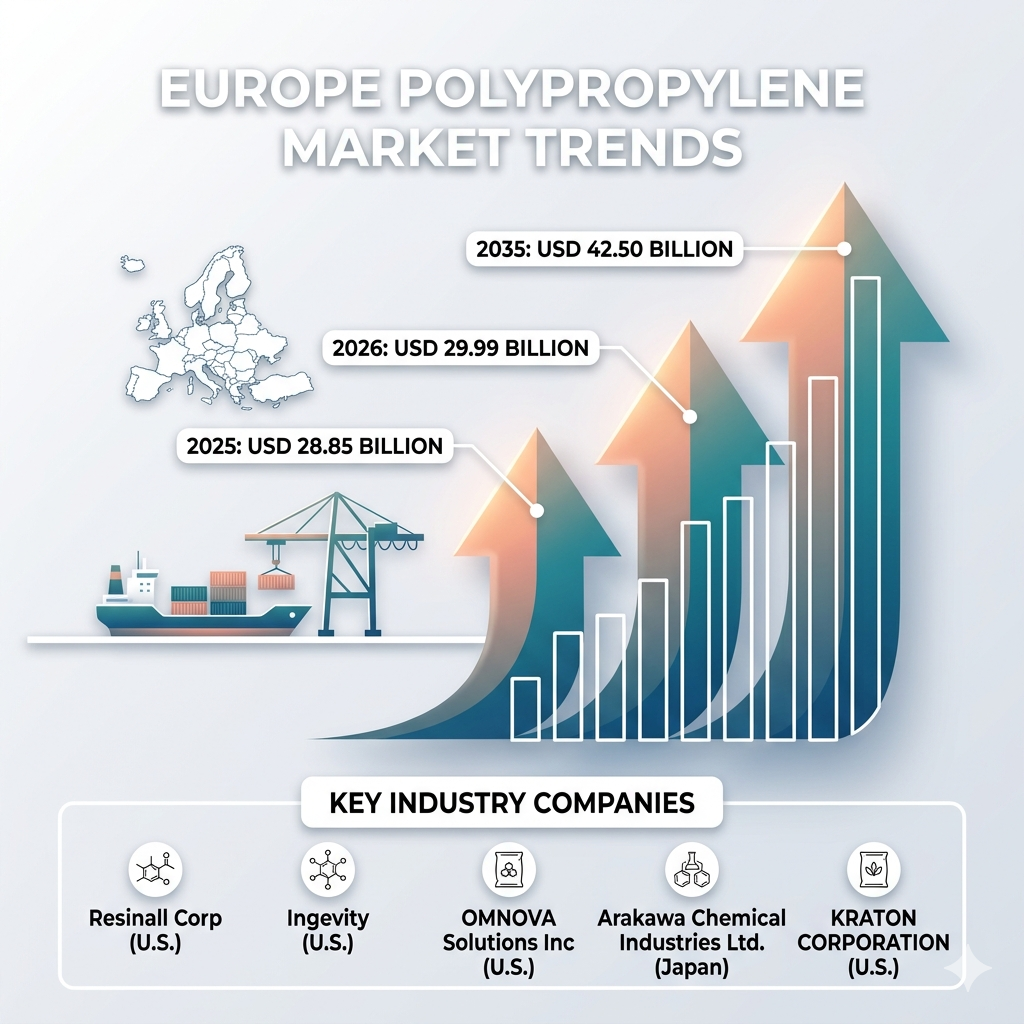

The Europe polypropylene market is undergoing a major structural transformation driven by strict circular economy mandates, localized automotive supply chains, and advanced food contact safety packaging regulations. Valued at USD 28.85 billion in 2025, the market is estimated to reach USD 29.99 billion in 2026. Projecting forward, the market is on track to reach USD 42.50 billion by 2035, growing at a compound annual growth rate (CAGR) of 3.95% over the forecast period from 2026 to 2035. In terms of volume, the market is expected to expand from 16.19 million tons in 2025 to 22.51 million tons by 2035, expanding at a volume-based CAGR of 3.35%. This high-value trajectory reflects the transition of European plastic compounding toward mechanically and chemically recycled polymer alternatives.

Market Overview

What is the Europe Polypropylene Market?

The European polypropylene market encompasses the production, distribution, and consumption of thermoplastic addition polymers made from the combination of propylene monomers. Known for its ruggedness, chemical resistance, and high melting point, polypropylene is highly valued across critical manufacturing sectors. In Europe, this market operates under intense regulatory oversight, driving producers to innovate in homopolymers, random copolymers, and block copolymers. These materials are heavily utilized across Western and Central Europe in fast-moving consumer goods (FMCG) packaging, medical devices, and light-weighted automotive parts.

Why Is This Market Important?

Polypropylene is an essential baseline material for European industrial manufacturing. Its exceptional thermal stability and fatigue resistance make it indispensable for reducing vehicle weight to meet strict carbon emission goals, while its moisture barrier properties protect food supplies. Furthermore, as Europe pivots toward localized production, polypropylene serves as a key economic indicator for regional manufacturing health. It bridges the gap between commodity plastics and high-performance engineering resins without escalating baseline production costs.

Market Dynamics

What Are the Key Factors Driving the Market?

The growth of the European polypropylene market is fueled by the continuous lightweighting of internal combustion engines and electric vehicles to lower vehicle emissions. Automakers are replacing heavy metal brackets, interior trims, and dashboard assemblies with high-performance polypropylene compounds. Additionally, the booming e-commerce sector and medical device supply chains across Western Europe demand highly sterile, impact-resistant, and chemically inert packaging mediums.

What is Key Market Trends?

The defining trend in the current market landscape is the massive shift from virgin, fossil-fuel-derived resins to post-consumer recycled (PCR) and bio-allocated polypropylene fractions. This is achieved through mass-balance certification pathways. Chemical recycling technologies, such as pyrolysis and gasification, are rapidly gaining traction alongside advanced mechanical sorting plants. This allows manufacturers to produce high-purity recycled polypropylene that satisfies the European Union’s stringent requirements for food-contact materials.

Technical Insights and Core Benefits

What is Market Benefits of Using Polypropylene?

Polypropylene delivers a uniquely balanced property profile, blending low density with high heat distortion thresholds, excellent stress-crack resistance, and complete chemical neutrality against acids and organic solvents. From a manufacturing perspective, its high flow rate simplifies the injection molding of complex shapes, cutting energy consumption and cycle times compared to alternative polymers. Additionally, its inherent cleanliness makes it ideal for medical syringes, labware, and flexible food pouches that require hot-filling or steam sterilization.

Market Segmentation and Forecast Indicators

The market can be segmented by type (homopolymer, copolymer), application (packaging, automotive, building & construction, medical), and geography (Western Europe, Central & Eastern Europe). Below is the recommended structured layout for tracking data points through the 2035 horizon.

| Year | Market Value (USD Billion) | Market Volume (Million Tons) | Key Growth Drivers |

| 2025 | 28.85 | 16.19 | Automotive lightweighting & rigid packaging baseline |

| 2026 | 29.99 | 16.73 | Rigid compliance with circular economy frameworks |

| 2035 (Projected) | 42.50 | 22.51 | Broad adoption of chemically recycled & bio-based resins |

Which Segment Accounted for the Largest Market Share?

The packaging segment continues to hold the dominant share of both market volume and value across Europe. This dominance is led by thin-wall injection-molded containers, clear caps and closures, and biaxially oriented polypropylene (BOPP) films used in flexible packaging laminate structures. While automotive applications are expanding faster on a per-unit basis, the steady, non-cyclical demand from food, beverage, and consumer goods packaging secures its position as the primary volume driver.

Regulatory and Compliance Landscape

What is Market Recent Government Initiatives?

The European chemical ecosystem is guided by the EU’s Packaging and Packaging Waste Regulation (PPWR) and the strict Circular Economy Action Plan. Recent government updates mandate minimum percentages of recycled content in all newly manufactured plastic packaging, coupled with escalating financial penalties for non-recyclable plastic waste. These regulations have forced regional resin producers to re-engineer their production setups, prompting heavy investments in sorting infrastructures and supply networks for certified circular polymers.

Competitive Landscape & Top Companies

The European landscape is highly consolidated, with a few chemical conglomerates managing large integrated crackers and derivative production lines.

LyondellBasell Industries N.V.

-

About: LyondellBasell is an international plastics, chemical, and refining powerhouse, rooted in European operations with core corporate offices in the Netherlands. It stands as one of the world’s largest producers of versatile polyolefin materials.

-

Products: Offers advanced polypropylene grades under the Circulen circular polymer line, alongside Moplen homopolymers and Clyrell specialized resins.

-

Market Capitalization: Approximately USD 21.73 billion.

Borealis AG

-

About: Headquartered in Austria, Borealis is a premier provider of advanced polyolefin solutions, majority-owned by OMV. The company serves as a vital anchor for polyolefin innovation throughout Europe.

-

Products: Specializes in Borstar technology polypropylene, Borcycle mechanically recycled polypropylene compounds, and Bornewables bio-allocated resins.

-

Market Capitalization: Private entity (Majority owned by OMV Group, which holds a market capitalization of approximately EUR 19.86 billion).

TotalEnergies SE

-

About: TotalEnergies is a French multi-energy major that operates highly integrated refining and petrochemical platforms across Western Europe, emphasizing the scalable production of circular polymers.

-

Products: Produces high-purity polypropylene blocks, dedicated automotive compounds, and a growing portfolio of certified circular polymers from recycled streams.

-

Market Capitalization: Approximately USD 193.96 billion.

Repsol S.A.

-

About: Based in Spain, Repsol is an integrated energy and chemical supplier leading the energy transition in the Iberian Peninsula and broader Mediterranean chemical markets.

-

Products: Markets the Repsol Reciclex range of polypropylene compounds with recycled content, along with high-flow grade resins designed for packaging applications.

-

Market Capitalization: Approximately USD 28.64 billion.

Market Recent Developments by Major Companies

Recent corporate strategies show a clear pivot toward collaborative joint ventures and major capital investments in advanced recycling plants. LyondellBasell expanded its Circulen production assets across Europe, securing long-term supply agreements for plastic waste feedstock. Simultaneously, Borealis successfully integrated advanced sorting facilities into its supply chain, enabling commercial production of food-grade recycled polypropylene compounds. TotalEnergies and Repsol have focused on upgrading their existing refining sites to handle pyrolysis oils, allowing them to introduce chemically recycled polypropylene into standard consumer grade applications.

Future Landscape and Strategic Outlook

What is the Future of the Market?

Looking ahead, the European polypropylene market will shift from volume-driven sales toward value-added circular products. By the mid-2030s, the traditional distinction between virgin and recycled plastics will likely disappear, replaced by standardized “circular-by-design” polypropylene resins. Companies that secure reliable recycled feedstocks and perfect chemical purification techniques will capture premium margins, establishing a more resilient, low-carbon polymer ecosystem across Europe.

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Email: [email protected]

Leave a Reply