successfully transition to green ammonia processing methods.

Over the coming decade, the industry will reward technical efficiency over raw output. Companies that focus on high-efficiency coated granules, liquid nano-formulations, and high-purity automotive fluids will successfully insulate their business models from natural gas price shocks, securing a resilient positions in the global agricultural and industrial supply chains.

Leave a Reply