According to Towards Chemicals And Materials Analytics and Consulting, The global materials sector is undergoing a profound structural evolution. No longer confined to traditional petrochemical synthesis, the industry is transitioning into an era of predictive molecular design, circular chemical systems, and aggressive carbon-mitigation strategies. As regulatory frameworks tighten globally, the demand for application-specific, high-performance specialty materials is accelerating. This report provides an in-depth analysis of the market’s trajectory, key segments, and competitive dynamics.

Executive Summary

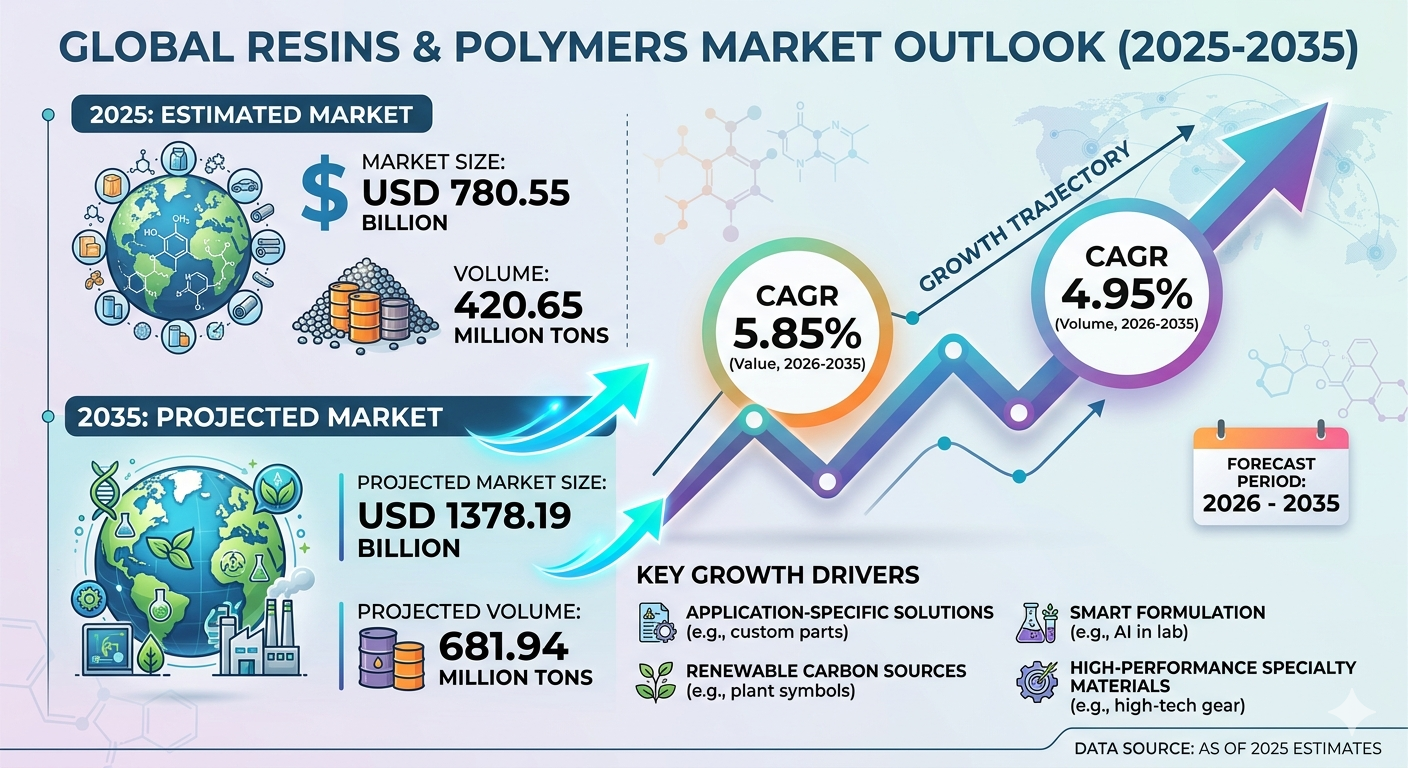

The global Resins and Polymers market represents a cornerstone of modern industrial manufacturing, serving as an indispensable foundation for the automotive, aerospace, packaging, construction, and telecommunications sectors. Valued at USD 780.55 billion in 2025, the market is on a firm trajectory to reach USD 1,378.19 billion by 2035. This expansion represents a steady Compound Annual Growth Rate (CAGR) of 5.85% during the forecast period from 2026 to 2035.

In terms of physical volume, the market is projected to expand from 420.65 million tons in 2025 to 681.94 million tons by 2035, growing at a volume CAGR of 4.95%. The delta between value and volume growth underscores a significant macroeconomic trend: the rising premium on high-performance specialty grades, smart formulations, and bio-based alternatives.

Market Overview: Why Is This Market Important?

Resins and polymers are the unsustainability-redefining, structural workhorses of the global economy. They dictate the performance boundaries of everyday products and advanced industrial systems alike. Today, the market is defined by a dual mandate: advancing molecular science innovation while managing absolute lifecycle responsibility.

The industrial shift toward the “de-petrolization” of feedstocks is forcing a re-engineering of classic polymer chains. Manufacturers are heavily investing in supply chain decarbonization and the integration of renewable carbon sources to decouple production from volatile fossil fuel markets. From enabling the lightweighting of electric vehicles (EVs) to providing high-frequency dielectric precision for 5G/6G infrastructure, these materials are the silent enablers of next-generation technological ecosystems.

Market Dynamics: What Are the Key Factors Driving the Market?

What are the Primary Drivers for This Market?

-

The Shift to Water-Borne Systems: To comply with increasingly stringent low-VOC (volatile organic compound) mandates, the chemical industry is accelerating its transition toward water-based resin systems. This shift is particularly pronounced in advanced coatings and structural adhesives.

-

Automotive Lightweighting and EV Adoption: The global transition to electric mobility requires radical weight reduction to optimize battery range. High-performance engineering plastics and thermosetting composites are replacing traditional metal components under the hood, in structural frames, and within battery enclosures.

-

E-Commerce and Mono-Material Packaging: The sustained expansion of global e-commerce has maintained massive demand for flexible and rigid packaging. Innovation here is focused on mono-material structures (such as pure polyethylene lines) that dramatically simplify mechanical recycling.

What are the Main Restraints Limiting Growth?

-

Upstream Feedstock Volatility: Because 82% of the market remains anchored to petrochemical feedstocks, manufacturer margins are highly vulnerable to crude oil and natural gas price shocks.

-

Infrastructure Gaps in Emerging Economies: While advanced recycling regulations are expanding, the physical infrastructure required for high-purity post-consumer resin (PCR) recovery remains inadequate across many developing industrial hubs, limiting the supply of circular materials.

Comprehensive Segmental Insights

Which Segment Accounted for the Largest Market Share?

The Thermoplastics segment dominated the global market, holding a 52% share in 2025. This dominance is driven by their inherent thermal plasticity—the capability to melt, form, and remelt through dynamic processing without chemical degradation. This trait makes materials like Polyethylene (PE), Polypropylene (PP), and Polyvinyl Chloride (PVC) vital to the realization of a closed-loop economy.

Conversely, Thermosetting Resins held a 30% share in 2025 but are projected to grow at the fastest value CAGR of 5.9%. This rapid growth is fueled by their superior molecular cross-linking, which provides unmatched thermal fatigue resistance and creep resistance in high-durability composites, electronic circuitry, and structural laminates. Elastomers captured the remaining 18% share, valued for their energy dissipation and high-pressure sealing capabilities.

Analysis of Source, Form, and Application Segments

-

Source: Petrochemical-based feedstocks held 82% of the market in 2025 due to their established cost efficiencies and structural stability. However, the Bio-based segment (18% share) is growing at a rapid CAGR of 8.7%, driven by the commercialization of PLA, PHA, and bio-equivalent polyolefins (Bio-PE/Bio-PET).

-

Form: Solid forms (granules, pellets, and beads) led the market with a 58% share due to their long-term storage stability and handling precision in automated systems. The Liquid segment (27% share) is growing at 6.1% CAGR, driven by uniform thin-film engineering in coatings and encapsulants. Powders comprised 15% of the market, expanding into advanced additive manufacturing like selective laser sintering (SLS).

-

Application: Packaging remained the primary application matrix at 34% of total market share. Construction held 22%, utilizing advanced polymer membranes for green building insulation. Automotive applications stood at 16% but represent the fastest-growing application segment at a 6.3% CAGR. Electrical & Electronics accounted for 12%, with the remaining 16% distributed across consumer and industrial applications.

Global and Regional Analysis

How Did Asia-Pacific Dominate the Market in 2025?

The Asia-Pacific region held a commanding 46% share of the global market in 2025 and is projected to expand at the fastest CAGR of 6.4%. The region acts as both the world’s primary resin synthesis powerhouse and its largest polymer conversion hub. China maintains structural leadership through massive capacity expansions in baseline ethylene and propylene, alongside a fast-evolving domestic shift toward specialty material self-sufficiency for green energy and consumer electronics.

North American Growth Trends

North America secured a 20% market share in 2025 and is forecasted to grow at a 5.10% CAGR. The region leverages its massive shale-gas infrastructure, providing a low-cost, natural gas liquid (NGL) feedstock advantage. Innovation in the United States is focused on high-specification material engineering for the aerospace, defense, and medical-grade polymer sectors, heavily backed by investments in advanced chemical (molecular) recycling infrastructure.

Key Market Trends & Technological Shifts

The industry is actively transitioning from empirical, trial-and-error chemistry to predictive molecular design.

The Rise of AI and Autonomous Laboratories

Machine learning models are radically compressing the R&D lifecycles required to discover novel polymer formulations. By simulating molecular combinations under varied stress states, AI enables the rapid deployment of custom, application-specific specialty resins. Furthermore, chemical conglomerates are adopting cognitive supply chain architectures to insulate operations from raw material price volatility, utilizing real-time predictive analytics to manage feedstock hedging.

What are the Key Benefits of Using Modern Specialty Polymers?

Modern engineered resins deliver highly precise performance traits, including customized dielectric constants for telecommunications, advanced barrier properties for food preservation without added mass, and superior strength-to-weight ratios that directly reduce carbon emissions in transportation applications.

Competitive Landscape & Top Companies

The global resins and polymers landscape is highly consolidated among a select group of chemical conglomerates. Success is increasingly determined by patent portfolios in specialty polymers, access to bio-feedstocks, and large-scale regional manufacturing efficiencies.

1. SABIC (Saudi Basic Industries Corporation)

-

About: Headquartered in Riyadh, Saudi Arabia, SABIC is a diversified chemical leader, with Aramco holding a majority stake. It operates across more than 50 countries.

-

Products: Broad portfolio including LEXAN™ (polycarbonate), CYCOLOY™ (PC/ABS blends), ultra-high-molecular-weight polyethylene, and specialized polyolefins.

-

Market Cap: Approximately USD 72 Billion.

2. BASF SE

-

About: Based in Ludwigshafen, Germany, BASF is the world’s largest chemical producer, utilizing highly integrated “Verbund” production sites to optimize resource efficiency.

-

Products: Ultramid® (polyamides), Ultradur® (PBT), advanced polyurethane systems, engineering plastics, and functional coating resins.

-

Market Cap: Approximately USD 45 Billion.

3. LyondellBasell Industries N.V.

-

About: A multinational chemical company incorporated in the Netherlands with operational headquarters in Houston, Texas. It is one of the world’s largest plastics, chemical, and refining companies.

-

Products: Global leader in polypropylene (PP) and polyethylene (PE) technologies, advanced polyolefin components, and Catalloy process resins.

-

Market Cap: Approximately USD 31 Billion.

4. DuPont de Nemours, Inc.

-

About: A premier US-based specialty materials company focused on high-technology applications across electronics, water, protection, and industrial fields.

-

Products: Kapton® polyimide films, Nomex® and Kevlar® aramid polymers, and specialty electronic resins.

-

Market Cap: Approximately USD 36 Billion.

5. Arkema SA

-

About: A French specialty chemicals and advanced materials company headquartered in Colombes, structured around Adhesive Solutions, Advanced Materials, and Coating Solutions.

-

Products: Rilsan® bio-polyamide 11, Kynar® PVDF fluoropolymers, and Foral® specialty tackifying resins.

-

Market Cap: Approximately USD 7.5 Billion.

What is the Future of the Market?

The future of the Resins and Polymers market lies in true chemical circularity. Over the next decade, the industry will likely see mechanical recycling supplemented—and in some areas surpassed—by advanced molecular recycling (pyrolysis and depolymerization). This transition will allow post-consumer waste to be broken down into its base monomers and rebuilt into virgin-quality resins infinitely.

Furthermore, as AI-guided autonomous synthesis matures, the time required to bring a specialized polymer from a lab concept to commercial scale will drop significantly. Companies that master the integration of bio-based feedstocks into existing high-throughput manufacturing lines without sacrificing performance will capture the definitive share of this USD 1.37+ trillion marketplace.

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Email: [email protected]

Leave a Reply