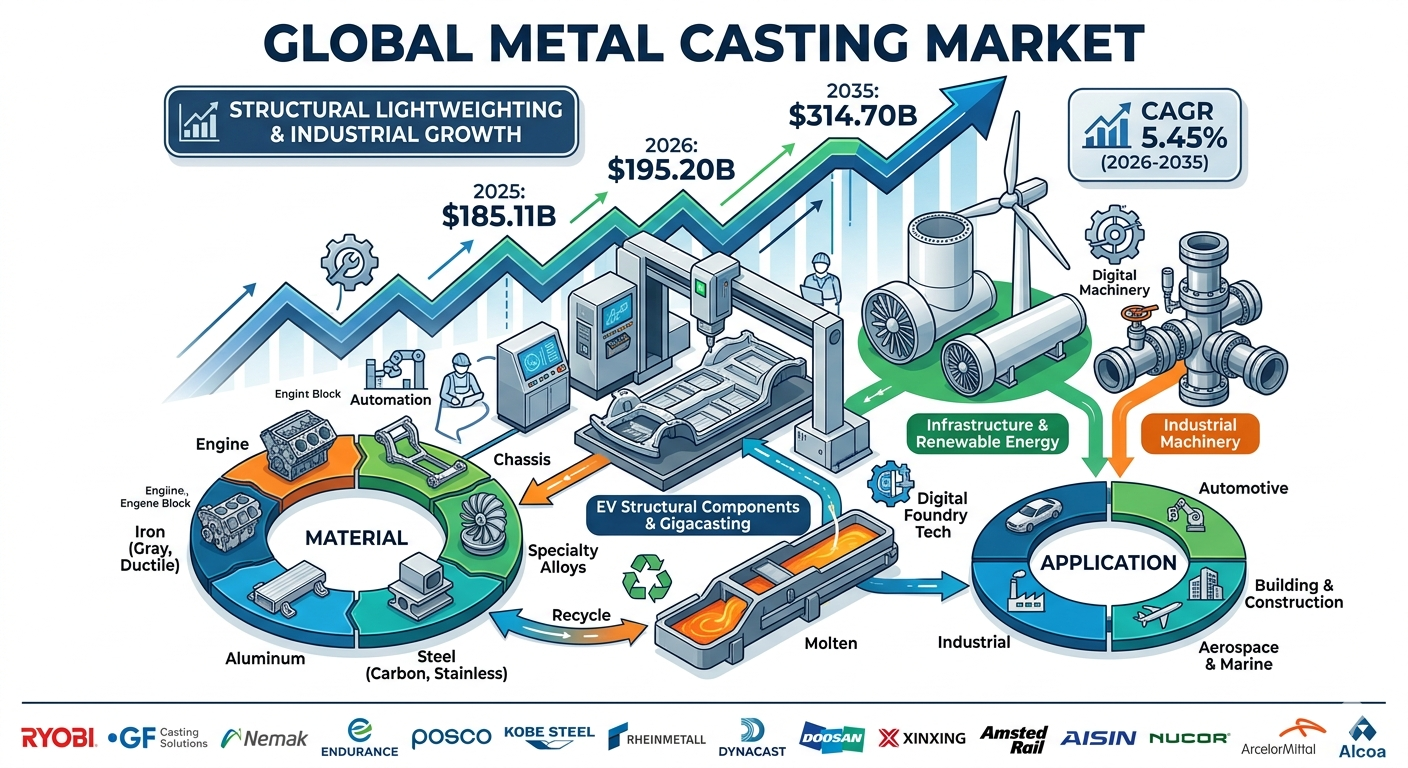

The structural layout of modern manufacturing networks has repositioned metal solidification processes as a core driver of modern component fabrication. Valued at USD 185.11 billion in 2025, the global metal casting market is estimated to reach USD 195.20 billion in 2026. Propelled by the rapid adoption of automated gigacasting methodologies in electric vehicle (EV) structural framing, global infrastructure developments, and advanced component optimization, the market is projected to expand to USD 314.70 billion by 2035. This multi-year expansion represents a steady CAGR of 5.45% from 2026 to 2035, emphasizing the critical role of custom cast alloys in international supply chains.

Market Overview: Why Is the Metal Casting Market Important?

Metal casting—the process of pouring liquid molten metal into structured molds to solidify into complex geometric components—remains an irreplaceable foundational layer of global manufacturing.

This process allows industries to produce intricate components with internal cavities, variable wall thicknesses, and high structural integrity that would be cost-prohibitive or impossible to fabricate via standard CNC machining or welding. From massive industrial valve bodies and mining crushers to thin-walled aluminum battery enclosures for modern electric vehicle powertrains, casting provides a highly cost-effective path to mass production. It minimizes raw material waste while allowing engineers to integrate multiple components into single, unified castings that lower overall assembly costs.

Market Dynamics: What Are the Key Factors Driving the Market?

Structural Drivers and Economic Motivation

-

The Gigacasting Shift in Automotive Production: Next-generation vehicle architecture is heavily built around mega-casting and giga-casting methods. Automakers are using massive high-pressure die-casting machines to cast large sections of vehicle underbodies as single pieces, significantly reducing factory footprints and structural component counts.

-

Widespread Modernization of Global Power Grids: The expansion of renewable energy systems requires millions of high-durability cast parts. Wind turbine gearboxes, generator housings, and heavy-duty fluid control valves require high-performance ductile iron and alloy steel castings to endure severe outdoor operational environments.

Restraints and Technical Challenges

-

Rising Operational Costs and Energy Volatility: Operating foundry furnaces requires significant energy inputs. Sharp fluctuations in electricity and natural gas pricing directly pressure the profit margins of mid-tier casting facilities.

-

Stringent Air Quality and Emissions Regulations: Foundries face intense scrutiny from international environmental agencies over particulate matter and greenhouse gas outputs. Meeting these strict standards requires heavy capital spending on advanced smoke scrubber installations and energy-efficient induction furnaces.

Market Segments: Which Segment Accounted for the Largest Market Share?

By Material: Iron Castings Command Volumetric Presence

The metal casting market is segmented by material chemistry, dividing into Iron (Gray, Ductile, Malleable), Steel (Carbon, Alloy, Stainless), Aluminum (Sand, Die, Permanent Mold), and specialized non-ferrous alloys. Iron castings—specifically gray and ductile variations—accounted for the largest volumetric share, owing to their dampening qualities, wear resistance, and low production costs across the industrial machinery and municipal pipe sectors.

Simultaneously, aluminum die casting is emerging as the fastest-growing financial sub-segment, driven by global automotive weight-reduction initiatives.

By Application: Automotive Integration Secures Lead Shares

The Automotive sector holds the dominant application market share. It relies heavily on high-precision castings for transmission systems, structural shock towers, steering knuckles, and engine blocks.

The Industrial Machinery and Building & Construction segments also serve as vital market pillars. They require large volumes of ductile iron pipes, fittings, architectural structural parts, and heavy mining equipment components to sustain global infrastructure development.

Data Presentation: Sector Growth and Tonnage Projections

The physical production volume of international foundry operations tracks a steady upward trajectory. The table below outlines this scaling from 127.11 million tons in 2025 to 204.11 million tons by 2035, growing at a volume CAGR of 4.85%.

| Reference Year | Market Valuation (USD Billion) | Physical Volume Throughput (Million Tons) | Primary Industry Segment Driver |

| 2025 | 185.11 | 127.11 | Widespread usage of conventional gray iron and sand-cast construction materials. |

| 2026 | 195.20 | 132.27 | Rising deployment of high-pressure die-cast aluminum within hybrid and EV platforms. |

| 2035 (F) | 314.70 | 204.11 | Widespread adoption of advanced automation and near-net-shape alloy processes. |

Regional Insights: What Is the Regional Growth Architecture?

The Asia-Pacific region dominated the global metal casting market, holding a 53% revenue share in 2025, and is projected to expand at the fastest CAGR of 5.55% through 2035. This massive regional position is sustained by China, India, and Japan.

China functions as the global center for casting production, running thousands of automated foundries that supply domestic automotive factories, infrastructure networks, and machine tool shops. India’s casting sector is also seeing notable growth, driven by domestic infrastructure investments and growing automotive component exports.

What Are the Market’s Recent Government Initiatives?

Foundry operators worldwide must continually adapt to a evolving landscape of national industrial policies:

-

The European Union’s Carbon Border Adjustment Mechanism (CBAM): This policy imposes carbon tariffs on imported iron and steel components, forcing non-EU foundries to implement cleaner melting practices to protect their export margins.

-

The US Infrastructure Investment and Jobs Act: This legislation mandates strict “Build America, Buy America” compliance. It requires that iron and steel castings used in federal transit, water management, and infrastructure projects be poured domestically.

-

Indian National Manufacturing Policies: Government incentives like the Production Linked Incentive (PLI) scheme for auto components encourage foundries to upgrade to advanced, low-emission aluminum die-casting technologies.

Competitive Landscape: Top Companies and Strategic Movements

The global casting sector features a mix of massive steel and aluminum conglomerates operating next to specialized, highly advanced auto component manufacturers. To thrive in a margin-sensitive market, top companies are expanding beyond basic cast parts. They are investing heavily in secondary machining, heat treatments, and surface coatings to deliver ready-to-assemble, high-margin sub-assemblies directly to final assembly lines. Strategic acquisitions are heavily focused on buying advanced high-pressure die-casting facilities to quickly secure supply contracts for upcoming EV manufacturing platforms.

Ryobi Limited

-

About: Ryobi Limited is a Japanese manufacturing powerhouse that sets global standards for precision aluminum die-casting technology.

-

Key Products: Thin-walled automotive engine blocks, highly complex transmission cases, structural chassis mounts, and lightweight vehicle subframes.

-

Market Capitalization: Approximately JPY 83.02 Billion as of mid-2026.

GF Casting Solutions (Georg Fischer)

-

About: A specialized division of Switzerland’s Georg Fischer, this innovator designs and manufactures high-performance cast parts for the global mobility and aerospace sectors.

-

Key Products: Light-alloy powertrain housings, structural magnesium components, safety-critical suspension parts, and advanced industrial turbine blades.

-

Market Capitalization: Approximately CHF 3.60 Billion as of mid-2026.

Nemak

-

About: Headquartered in Mexico, Nemak is an elite global tier-1 automotive supplier specializing in aluminum components for e-mobility and conventional powertrains.

-

Key Products: Complex electric vehicle battery enclosures, multi-piece e-motor housings, and structural cylinder heads.

-

Market Capitalization: Approximately MXN 10.30 Billion as of mid-2026.

Endurance Technologies Limited

-

About: Endurance Technologies stands as one of India’s largest automotive component manufacturers, running advanced casting operations across Asia and Europe.

-

Key Products: High-pressure aluminum die-cast engine parts, complex two-wheeler transmission casings, and alloy wheels.

-

Market Capitalization: Approximately INR 36,184 Crores as of mid-2026.

What Is the Future of the Market?

The future of metal casting is tied to digital transformation and smart foundry automation. Foundries are increasingly deploying Internet of Things (IoT) sensors throughout their molding lines to track real-time thermal variations, molten fluid dynamics, and sand core consistency, preventing internal casting defects before the metal is poured.

Furthermore, the integration of 3D sand printing allows foundries to eliminate traditional wooden tooling entirely. This technology enables rapid prototyping of massive, complex components in days rather than months, reshaping production timelines for low-volume aerospace and heavy defense applications.

Insights: Strategic Guidance for Market Players

To capture value in this evolving industrial sector, market participants should execute three critical strategies:

1. Invest in Large-Scale Die-Casting Assets: Upgrading foundries with multi-thousand-ton gigacasting machinery positions businesses as indispensable structural suppliers to leading EV and hybrid vehicle manufacturers.

2. Transition to Advanced Induction Heating: Moving away from coke- and gas-fired cupola furnaces toward electric induction options shields operations from shifting fuel prices while lowering corporate emissions.

3. Expand Downstream Value-Add Services: Providing in-house CNC finish-machining, x-ray quality testing, and surface treatments allows foundries to capture higher product margins compared to supplying raw, unfinished castings.

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Email: [email protected]

Leave a Reply