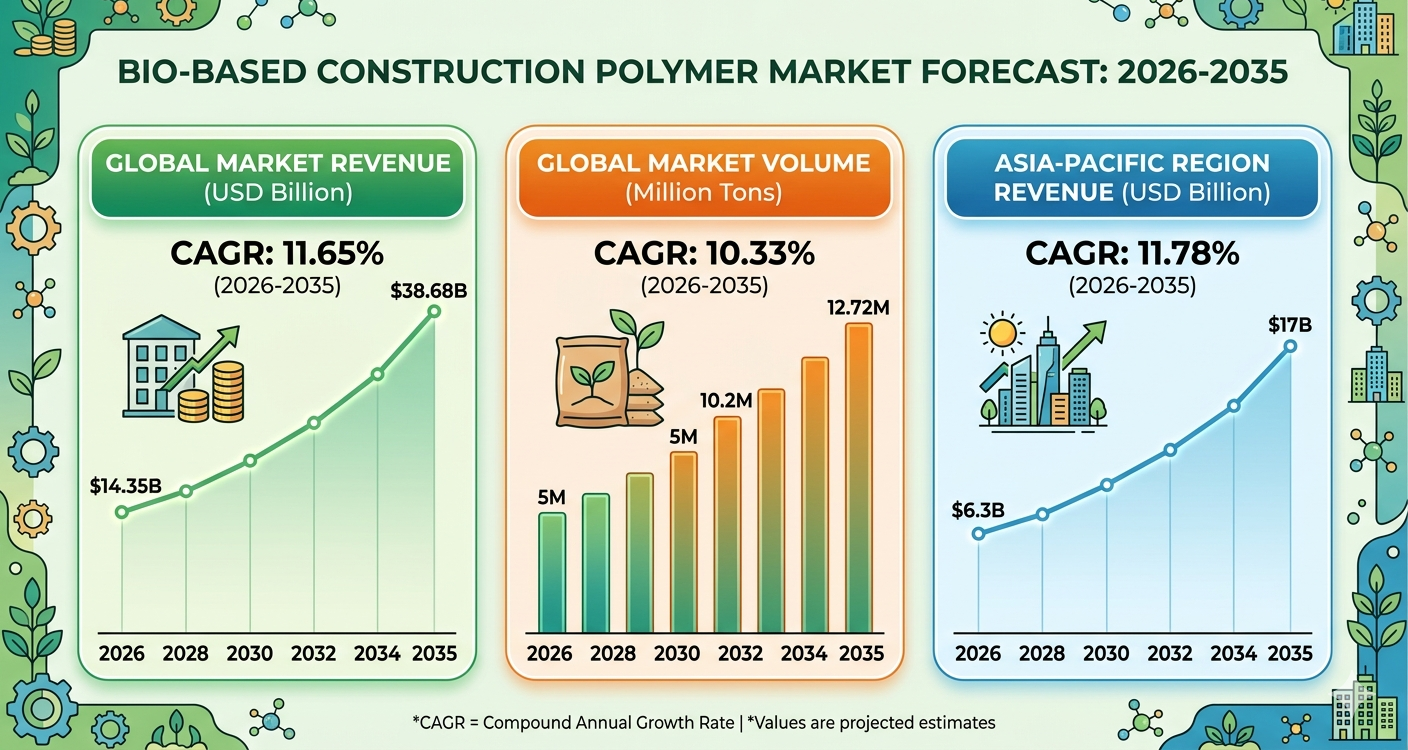

The global Bio-Based Construction Polymer Market is undergoing a profound structural shift as the AEC (Architecture, Engineering, and Construction) industry moves toward decarbonization. Valued at USD 12.85 billion in 2025, the market is projected to reach USD 14.35 billion in 2026 and scale to USD 38.68 billion by 2035. This represents a robust CAGR of 11.65%. By 2032, the market is expected to surpass a critical valuation of approximately USD 28 billion, reflecting the mainstream adoption of renewable materials in residential and infrastructure projects.

Market Overview: What defines Bio-Based Construction Polymers?

Bio-based construction polymers are advanced materials derived from renewable biological sources—such as crop waste, plants, and organic matter—rather than traditional petroleum-based feedstocks. These materials are increasingly integrated into modern building systems for critical applications including high-performance insulation, weather-resistant coatings, and high-strength adhesives. As a Senior Analyst with 15 years in the chemicals sector, I recognize this market as the nexus where biotechnology meets structural engineering, providing a pathway to reduce the embodied carbon of the built environment while maintaining or exceeding the performance standards of synthetic predecessors.

What is the projected Market Growth?

The growth trajectory of this market is aggressive in both value and volume. Revenue is set to expand at an 11.65% CAGR, while the physical volume is anticipated to grow from 4.76 million tons in 2025 to 12.72 million tons by 2035 (a 10.33% CAGR). This expansion indicates a deepening market penetration as economies of scale begin to narrow the price gap between bio-based and conventional polymers.

What are the Key Market Trends?

-

Sustainability as a Premium Selling Strategy: Manufacturers are no longer treating “eco-friendly” as a side feature but are leveraging sustainability as their core value proposition to drive stronger cash flows.

-

Shift to Long-Term Value: There is a notable consumer and developer shift toward products that offer long-term durability and value over the cheapest upfront cost.

-

Region-Specific Material Innovation: Companies are tailoring polymer formulations to localized climates, such as high-heat resistance for the Middle East or moisture-stable resins for tropical zones.

-

Rise of Bio-PE and PHA: While Bio-PE remains a staple, Polyhydroxyalkanoates (PHA) are emerging as the high-growth frontier due to their superior biodegradability.

-

Adoption of Bio-Composites: The integration of natural fibers with bio-resins is creating a new class of structural materials that are both lightweight and carbon-sequestering.

What are the Recent Government Initiatives?

Governmental frameworks are transitioning from voluntary “Green Building” guidelines to mandatory low-carbon requirements. In the European Union, the Energy Performance of Buildings Directive (EPBD) is pushing for “Zero-Emission Buildings,” which directly incentivizes the use of bio-based insulation and structural materials. In Asia-Pacific, particularly China and India, national mandates to reduce plastic waste and promote “Circular Bio-economies” are providing subsidies for manufacturers using agricultural residues as polymer feedstocks. Furthermore, the U.S. General Services Administration (GSA) has recently expanded its “Buy Clean” initiative, prioritizing federal construction projects that utilize bio-based materials with lower embodied carbon. These systemic shifts ensure a guaranteed pipeline for bio-based construction polymers in the public sector, which is increasingly spilling over into private commercial development.

What are the Benefits of Using Bio-Based Construction Polymers?

The most immediate benefit is the reduction in carbon footprint; by utilizing plant-derived organic matter, these polymers often act as carbon sinks throughout their lifecycle. Beyond environmental impact, these materials often provide enhanced indoor air quality by reducing the VOC (Volatile Organic Compound) off-gassing common in synthetic adhesives and foams. Additionally, bio-based polymers like PHA offer end-of-life advantages, providing biodegradable or compostable options that traditional polymers cannot match, thereby reducing the burden of construction and demolition waste.

What Are the Key Factors Driving the Market?

The market is primarily driven by stringent environmental regulations and the global push toward Net Zero. The residential construction sector, currently holding a 38% share, is a massive driver as homeowners increasingly demand “healthy” and “green” living spaces. Additionally, volatility in petrochemical prices is forcing the industry to seek stable, renewable alternatives. The infrastructure segment is also a rising driver, growing at 12.40% as governments integrate bio-based waterproofing and structural polymers into large-scale public works to meet sustainability quotas.

Why is this Market Important?

The construction industry is responsible for nearly 40% of global $CO_2$ emissions. This market is important because it offers the most viable technical solution to replace fossil-fuel-intensive materials at scale. Without the transition to bio-based polymers in insulation, foams, and adhesives, achieving global climate targets would be virtually impossible for the construction sector.

Key Segments & Regional Insights

The market is characterized by a strong regional dominance in Asia-Pacific (44% share in 2025), where rapid urbanization and massive investments in green infrastructure are concentrated. However, the Middle East & Africa is the fastest-growing region (12.90% CAGR) as they diversify their economies and invest in sustainable cities.

-

By Polymer Type: Bio-based Polyethylene (Bio-PE) leads with a 26% share, but PHA is the growth leader at 13.60% CAGR.

-

By Application: Insulation materials dominate (29% share), though Composites are surging at 12.80% CAGR.

-

By Form: Foams are the most common form (33% share), essential for the insulation segment.

Competitive Landscape: Top Companies

The competitive landscape is a mix of traditional chemical giants and specialized bio-technology firms. Recent strategic moves include vertical integration with agricultural suppliers and the development of “next-gen” PHA for structural use.

1. Braskem S.A.

-

About: A Brazilian petrochemical company that is the world’s leading producer of biopolymers.

-

Products: I’m green™ Bio-based Polyethylene (Bio-PE) used in building pipes and films.

-

Market Cap: ~USD 4.5 – 5.5 Billion (Fluctuating).

2. BASF SE

-

About: The largest chemical producer in the world, heavily investing in the “ChemCycling” and bio-based resin sectors.

-

Products: Bio-based polyols for foams and insulation; ecovio® for construction films.

-

Market Cap: ~USD 45 – 55 Billion.

3. Corbion N.V.

-

About: A Dutch food and biochemicals company specializing in lactic acid and its derivatives.

-

Products: Bio-based resins and Luminy® PLA used in composites and coatings.

-

Market Cap: ~USD 1.5 – 2 Billion.

4. Danimer Scientific

-

About: A leading developer and manufacturer of biodegradable biopolymers.

-

Products: Nodax® PHA, which is seeing rapid adoption in the waterproofing and film segments.

-

Market Cap: ~USD 100 – 150 Million (High-growth small cap).

Data Presentation & Trade Insights

| Metric | 2025 (Base) | 2035 (Projected) | Growth Rate (CAGR) |

| Market Value (USD) | $12.85 Billion | $38.68 Billion | 11.65% |

| Market Volume (Tons) | 4.76 Million | 12.72 Million | 10.33% |

| Top Region | Asia Pacific | (44% Share) | Stable Dominance |

| Growth Leader (Type) | PHA | (13.60% CAGR) | Emerging High-Growth |

Recent Developments: In 2024-2025, several firms have launched liquid-form bio-polymers (growing at 12.60%) which are designed for on-site spray-foam insulation, significantly reducing labor costs while improving the thermal efficiency of residential buildings.

Which segment accounted for the largest Market share?

The Asia-Pacific region (44%), Bio-based Polyethylene (26%), and the Residential Construction sector (38%) currently hold the largest shares of the market. Within functional roles, Structural Materials lead with a 30% share, highlighting that bio-polymers are now trusted for load-bearing and core construction tasks.

Future of the Market & Conclusion

The future of the Bio-Based Construction Polymer market is inextricably linked to the “Circular Cities” concept. Looking toward 2035, I expect to see the rise of Carbon-Negative structural polymers—materials that don’t just reduce emissions but actually sequester more carbon than was used to produce them. The integration of AI in molecular design will likely yield waterproofing materials (growing at 12.70%) that are thinner, more durable, and completely biodegradable. As costs continue to stabilize, the bio-based construction polymer will transition from an alternative choice to the industry standard for high-performance, sustainable infrastructure.

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Email: [email protected]

Leave a Reply