Executive Summary

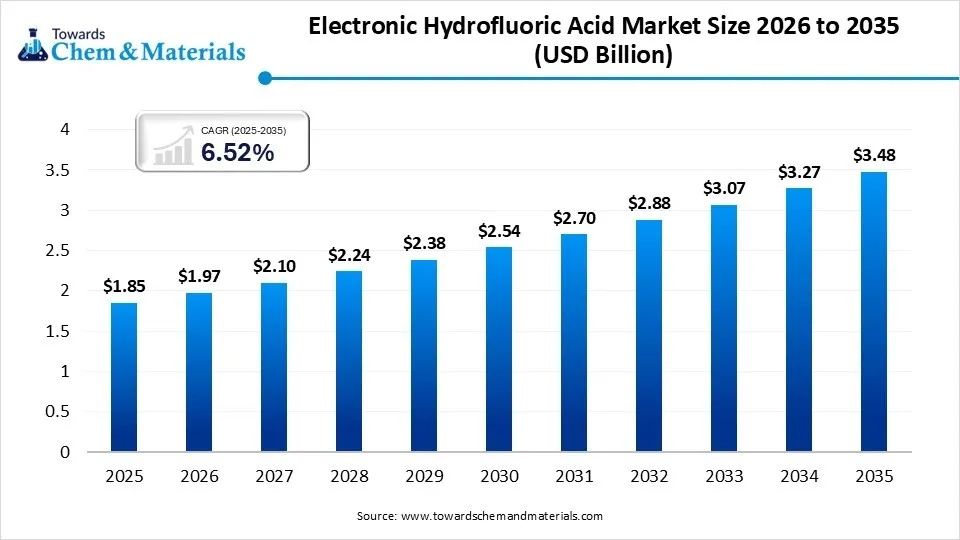

The global electronic hydrofluoric acid (e-HF) market is entering a phase of rapid value-acceleration. Valued at USD 1.85 billion in 2025, the market is projected to reach USD 3.48 billion by 2035. This growth, moving at a steady CAGR of 6.52%, is no longer just about volume; it is driven by the industry’s shift toward “Ultra-High Purity” (UHP) grades required for sub-5nm semiconductor nodes.

What is Driving the Surge in Electronic Hydrofluoric Acid Demand?

Several structural shifts in the electronics and energy sectors are making e-HF an indispensable commodity:

-

The “Angstrom Era” of Semiconductors: As chipmakers move toward 2nm and 3nm processes, the tolerance for metallic impurities has dropped to parts-per-trillion (ppt). This necessitates massive volumes of ultra-pure hydrofluoric acid for repeated wafer cleaning and etching cycles.

-

Solar PV Evolution: The transition from PERC to N-type (TOPCon/HJT) solar cells requires more intensive surface texturing, directly boosting e-HF consumption in the renewable energy sector.

-

The AI and 5G Infrastructure Boom: The build-out of high-performance computing (HPC) data centers is creating a secondary, yet powerful, demand pull for advanced logic chips.

Regional Performance: Asia Pacific’s Unshakable Dominance

In 2025, Asia Pacific dominated the market with a 40.00% revenue share, and this lead is expected to widen.

| Feature | Asia Pacific Dynamics |

| Manufacturing Hubs | Home to the world’s largest foundries (TSMC, Samsung, SK Hynix) and display giants. |

| Supply Chain Control | Significant control over raw material precursors (fluorspar) and sulfuric acid production. |

| Growth Catalyst | Massive state-led fab expansions in China and India’s emerging semiconductor ecosystem. |

Market Segmentation & Technological Shifts

1. Purity is the New Currency

The market is bifurcated by concentration, with the >49% concentration segment seeing the highest growth. High-end applications in AI-enabled devices and 5G infrastructure simply cannot function with lower-grade acids, which often lead to device yield failures.

2. Application Breakdown

-

Integrated Circuits (IC): The largest and most quality-sensitive segment.

-

Solar Energy: Increasing adoption of bifacial and high-efficiency panels.

-

Display Panels: High demand for OLED and next-gen LCD etching.

Competitive Landscape: The Pursuit of Purity

The market is moderately consolidated, with leaders focusing on vertical integration and geographic expansion near new semiconductor “mega-fabs.”

Key Market Participants:

-

Stella Chemifa Corporation: A global benchmark for high-purity chemistry.

-

Honeywell International Inc.: Leading the charge in the North American market with specialized grades for VLSI.

-

Solvay (Zhejiang Lansol): Focusing on sustainable purification and recycling technologies.

-

Morita Chemical Industries: A critical supplier for the Japanese and South Korean electronics corridors.

-

Emerging Players: Sunlit Chemical (Arizona expansion) and Tanfac Industries (India capacity doubling).

Future Outlook: Sustainability & Supply Resilience

Looking toward 2035, the industry faces a dual challenge: Safety and Sustainability. We expect to see a rise in closed-loop recycling systems at fab sites to reduce the environmental footprint of HF waste. Furthermore, as geopolitical tensions influence chemical trade, companies that secure localized “mine-to-fab” supply chains will emerge as the long-term winners.

Leave a Reply