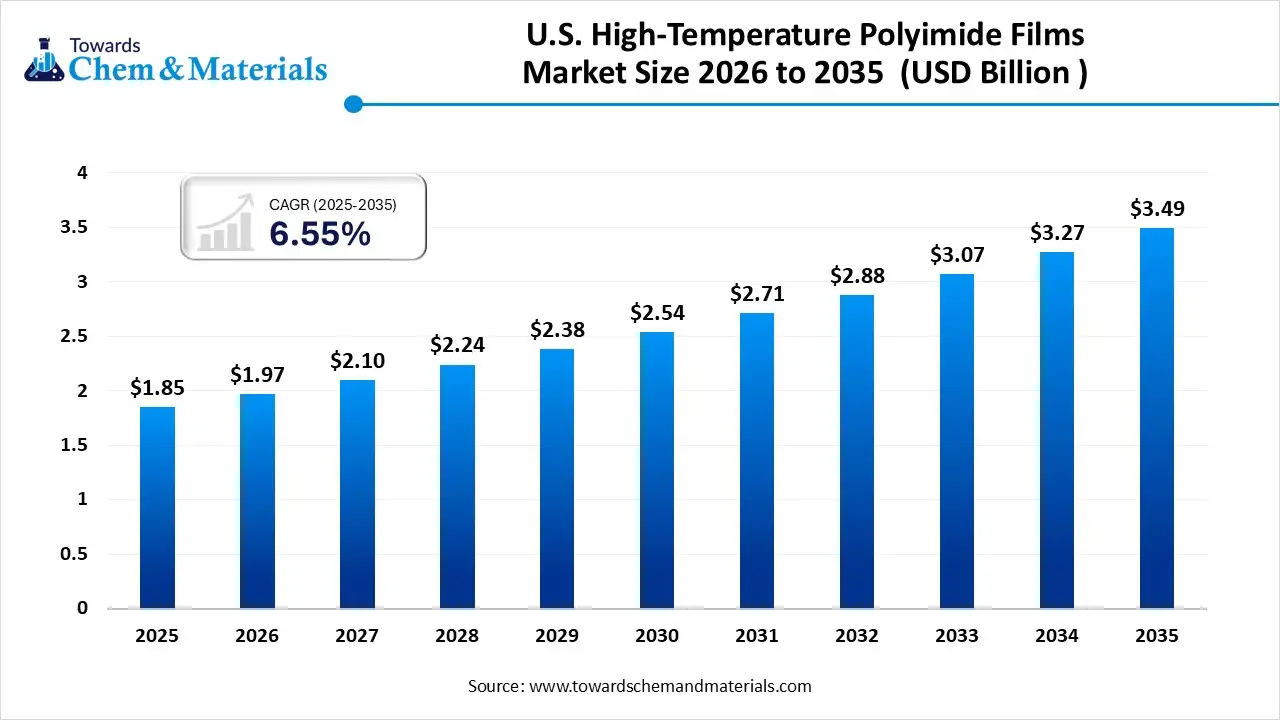

The United States high-temperature polyimide films market was valued at USD 1.85 billion in 2025 and is projected to grow from USD 1.97 billion in 2026 to approximately USD 3.49 billion by 2035, expanding at a CAGR of 6.55% from 2026 to 2035. The market growth is largely driven by the increasing demand for durable, lightweight, and high-performance insulation materials, particularly in emerging technologies such as electric vehicles (EVs), advanced electronics, and aerospace systems.

High-temperature polyimide (PI) films are engineered to withstand continuous service temperatures above 300°C–400°C, while offering exceptional dielectric strength, chemical resistance, mechanical durability, and thermal stability. These characteristics make them a preferred material in industries that require reliable insulation and high-performance flexible substrates. Growing investments in defense technologies, along with the rapid advancement of semiconductor packaging and EV power electronics, are further strengthening market expansion.

Download a sample of this report @ https://www.towardschemandmaterials.com/download-sample/6214

Market Highlights

-

By application: The flexible printed circuits (FPC) segment dominated the market with a 46.0% revenue share in 2025, driven by rising demand for lightweight and flexible electronic materials.

-

By product type: Conventional (amber) PI films led the market with a 45.5% share in 2025, supported by demand for compact and high-performance electronic components.

-

By end-use industry: Electronics & semiconductors accounted for the largest share of 54.3% in 2025, owing to expanding chip packaging and 5G infrastructure.

-

By thickness: The 25–50 μm segment held the largest share of 40.1% in 2025, widely used in aerospace components and flexible printed circuits.

Impact of Cutting-Edge Technologies on the Market

Technological advancements are significantly transforming the U.S. high-temperature polyimide films industry. Manufacturers are increasingly shifting from standard amber PI films to highly specialized and functional materials designed for harsh operating environments and advanced electronic systems.

The integration of nanoparticle-enhanced formulations is improving film performance by enhancing surface energy, dielectric strength, and mechanical durability. These improvements enable polyimide films to function effectively in extreme temperatures, high-voltage electronics, and next-generation aerospace systems. Additionally, innovations in roll-to-roll coating and precision film manufacturing are helping suppliers produce ultra-thin films for foldable displays and flexible electronics.

Trade Analysis: Import & Export Landscape

The global trade of polyimide films remains relatively specialized but strategically important. According to global export data, 69 shipments of polyimide films were exported worldwide between July 2024 and June 2025, involving 27 verified exporters and 26 buyers.

The United States continues to be one of the major importers of polyimide films, reflecting the country’s strong demand from electronics, aerospace, and automotive industries. This demand is further supported by the growing presence of semiconductor fabrication facilities and EV battery manufacturing plants.

Recent Market Trends

Several key trends are shaping the future growth of the market:

1. Rising demand from the electronics industry

Polyimide films are increasingly used in electronic components due to their excellent thermal resistance and electrical insulation properties. Their use in flexible circuits, microelectronics, and advanced semiconductor packaging continues to expand.

2. Growing adoption in aerospace applications

The aerospace sector is rapidly incorporating polyimide films because of their lightweight structure and exceptional heat resistance. These films serve as protective layers and thermal insulation materials in satellites, spacecraft, aircraft wiring systems, and propulsion components.

3. Sustainability initiatives in production

Major industry players are investing in sustainable manufacturing technologies, including improved recycling methods and environmentally friendly material formulations. These efforts aim to reduce environmental impact while maintaining the performance standards required by high-temperature applications.

Segmental Insights

Application Insights

Flexible Printed Circuits Dominated the Market in 2025

The flexible printed circuits (FPC) segment accounted for 46.0% of the market share in 2025. The growth of this segment is linked to the increasing demand for compact, flexible, and lightweight electronic devices, particularly in wearable technology, foldable smartphones, and high-frequency communication systems.

The rapid adoption of touchscreens, flexible displays, and 5G components also requires materials capable of maintaining electrical performance under high heat and mechanical stress.

The pressure-sensitive tapes segment is expected to register the fastest growth rate during the forecast period. These tapes are widely used as high-performance insulating materials in electric vehicles, aerospace components, and advanced electronic devices. In aerospace applications, they provide lightweight thermal insulation for engines, satellites, and spacecraft structures.

To own our research study instantly, Click here @ https://www.towardschemandmaterials.com/checkout/6214

Product Type Insights

Conventional (Amber) PI Films Led the Market

The conventional (amber) PI films segment held the largest share of 45.5% in 2025. These films remain widely used due to their proven reliability, thermal endurance, and electrical insulation capabilities in compact electronic components.

Growing investments by major manufacturers in the domestic electronics and industrial sectors are also supporting the demand for high-temperature insulation materials.

The colorless/transparent PI films segment is expected to experience the fastest CAGR during the forecast period. These films are increasingly used in foldable displays, wearable devices, and healthcare electronics. Their role as protective layers for flexible solar cells is also expanding due to supportive renewable energy policies.

End-Use Industry Insights

Electronics & Semiconductors Segment Dominated

The electronics & semiconductors industry accounted for the largest market share of 54.3% in 2025. This dominance is driven by the expansion of advanced semiconductor packaging, 5G networks, and flexible electronic devices.

The increasing adoption of wearable electronics, foldable smartphones, and high-density circuit boards is significantly boosting demand for heat-resistant and flexible polyimide substrates.

The automotive segment, particularly EV batteries and power electronics, is expected to record the fastest growth. Polyimide films provide high dielectric strength and superior thermal stability, enabling higher power density and improved safety in electric vehicle systems.

Thickness Insights

25–50 μm Segment Held the Largest Share

The 25–50 μm thickness segment captured 40.1% of the market share in 2025. This thickness range is widely used in aerospace systems, flexible printed circuits, and EV battery components, where high dielectric performance and chemical resistance are critical.

The <25 μm ultra-thin segment is anticipated to grow at the fastest rate during the forecast period. The growth is driven by increasing demand for bendable displays, compact electronic devices, and advanced flexible substrates. Additionally, manufacturers are investing in roll-to-roll coating technologies to improve production efficiency and yield for ultra-thin films.

You can place an order or ask any questions, please feel free to contact us at [email protected]

Recent Developments

-

In July 2025, Arkema and its affiliate PI Advanced Materials rebranded their flagship high-performance polyimide material as Zenimid™, aiming to expand its global footprint across aerospace, automotive, electronics, and industrial applications.

Key Companies in the U.S. High-Temperature Polyimide Films Market

Leading companies operating in the market include:

-

PI Advanced Materials

-

Taimide Tech Inc.

-

Ube Industries

-

Saint‑Gobain Performance Plastics

-

DuPont de Nemours, Inc.

-

Kaneka Corporation

-

Mitsubishi Gas Chemical Company

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Explore the comprehensive statistics and insights on healthcare industry data and its associated segmentation: Get a Subscription

Leave a Reply