Executive Summary

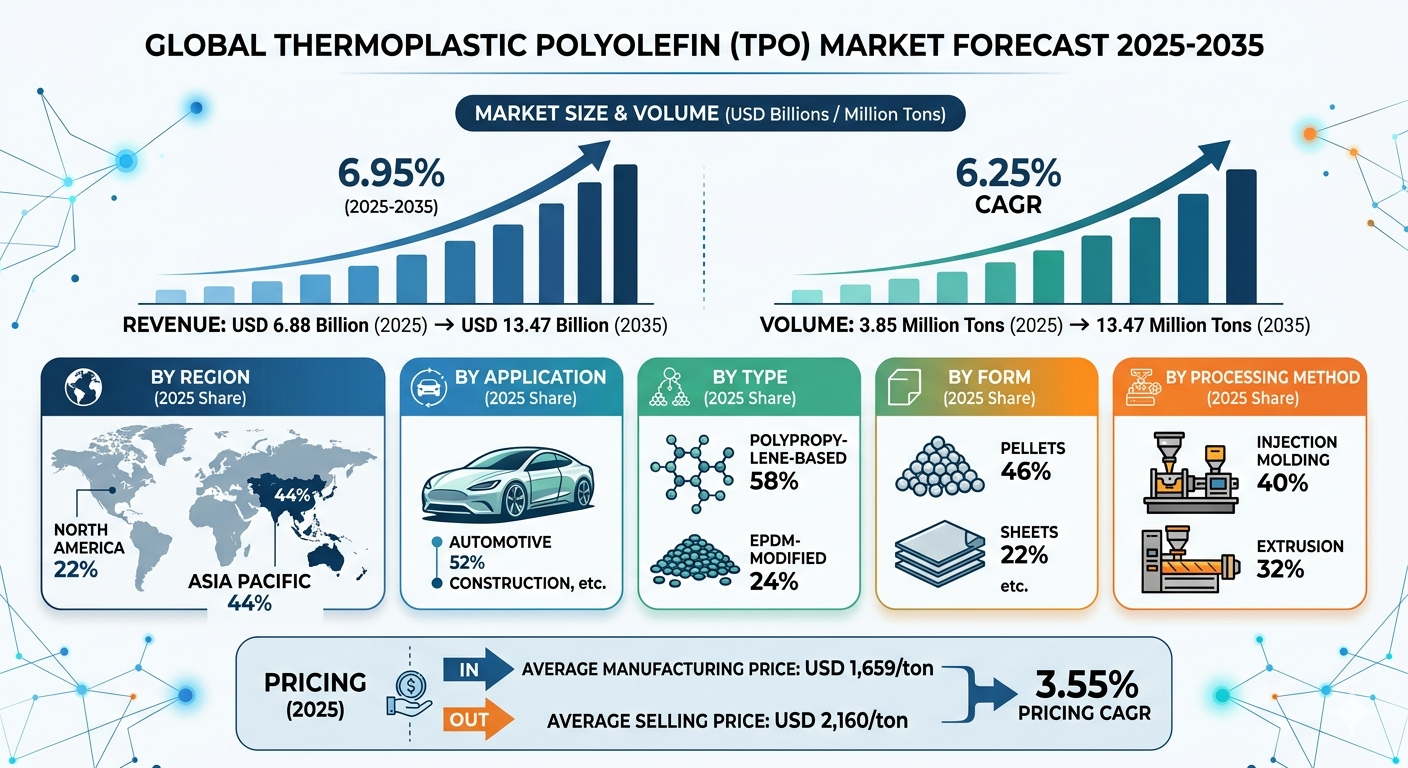

The global Thermoplastic Polyolefin (TPO) market is undergoing a major structural evolution driven by industrial lightweighting, aggressive automotive engineering redesigns, and a shifting regulatory focus toward low-carbon footprint manufacturing. As of 2025, the global TPO market valuation stood at USD 6.88 Billion, supported by a robust baseline manufacturing volume of 3.85 Million Tons. Capitalizing on high performance-to-weight ratios and efficient processing cycles, the market is poised to compound at a revenue CAGR of 6.95% from 2025 through 2035.

By continuing along this trajectory, market revenues are projected to reach USD 13.47 Billion by 2035. Over the same forecast horizon, volumetric consumption is expected to expand at a CAGR of 6.25%, reaching a targeted scale of 13.47 Million Tons by 2035. To align with specific client parameters seeking mid-term tracking milestones, this compounding growth positions the global market value to reach approximately USD 10.92 Billion by 2032.

Market Overview & Dynamics

What is the Thermoplastic Polyolefin Market?

Thermoplastic Polyolefin (TPO) refers to a versatile class of polymer blends combining a polypropylene (PP) matrix with elastomeric additives, most notably Ethylene Propylene Diene Monomer (EPDM) or ethylene-octene copolymers. This structural hybridization yields a compound that delivers the structural rigidity and thermal resistance of engineering plastics alongside the flexible, high-impact capabilities of conventional rubber. Unlike traditional thermoset rubber variants, TPO materials are fully recyclable and can be re-melted and reshaped multiple times, placing them at the center of modern circular economy initiatives within heavy manufacturing sectors.

Why Is This Market Historically and Logistically Important?

The intrinsic value of TPO materials lies in their disruptive capability to replace heavier, costlier, and less sustainable engineering materials like Polyvinyl Chloride (PVC), polyurethane, and certain metals. Historically, industries were forced to trade mechanical strength for design elasticity. TPO eliminated this compromise, offering an optimized substrate that demonstrates outstanding chemical stability, exceptional UV resistance, and excellent low-temperature impact strength. Logistically, TPO plays a foundational role in reducing vehicular emissions through lightweighting and reducing building energy costs when utilized as reflective, high-albedo commercial roofing membranes.

What Are the Key Factors Driving The Market?

-

The Global Automotive Lightweighting Imperative: Driven by strict corporate average fuel economy guidelines and the continuing expansion of the electric vehicle (EV) ecosystem, automotive OEMs are systematically replacing sheet metals and heavy polymers with high-performance TPO. Lowering structural weight directly correlates with extended battery ranges in EVs and lowered tailpipe emissions in internal combustion engines.

-

Decarbonization of Commercial Construction: Modern building infrastructure increasingly demands energy-efficient, cool-roofing solutions. TPO sheets offer a highly reflective surface that significantly cuts HVAC cooling loads, directly aligning with global net-zero building mandates.

-

Manufacturing Energy Efficiency: TPO processing demands lower melt temperatures and faster cycle times than competitive engineering resins. This translates into measurable energy savings and reduced operating overhead for plastics compounders and injection molders.

Technical Insights & Practical Benefits

What Are the Core Benefits of Using TPO Materials?

TPO compounds offer a compelling suite of performance advantages that make them a preferred material for complex engineering requirements:

-

Optimized Flexural and Tensile Balance: Blending polypropylene with elastomers ensures the final component does not fail under high mechanical stress or brittle low-temperature conditions.

-

Inherent Weatherability and UV Stability: TPO resists environmental oxidation, cracking, and ozone degradation, rendering it highly durable for external automotive panels and exposed civil infrastructure.

-

Superior Processing Efficiency: TPO is highly compatible with high-speed automated production frameworks, exhibiting uniform melt flow behavior and minimal shrinkage variance.

Data Reference Point Note: The financial dynamics of TPO manufacturing highlight robust margin health across processing tiers. In 2025, the global Average Manufacturing Price was benchmarked at USD 1,659/ton, compared to an Average Selling Price (ASP) of USD 2,160/ton. The price evolution is anticipated to rise continuously at a Pricing CAGR of 3.55% through 2035, driven by functional compounding modifications and specialized additive integrations

Market Segments & Performance Granularity

Which Segment Accounted for the Largest Market Share?

An analytical breakdown of the TPO landscape across core segments displays a well-defined concentration of volume and market power:

-

By Region: The Asia Pacific region dominated global operations with a commanding 44% market share in 2025. Backed by rapid industrialization, extensive automotive manufacturing hubs, and large infrastructure projects in China and India, APAC is slated to maintain its position as the fastest-growing region, clocking a CAGR of 7.5%. Concurrently, North America remains a mature powerhouse, holding a notable 22% market share in 2025, anchored heavily by the region’s commercial roofing retrofit sector.

-

By Type: The polypropylene-based TPO segment captured the largest market share with 58% in 2025, favored for its baseline cost-effectiveness and broad utility. However, the EPDM-modified TPO segment—holding a 24% market share in 2025—is anticipated to be the fastest-growing type, recording a CAGR of 7.5% due to its superior elastomeric rebound and thermal sealing properties.

-

By Form: The standard pellets segment captured the top spot with a 46% share in 2025 due to its ease of transport and storage for injection molding feeds. The sheets segment, holding a 22% share in 2025, is the fastest-expanding structural form with a projected CAGR of 7.2%, moving in lockstep with single-ply membrane roofing demand.

-

By Application: The automotive sector dominated all end-uses with a 52% market share in 2025. It is projected to lead future growth with a 7.1% CAGR, propelled by interior trim, instrument panels, and bumper fascia applications.

-

By Processing Method: Injection molding led processing with a 40% market share in 2025. Meanwhile, extrusion methods represented 32% of the market in 2025, and will outpace other methods with a 6.9% CAGR due to continuous sheet and profile production efficiencies

Key Strategic Trends & Regulatory Environment

What Are the Primary Key Market Trends?

The global TPO ecosystem is navigating a paradigm shift toward early-stage product integration. Historically, manufacturers treated TPO as an afterthought or a secondary alternative to replace underperforming polymers. Today, engineering teams introduce TPO at the foundational design and conceptual phase of a product cycle, unlocking maximum aerodynamic and structural advantages. Additionally, there is an industry-wide trend toward high-flow TPO formulations that accommodate thin-wall designs. This allows part walls to be molded with significantly less thickness without compromising the structural safety or integrity of the final product.

What Are the Recent Government Initiatives Impacting the Market?

Global regulatory mandates are serving as structural drivers for TPO market acceleration. In the European Union, the Ecodesign for Sustainable Products Regulation (ESPR) enforces strict end-of-life vehicle recyclability targets, penalizing non-recyclable thermoset composites and favoring recyclable thermoplastic matrices like TPO. In the United States, federal energy efficiency incentives provided under the Inflation Reduction Act (IRA) heavily subsidize commercial retrofits that employ energy-efficient, cool-roofing TPO membranes. Furthermore, nationwide net-zero building updates across major Asian nations—such as India and Japan—have institutionalized reflective roof mandates, forcing a programmatic pivot toward white TPO sheeting.

Competitive Landscape & Top Companies

The global TPO space features a consolidated core tier of chemical conglomerates that drive innovation through strategic capacity expansions, custom compounding breakthroughs, and targeted asset acquisitions.

Major Market Competitors

1. Dow Chemical Company (Dow Inc.)

-

About: Headquartered in Michigan, USA, Dow is an elite tier-one material science leader with broad global operations spanning packaging, infrastructure, and consumer applications.

-

Products: Marketed under the Engage™ and Infuse™ brand architectures, Dow offers high-performance polyolefin elastomers (POEs) and olefin block copolymers utilized globally to modify TPO structures.

-

Market Cap: Approximately USD 38.5 Billion.

2. Mitsui Chemicals, Inc.

-

About: Operating out of Tokyo, Japan, Mitsui Chemicals is a premium specialty chemical producer focusing heavily on functional polymeric materials for the automotive and electronic sectors.

-

Products: Mitsui manufactures Milastomer™, a premier thermoplastic olefin elastomer series widely specified for automotive weatherstrips, interior skins, and soft-touch gaskets.

-

Market Cap: Approximately USD 4.8 Billion.

3. Sumitomo Chemical Co., Ltd.

-

About: Sumitomo Chemical is a highly diversified Japanese multinational chemical corporation providing advanced polymer solutions, petrochemicals, and energy-related materials globally.

-

Products: Sumitomo supplies specialized polypropylene matrix resins and custom TPO compounds engineered for high impact resistance and optimal flow properties in injection molding fields.

-

Market Cap: Approximately USD 4.2 Billion.

Recent Industrial Developments

The industry has witnessed significant commercial expansion and product launches tailored to meet high-performance infrastructure demands. Notably, IB Roof Systems expanded its commercial portfolio by launching an advanced range of TPO membranes explicitly engineered for low-slope commercial roofing applications. These membranes are distributed across multiple specific industrial thickness levels (60 mil, 80 mil, 115 mil, and 135 mil) and optimized to operate seamlessly as integrated, single-system architectures alongside preexisting building insulation.

Concurrently, on the regional infrastructural front, market leaders like Sika AG completed key corporate acquisitions, including sustainable urban greening expert Elmich Pte Ltd, while opening dedicated chemical manufacturing facilities in Singapore and Xi’an. These targeted manufacturing investments have successfully reduced local single-ply TPO membrane shipping lead times down to a lean three-to-five-day operating window across dense Asia Pacific shipping corridors.

Future Outlook

What is the Future of the Market?

Looking out toward 2035, the global Thermoplastic Polyolefin market is poised to solidify its role as a vital material within sustainable engineering. Future expansions will depend on the successful commercial scaling of bio-based polyolefin matrices derived from renewable, non-food crop feedstocks. As manufacturing entities face mounting carbon accounting audits, the capability to supply low-carbon, drop-in bio-TPO alternatives will differentiate market leaders from standard compounders.

Furthermore, as the global deployment of automated, high-precision additive manufacturing speeds up, the market will likely see the launch of specialized, micronized TPO powders tailored specifically for industrial 3D printing and advanced rapid prototyping applications. This evolution will firmly cement TPO’s role as a cornerstone of next-generation material design.

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Email: [email protected]

Leave a Reply