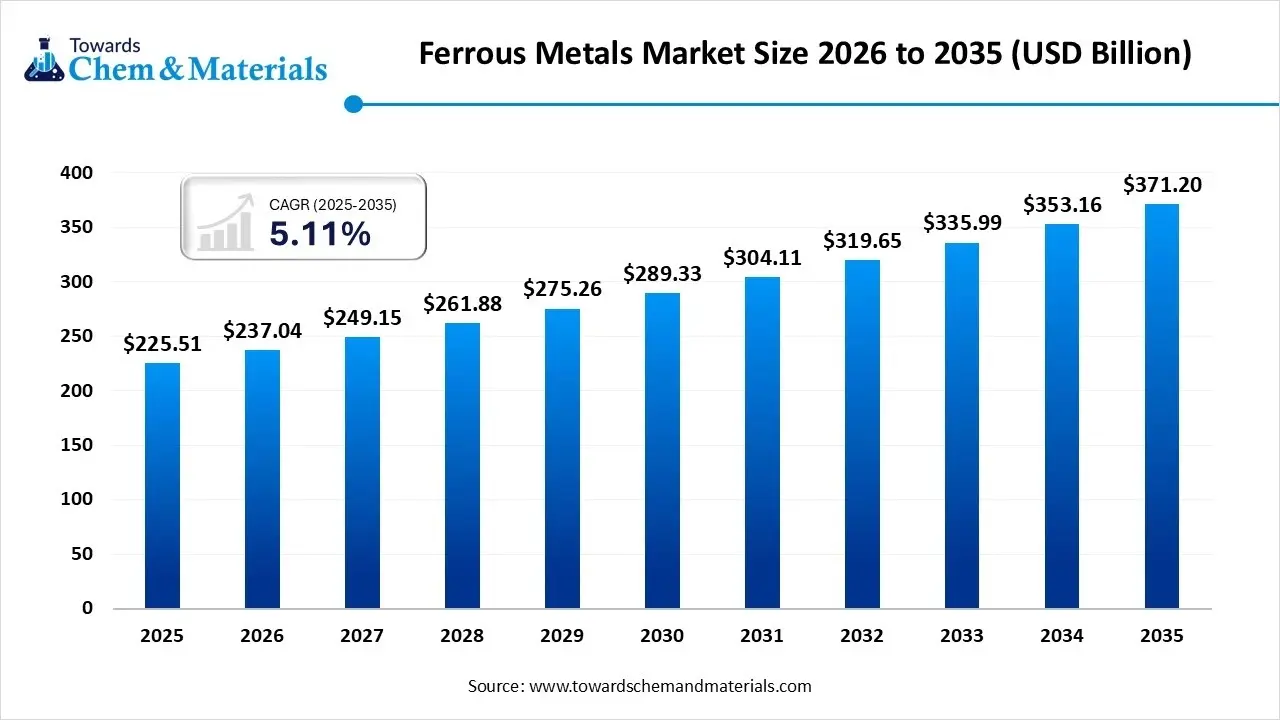

The global ferrous metals market continues to play a foundational role in the global industrial economy. In 2025, the market was valued at USD 225.51 billion and is projected to grow from USD 237.04 billion in 2026 to USD 371.20 billion by 2035, registering a CAGR of 5.11% during 2026–2035.

Growth is primarily driven by strong infrastructure development in emerging economies, sustained demand from the manufacturing and automotive sectors, and rapid urbanization worldwide.

Download a sample of this report @ https://www.towardschemandmaterials.com/download-sample/6226

Market Overview

Ferrous metals are metals and alloys that contain iron as their primary constituent. These include:

-

Carbon steel

-

Stainless steel

-

Cast iron

In 2026, the market is experiencing what analysts describe as a “low growth but high transformation” phase. While traditional demand from construction is moderating in some regions, specialty demand is accelerating due to:

-

Energy transition infrastructure (renewable energy plants, transmission systems)

-

Expansion of AI-powered data centers

-

Advanced mobility and transportation solutions

This structural shift is redefining demand patterns across material types and product forms.

Market Highlights

-

Asia Pacific dominated the market in 2025, accounting for 58% of total revenue share, driven by massive construction and industrial activities.

-

By material type, the stainless steel segment led with a 45% revenue share in 2025, supported by urbanization and corrosion-resistant infrastructure demand.

-

By product form, flat steels accounted for 49% share in 2025, owing to growing demand for lightweight and high-strength materials.

-

By application, the construction & infrastructure segment dominated with 40% share, backed by rising population density and smart city development.

Regional Insights

Asia Pacific – The Market Leader

Asia Pacific remains the dominant region due to:

-

Expanding construction activities

-

Rapid industrialization

-

Government-led infrastructure programs

-

Strong steel production capabilities in China, India, Japan, and South Korea

The region’s 58% revenue share in 2025 underscores its critical role in global steel manufacturing and consumption.

Trade Analysis: Import & Export Statistics

Global trade flows remain vital to the ferrous metals ecosystem.

According to the American Iron and Steel Institute (AISI) and preliminary U.S. Census Bureau data:

-

U.S. steel imports reached 2,123,000 net tons (NT) in December 2024, reflecting a 2.7% increase over November.

-

Finished steel imports rose 14.3%, totaling 1,820,000 NT.

Between June 2024 and May 2025:

-

26,564 shipments of metal ferrous products were imported globally.

-

These shipments involved 26,564 exporters and 22,113 verified buyers.

Top Importers

-

Russia

-

Ukraine

-

Uzbekistan

Top Exporters

-

China

-

Germany

-

Russia

These trade movements highlight the geopolitical and industrial concentration of ferrous metal production and consumption.

Key Market Trends

1. Green Steel Revolution

The push toward sustainable steel production is reshaping the industry. Companies are transitioning from coal-based blast furnaces to hydrogen-based direct reduced iron (DRI) processes.

Benefits include:

-

Reduced carbon emissions

-

Lower long-term operational costs

-

Compliance with tightening environmental regulations

Green hydrogen adoption is expected to be a defining transformation factor over the forecast period.

2. AI and Industry 4.0 Integration

Rapid technological innovation is improving efficiency and profitability. The adoption of:

-

AI-powered predictive maintenance

-

IoT-enabled smart production systems

-

Digital twins and automated quality inspection

These technologies enhance uptime, reduce unexpected shutdowns, and optimize supply chains.

3. Recycling and Circular Economy Expansion

The growing emphasis on scrap recycling is significantly influencing market dynamics. Increased electric arc furnace (EAF) adoption:

-

Conserves natural resources

-

Reduces carbon footprints

-

Lowers manufacturing costs

Sustainability is now both an environmental and financial imperative.

To own our research study instantly, Click here @ https://www.towardschemandmaterials.com/checkout/6226

Report Scope

| Report Attribute | Details |

|---|---|

| Market Size in 2026 | USD 237.04 Billion |

| Revenue Forecast in 2035 | USD 371.20 Billion |

| Growth Rate | CAGR 5.11% |

| Forecast Period | 2026–2035 |

| Base Year | 2025 |

| Dominant Region | Asia Pacific |

| Segments Covered | By Material Type, Product Form, Application, Region |

How Cutting-Edge Technologies Are Transforming the Market

Advanced technologies are revolutionizing ferrous metal production and processing:

-

Hydrogen-based reduction methods

-

AI-driven material sorting systems

-

IoT-enabled smart manufacturing

-

Automated quality inspection systems

These innovations are:

-

Improving product precision

-

Reducing CO₂ emissions

-

Enhancing operational efficiency

-

Optimizing supply chains

The transformation is pushing the industry toward high-performance, low-carbon, and digitally integrated production systems.

You can place an order or ask any questions, please feel free to contact us at [email protected]

Recent Developments

In November 2025, Shanghai Metals Market (SMM) announced the operational launch of its Korea Office. This expansion reflects SMM’s strategic commitment to the Northeast Asian market and its emphasis on delivering localized services to regional clients.

Competitive Landscape

The global ferrous metals market is highly competitive, with vertically integrated steelmakers and mining giants dominating the landscape.

Leading Companies

-

ArcelorMittal S.A. – The world’s second-largest steel producer, operating a vertically integrated model from iron ore mining to finished steel production.

-

Baoshan Iron & Steel Co., Ltd. – A subsidiary of China Baowu Steel Group and one of China’s premier steel manufacturers.

-

Nippon Steel Corporation – Japan’s largest steel producer, focused on high-grade steel and global capacity expansion.

-

Tata Steel Limited

-

Nucor Corporation

-

JFE Holdings Inc.

-

thyssenkrupp AG

-

BHP Group

-

Rio Tinto Group

-

Vale S.A.

-

Hyundai Steel Company

-

United States Steel Corporation

-

Gerdau S.A.

-

Cleveland-Cliffs Inc.

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Explore the comprehensive statistics and insights on healthcare industry data and its associated segmentation: Get a Subscription

Leave a Reply