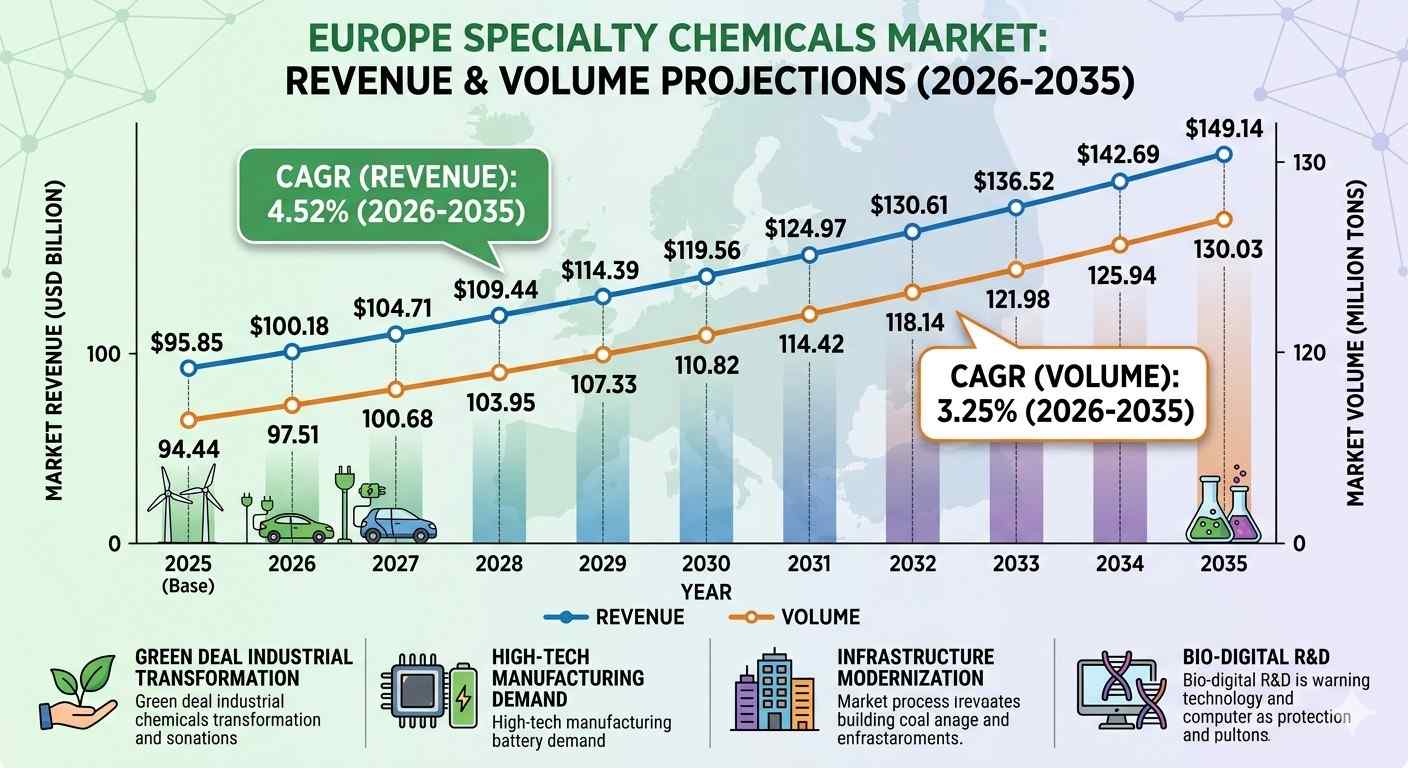

The European specialty chemicals sector is navigating a pivotal era defined by a strategic shift from volume-driven production to high-margin, performance-led innovation. Valued at USD 100.18 billion in 2026, the market is projected to reach USD 149.14 billion by 2035, expanding at a CAGR of 4.52%.

Parallel to this value growth, market volume is expected to rise from 94.44 million tons in 2025 to 130.03 million tons by 2035, representing a CAGR of 3.25%. This delta between value and volume growth underscores a significant trend: the “premiumization” of the European chemical portfolio, where advanced functionalities and sustainability credentials command higher market prices.

What are the Primary Drivers for the Europe Specialty Chemicals Market?

The trajectory of the European market is uniquely tethered to the “Green Deal” industrial transformation. Unlike other regions, Europe’s growth is not merely a byproduct of industrial demand but is actively shaped by stringent environmental mandates.

-

Sustainability as a Service: The EU Chemical Strategy for Sustainability is forcing a massive overhaul of formulations. Companies are replacing conventional surfactants and stabilizers with bio-based, non-toxic alternatives, creating a high-growth niche for “green” specialty chemicals.

-

High-Tech Manufacturing Demand: The resurgence of domestic semiconductor manufacturing and the acceleration of the EV battery supply chain are driving demand for ultra-high-purity electronic chemicals and advanced polymers.

-

Infrastructure Modernization: Urbanization and the push for energy-efficient “Green Buildings” have spiked demand for high-performance insulation materials, specialized coatings, and concrete admixtures.

Key Segments & Emerging Technological Shifts

The market is fragmenting into highly specialized application clusters, with digital and biological intersections defining the next generation of products.

Dominant and Emerging Segments

Agrochemicals continue to hold the largest market share by product type, driven by the need for precision farming solutions and eco-friendly pesticides that comply with the EU’s “Farm to Fork” strategy. Conversely, Personal Care Ingredients and Personalized Medicines represent the fastest-growing segments, as consumer spending shifts toward customized, sustainable, and dermatologically advanced formulations.

Technological Evolution: AI and Circularity

Technological shifts are moving toward Digital R&D and Molecular Modeling. AI-driven platforms are now significantly reducing the “time-to-market” for new molecules by predicting material properties before physical synthesis. Furthermore, Chemical Recycling (Pyrolysis) is integrating into the specialty chain, allowing manufacturers to offer “circular” specialty polymers that meet the recycled-content requirements of the automotive and packaging industries.

Competitive Landscape: Strategic Moves of Key Players

The European competitive environment is undergoing a “portfolio purification” phase. Legacy giants are divesting commodity-linked assets to focus exclusively on high-value specialties.

-

BASF and Evonik: These leaders are aggressively investing in Carbon Management and bio-based platforms. Evonik, for instance, has pivoted heavily toward lipid technology for mRNA vaccines and biosurfactants for household care.

-

Solvay and Clariant: Both have undergone structural reorganizations to sharpen their focus on “essential” chemicals and high-performance solutions for electronics and renewable energy.

-

Specialized Entrants: Middle-market players are gaining ground by offering “Bespoke Chemical Services,” catering to the specific needs of regional SMEs that require smaller, tailored batches of high-performance additives rather than bulk shipments.

Data Presentation & Recent Developments

The following table highlights the critical divergence between value and volume, indicating the rising cost and value-add of modern specialty chemicals.

Europe Specialty Chemicals Market Projection (2025–2035)

| Year | Market Value (USD Billion) | Market Volume (Million Tons) |

| 2025 (Base) | 95.85 | 94.44 |

| 2026 (Est.) | 100.18 | 97.51 |

| 2035 (Proj.) | 149.14 | 130.03 |

| CAGR | 4.52% | 3.25% |

Recent Industry Milestones:

-

2025: The first commercial-scale biosurfactant plants became operational in Germany, utilizing fermentation instead of petroleum-based synthesis.

-

2026: Widespread adoption of “Digital Product Passports” across the EU, requiring specialty chemical producers to provide granular data on carbon footprint and toxicity for every batch.

-

Q1 2026: Multiple strategic mergers in the Electronic Chemicals sub-sector to support the growing European “Silicon Shield” initiative.

Recent Government Initiatives Shaping the Market

Regulatory pressure in Europe has transitioned from a hurdle to a market-maker. The REACH 2.0 revisions and the Eco-design for Sustainable Products Regulation (ESPR) are the most influential frameworks. Governments are providing massive subsidies through the Innovation Fund for projects that demonstrate “Functional Substitution”—replacing hazardous substances with safer, high-performing specialty chemicals. Additionally, national “Hydrogen Strategies” in France and Germany are creating a new demand vertical for specialty catalysts and ion-exchange membranes.

Conclusion: The Forward-Looking Perspective

The next decade will define Europe not as a high-volume producer, but as the world’s “Sustainability Laboratory.” We expect the market to become increasingly bifurcated: companies that cannot adapt to the circular economy will face obsolescence, while those mastering the “Bio-Digital” intersection will thrive. As the industry approaches 2035, the “Specialty” in specialty chemicals will no longer refer just to the application, but to the verifiable environmental and social impact of the molecule itself.

Leave a Reply