The global specialty chemicals and performance materials sector is undergoing a profound structural evolution. Driven by rapid industrialization, complex chemical processing demands, and a global pivot toward strict environmental compliance, the high-performance catalyst market has emerged as an essential pillar of modern manufacturing. High-performance catalysts—ranging from engineered solid-state structures to precise biological enzymes—are fundamental to reducing process energy requirements, minimizing harmful emissions, and maximizing product selectivity. This comprehensive report outlines the core market dynamics, segmentation insights, and strategic corporate initiatives shaping the global landscape.

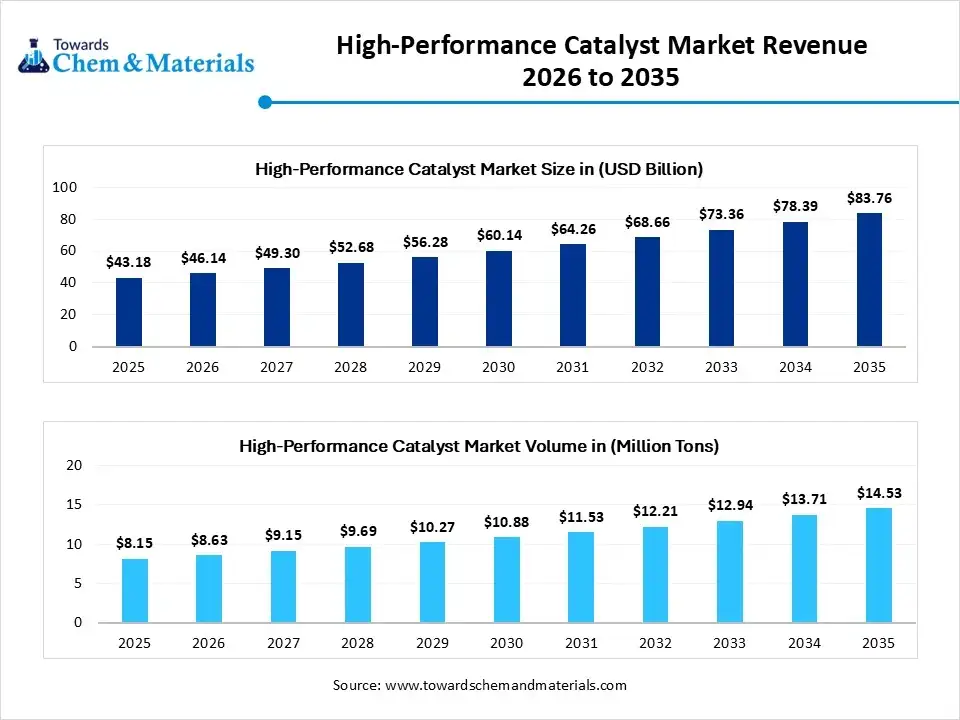

The global high-performance catalyst market is experiencing consistent long-term growth, supported by steady demand from the refining, petrochemical, and automotive sectors, along with emerging clean energy infrastructures. Valued at USD 43.18 billion in 2025, the market is estimated to reach USD 46.14 billion in 2026. Strategic long-term modeling projects that the market will achieve a value of USD 83.76 billion by 2035, expanding at a compound annual growth rate (CAGR) of 6.85% over the forecast period from 2026 to 2035.

In terms of physical volume, the industry is projected to scale from 8.15 million tons in 2025 to 14.53 million tons by 2035, exhibiting a volume CAGR of 5.95%. This strong volume and revenue trajectory reflects an increasing industrial reliance on advanced active components capable of driving down carbon emissions and optimizing feedstock yields.

Market Overview: What is the High-Performance Catalyst Market?

The high-performance catalyst market encompasses the research, chemical synthesis, and industrial application of advanced compounds engineered to accelerate chemical reactions without being consumed in the process. These specialized catalysts modify molecular activation energy, allowing industrial facilities to operate at lower temperatures and pressures.

By improving reaction selectivity, high-performance catalysts significantly minimize byproducts and unwanted waste, helping manufacturers optimize their production lines. Today, these advanced materials are heavily utilized across oil refining, environmental emission management, pharmaceutical processing, and the expanding green hydrogen infrastructure.

Market Dynamics: What Are the Key Factors Driving the Market?

What Are the Primary Drivers for This Market?

-

Stricter Environmental Compliance Pressure: Governments worldwide are enforcing legally binding caps on industrial emissions and automotive exhaust gases, compelling plants to implement advanced catalytic abatement systems.

-

Petrochemical and Refining Growth: The steady global demand for cleaner, lower-sulfur fuels requires advanced catalytic cracking, reforming, and hydroprocessing solutions capable of managing complex, variable feedstocks.

-

Fine Chemical and Pharmaceutical Selectivity: The expanding life sciences sector demands high-purity molecular structures, accelerating the use of highly selective catalysts that eliminate multi-step processing waste.

Why Is This Market Important?

High-performance catalysts are vital for balancing ongoing industrial growth with international carbon-neutral targets. Without these advanced materials, primary industries would face higher thermal energy expenses, elevated greenhouse gas profiles, and increased raw material costs. They enable the integration of renewable bio-feedstocks—such as used cooking oils—into traditional refining infrastructure by efficiently removing impurities, smoothing the transition away from fossil-dependent manufacturing.

What Are the Benefits of Using High-Performance Catalysts?

Modern industrial chemical operations achieve substantial performance and environmental advantages by deploying advanced catalysts:

-

Optimized Resource and Energy Efficiency: Enables large-scale reactions to proceed under milder operational settings, which curbed utility consumption and thermal degradation.

-

Maximized Product Selectivity: Lowers waste generation by steering chemical pathways toward the desired target molecules, which is critical for fine chemicals and pharmaceuticals.

-

Excellent Reusability and Durability: Solid-state heterogeneous variants provide ease of separation and long active lifetimes, supporting continuous production and lowering replacement costs.

-

Superior Environmental Control: Speeds up the conversion of toxic exhaust byproducts (such as nitrous oxides and carbon monoxide) into harmless atmospheric gases inside automotive and industrial scrubbing systems.

Global High-Performance Catalyst Market Segmentation

The market is analyzed across type, active component, application, end-user industry, and geographic region.

By Market Type

-

Heterogeneous Catalysts: Dominated the global landscape with a 61% market share in 2025. Their solid-state nature makes them ideal for continuous, high-volume production lines in petrochemical plants, where ease of separation and reusability are crucial.

-

Homogeneous Catalysts: Anticipated to experience significant growth due to their high selectivity and molecule-specific reaction control within specialized fine chemical synthesis.

-

Biocatalysts: Gaining traction for organic, low-temperature enzymatic transformations in food processing and pharmaceutical manufacturing.

By Active Component

-

Noble Metals: Commanded a 44% market share in 2025. Materials like platinum, palladium, and rhodium remain vital for demanding automotive catalytic converters and specialized chemical refining.

-

Transition Metals & Metal Oxides: Extensively utilized for large-scale industrial oxidation, synthesis gas production, and base chemical processing.

By Application & End-User

-

Petrochemical Application: Led the sector with a 46% market share in 2025, driven by continuous catalytic cracking and hydroprocessing operations.

-

Automotive End-User: Held a 28% market share in 2025, supported by the manufacturing of catalytic converters to comply with tightening global vehicular emission limits.

Key Regional Trends: Where is Growth Concentrated?

Asia Pacific: The Industrial Powerhouse

Asia Pacific led the global arena with a 43% revenue share in 2025 and is projected to expand at the fastest regional CAGR of 6.97%. This regional focus is driven by a vast industrial manufacturing base, heavy investments in domestic petrochemical processing facilities across China and India, and tightening domestic air quality mandates. Favorable government support for industrial modernization also continues to accelerate regional catalyst consumption.

North America & Europe: Centers for Green Innovation

North America maintains a dominant position backed by specialized industrial operations, research infrastructure, and extensive investments in upgrading domestic refining and environmental setups. Meanwhile, Europe is emerging as a fast-growing hub for advanced precious metal catalysts, driven by a well-established chemical sector and an industry-wide focus on green hydrogen technologies and low-carbon industrial processes.

What Are the Key Challenges Facing the Market?

Despite strong market drivers, the industry faces notable hurdles:

-

High Production Costs: The heavy reliance on rare, expensive noble metals (such as platinum and palladium) significantly impacts production costs and working capital.

-

Supply Chain and Geopolitical Volatility: Sourcing base metals and precious minerals exposes manufacturers to trade restrictions and localized supply disruptions.

-

Complex R&D Cycles: Developing advanced catalysts with high thermal stability and resistance to chemical “poisoning” requires extensive research funding and long development timelines.

Market Recent Government Initiatives: What is Shaping the Industry?

National regulatory updates are actively driving the shift toward high-performance catalytic systems:

-

India’s Industrial Emission Targets: The Government of India strengthened its Greenhouse Gas Emission Intensity (GEI) Reduction Rules and rolled out its Carbon Credit Trading Scheme (CCTS) to curb manufacturing footprints. Simultaneously, the Department of Science and Technology is funding advanced nano-catalyst research to support domestic green hydrogen production.

-

Global Automotive Air Quality Mandates: Increasingly strict vehicular emission rules across the US, the European Union, and East Asia require automakers to install highly efficient, multi-component catalytic converters.

-

Decarbonization Subsidies: Several Western nations provide financial incentives and subsidies for low-carbon industrial work and hydrogen-based energy networks, boosting the demand for specialized clean energy catalysts.

Competitive Landscape: Top Companies and Strategic Portfolio Focus

BASF SE

-

About: A major global chemical enterprise with a dedicated Catalysts division focused on automotive emission control, battery materials, and industrial chemical processing.

-

Products: Advanced heterogeneous chemical catalysts, environmental catalysts for stationary sources, and custom refining formulas.

-

Market Cap: Approximately EUR 42.60 Billion (as of mid-2026).

Johnson Matthey

-

About: A specialized global sustainable technologies corporation with extensive expertise in platinum group metals (PGMs) and advanced catalytic synthesis.

-

Products: High-purity blue and green hydrogen generation catalysts, automotive catalytic components, and chemical transformation technologies.

-

Market Cap: Approximately GBP 3.79 Billion (as of mid-2026).

Honeywell UOP

-

About: A prominent technology supplier and software developer serving the global petroleum refining, gas processing, and petrochemical manufacturing sectors.

-

Products: High-performance catalysts for fluid catalytic cracking (FCC), reforming, isomerization, and hydroprocessing operations.

-

Market Cap: Parent enterprise (Honeywell International Inc.) is valued at approximately USD 132 Billion.

Topsoe A/S (Haldor Topsoe)

-

About: A specialized chemical technology company focused on carbon reduction solutions, energy efficiency, and solid-surface catalyst systems.

-

Products: SynCOR™ autothermal reforming technologies, hydroprocessing catalysts, and emissions management systems.

-

Market Cap: Privately held company.

Recent Developments by Major Companies: Innovation in Action

Corporate investments are increasingly aligning with the transition toward alternative energy and higher-purity chemical processes:

-

Strategic Green Technology Portfolio Shifts: In mid-2026, Johnson Matthey advanced its strategic plan to focus on lean, cash-generative segments, moving forward with its £1.325 billion sale of its Catalyst Technologies unit to prioritize stationary emission systems and data center cooling technologies via its Cormetech acquisition.

-

Launch of Specialized Hydrogen Dryers: In November 2025, GSA introduced an innovative industrial hydrogen dryer built on a specialized palladium catalyst platform. This system delivers ultra-high-purity hydrogen while lowering energy demand and reducing overall environmental impact.

-

Nano-Catalysis and Clean Fuel Upgrades: Leading catalyst producers are expanding their R&D into specialized nano-catalysts designed to efficiently remove impurities from renewable bio-based inputs, such as used cooking oils, ensuring clean fuel conversion.

What is the Future of the Market?

The global high-performance catalyst market is positioned for significant growth, driven by the expanding hydrogen economy and a broader shift toward circular industrial practices. As manufacturing plants move away from traditional fossil dependencies, the demand for advanced electro-catalysts and nano-catalytic systems for green hydrogen production is expected to scale rapidly.

Future market expansion will likely be guided by advancements in non-precious metal catalyst alternatives, smart process controls, and materials that can extend operational lifetimes. Chemical and material science companies that invest in secure raw material supply chains, automated production lines, and clean energy applications are well-positioned to lead the next generation of industrial processing.

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Email: [email protected]

Leave a Reply