Executive Summary

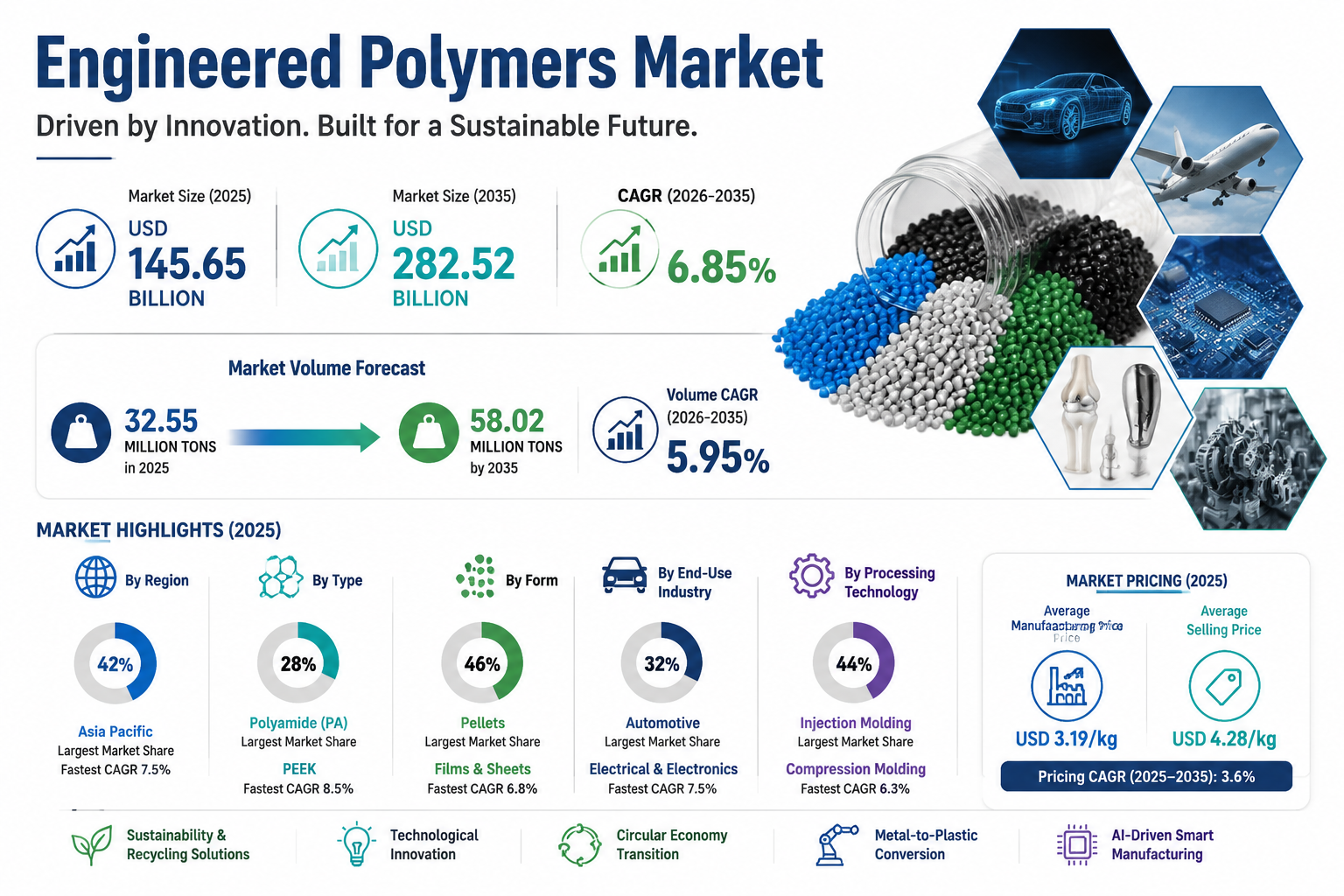

The global Engineered Polymers Market was valued at USD 145.65 billion in 2025 and is projected to reach USD 282.52 billion by 2035, growing at a CAGR of 6.85%. In terms of volume, the market will expand from 32.55 million tons in 2025 to 58.02 million tons by 2035 at a CAGR of 5.95%. Growth is fueled by technological advancements, sustainability integration, and increasing demand for metal-to-plastic conversions across automotive, electronics, and industrial sectors.

Market Overview

Engineered polymers are high-performance materials with superior dimensional stability, chemical resistance, and strength-to-weight ratios, making them essential for electrification, aerospace, and 5G applications. Rising focus on bio-based and recyclable polymers, regulatory compliance, and industrial automation is reshaping the market landscape, driving manufacturers toward precision-engineered solutions and circular economy practices.

What is Market Growth?

The market is expanding steadily due to:

- Asia Pacific dominance with 42% share in 2025 and a CAGR of 7.5%.

- North America holding 21% market share and 6.2% CAGR.

- Type-wise growth led by polyamide (28% share) and PEEK (fastest CAGR 8.5%).

- Form-wise growth led by pellets (46% share) and films & sheets (fastest CAGR 6.8%).

- End-use expansion in automotive (32% share) and electrical & electronics (fastest CAGR 7.5%).

What are Key Market Trends?

- Sustainability Integration: Adoption of bio-based and recycled polymers is rising to meet decarbonization targets.

- Metal-to-Plastic Conversion: High-performance polymers replace metals to reduce weight and operational costs.

- Advanced Manufacturing: AI-driven predictive analytics and machine learning are optimizing R&D and precision compounding.

- High-performance Applications: PEEK, PC, and polyamide are increasingly used in aerospace, medical, and EV infrastructure.

Market Recent Government Initiatives

- European Union: REACH revision, PPWR, RoHS targeting polymer safety and microplastic restrictions.

- North America: EPA and TSCA regulations focus on workers’ safety, PFAS control, and bio-based polymer adoption.

- Asia Pacific: BIS certification and Plastic Waste Management Rules enforce quality control, EV battery safety, and circular economy practices.

- Global: Annex XVII restricts microplastics in polymer powders and granules used industrially.

Market Benefits of Using Engineered Polymers

- High strength-to-weight ratio enabling automotive lightweighting.

- Superior chemical, thermal, and oxidative resistance for industrial durability.

- Dimensional stability for precision electronics and aerospace applications.

- Compatibility with recycled content and bio-based feedstock for sustainable production.

- Process flexibility across injection molding, extrusion, and blow molding for complex component manufacturing.

What Are the Key Factors Driving the Market?

- Industrial electrification and vehicle lightweighting.

- Rising adoption of high-performance thermoplastics in aerospace and electronics.

- Focus on circular economy and sustainable manufacturing.

- Technological innovations including AI-driven compounding and predictive material design.

- Strategic partnerships and government funding for advanced polymer research.

What is the Future of the Market?

The market is expected to evolve toward bio-based, recyclable, and ultra-performance polymers integrated with AI-driven manufacturing. Future demand will be driven by EVs, smart infrastructure, 5G devices, aerospace lightweighting, and sustainable industrial applications. Market consolidation and strategic partnerships will further enhance product innovation and global reach.

Why Is It Market Important?

Engineered polymers are critical for replacing metals, reducing environmental impact, enabling advanced manufacturing, and meeting stringent decarbonization and safety standards. They support high-performance, lightweight, and sustainable solutions across automotive, electronics, industrial, medical, and aerospace industries.

Which Segment Accounted for the Largest Market Share?

- By Type: Polyamide (28%) dominates, followed by Polycarbonate (16%).

- By Form: Pellets (46%) dominate; films & sheets fastest-growing (6.8% CAGR).

- By End-use: Automotive (32%) leads, electrical & electronics fastest-growing (7.5% CAGR).

- By Processing Technology: Injection molding (44%) dominates; compression molding fastest-growing (6.3% CAGR).

- By Region: Asia Pacific leads with 42%, followed by North America (21%).

Market Recent Developments by Major Companies

- Dow & RDM Group (2026): Launched Multiboard CirculaRR, a recycled fiber-based food packaging solution for circularity.

- Michelin (2026): Inaugurated PolMixLab for high-performance sustainable polymers and rubber R&D.

- Mitsui Chemicals & Polyplastics (2025): Strategic collaboration to enhance ARLEN® and AURUM® engineering plastics customer network.

- Top Players: Grand Pacific Petrochemical, BASF SE, SABIC, DuPont, LG Chem, Toray, Covestro AG, Evonik Industries AG, Eastman Chemical, Celanese Corporation.

Suggested Data Tables:

- Segment-wise market share (Type, Form, End-use, Processing Technology).

- Regional revenue and CAGR 2026–2035.

- Company profiles with market cap, product portfolio, and recent developments.

Top Companies Overview:

- Grand Pacific Petrochemical Corporation: Specialty polymers and thermoplastics; market focus on automotive and electronics.

- BASF SE: Global chemicals leader; products include PA, POM, PC; market cap ~USD 85B.

- SABIC: Engineering thermoplastics, PEEK, ABS; strong presence in Asia Pacific.

- DuPont: Advanced polymers, bio-based solutions; market cap ~USD 55B.

- LG Chem: Polycarbonate, engineering plastics; key EV battery and electronics applications.

- Toray: Carbon fiber and high-performance polymers; market cap ~USD 25B.

- Covestro AG: PC and engineering plastics; sustainability-focused R&D.

- Evonik Industries AG: Specialty additives, high-performance polymers; market cap ~USD 18B.

- Eastman Chemical Company: POM, polyester, high-performance resins; market cap ~USD 13B.

- Celanese Corporation: Polyamides, PEEK, PBT; solutions for automotive and electronics.

Leave a Reply