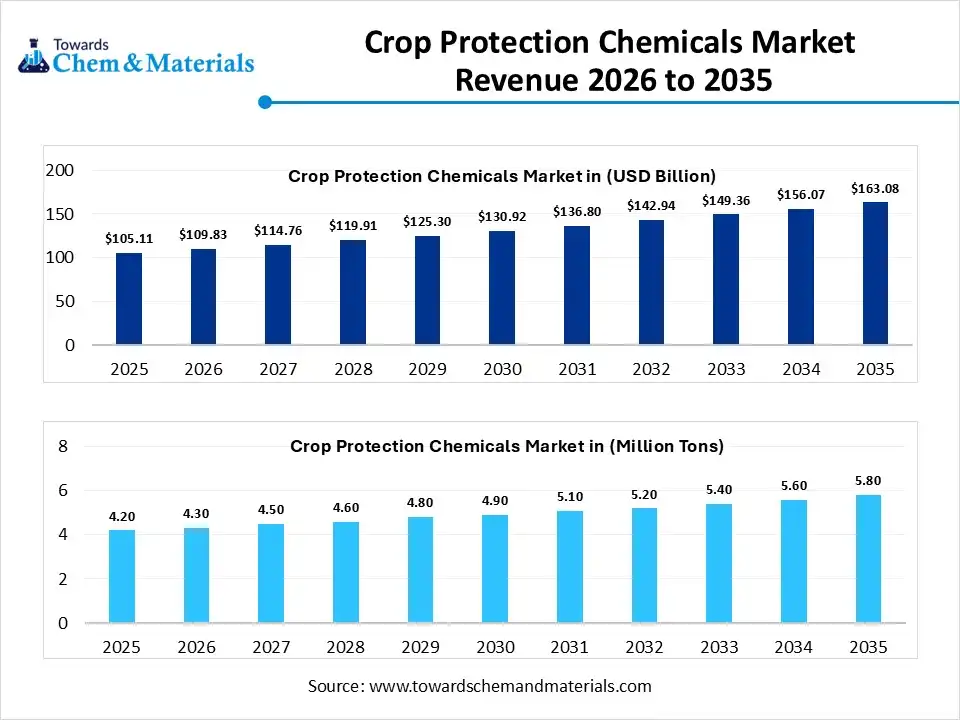

The global agricultural landscape is standing at a critical crossroads. As we move into the 2026-2035 forecast period, the Crop Protection Chemicals Market is no longer just about yield maximization; it has become a linchpin for global food security, environmental stewardship, and technological integration. Valued at USD 109.83 billion in 2026, the market is projected to reach USD 163.08 billion by 2035, growing at a steady CAGR of 4.49%.

This growth is underpinned by a dual necessity: feeding a population projected to approach 10 billion by mid-century while operating under the increasingly stringent “green” mandates of global regulatory bodies. For manufacturers, suppliers, and stakeholders, the next decade will be defined by the transition from broad-spectrum synthetic dominance to precision-targeted biological solutions.

Market Overview: Current Size and Volume Projections

The baseline for this analysis begins in 2025, where the market was estimated at USD 105.11 billion. In terms of physical volume, the industry is moving from 4.20 million tons in 2025 to an estimated 5.80 million tons by 2035, reflecting a CAGR of 3.21%. The discrepancy between value and volume growth suggests a market shift toward high-value, specialized formulations—meaning farmers are increasingly willing to pay more for “smarter” chemicals that require lower dosage per hectare.

Regional Dominance: The Asia Pacific Powerhouse

In 2025, the Asia Pacific region asserted its dominance with a 38.43% volume share. This leadership is driven by the massive agricultural output of China and India, coupled with rapid modernization of farming techniques in Southeast Asia. Conversely, North America is expected to maintain a robust CAGR of 3.77%, fueled by the adoption of ultra-high-tech precision agriculture tools.

Market Dynamics: The Drivers of Transformation

The “Why” behind the market’s steady climb involves a complex interplay of social, environmental, and technological factors.

1. Escalating Global Food Demand

Shrinking arable land per capita is forcing a transition toward “vertical” productivity gains. With urbanization claiming once-fertile plains, the remaining farmland must produce significantly higher yields. Crop protection chemicals—herbicides, fungicides, and insecticides—remain the primary defense against the estimated 20% to 40% of global crop yields lost annually to pests and diseases.

2. The Precision Agriculture Revolution

The integration of AI, GPS, and Drone technology is fundamentally changing how chemicals are applied. Variable-rate application (VRA) allows farmers to treat only the affected parts of a field rather than blanket-spraying. This trend is a double-edged sword: it reduces the total volume of chemicals needed but increases the demand for specialized, high-performance formulations that can be delivered via drone-mounted sprayers or smart tractors.

3. Climate Change and “Pest Migration”

Warmer global temperatures are altering the geographic boundaries of pests. Species previously confined to tropical zones are moving into temperate regions (e.g., the expansion of Fall Armyworm across Asia and Africa). This creates an urgent need for “emergency” chemical registrations and the development of products effective against invasive species in new climates.

4. The Biological Pivot (Biopesticides)

Perhaps the most significant trend is the rise of biopesticides, which are expected to grow at the fastest CAGR of 4.47% in volume terms. Driven by the EU’s “Farm to Fork” strategy and similar global initiatives, biopesticides—derived from bacteria, fungi, and plant extracts—are moving from niche organic use into mainstream Integrated Pest Management (IPM) programs.

Segment Analysis: Key Areas of Growth

To understand where the capital is flowing, we must look at the specific segments within the crop protection ecosystem.

By Product Type: Herbicides Lead, Biopesticides Sprint

-

Herbicides: This remains the largest segment, holding a 48.23% volume share in 2025. The high cost and shortage of manual labor for weeding in developing nations make chemical herbicides the only viable economic option for large-scale grain production.

-

Biopesticides: While smaller in total volume, this segment is the primary focus of R&D. Innovations in RNAi (RNA interference) technology are allowing for species-specific pest control, which represents the “Holy Grail” of crop protection: killing the pest without harming beneficial insects like bees.

By Crop Type: Cereals and Grains

The Cereals and Grains segment led the market in 2025 with a 35.00% revenue share. Wheat, maize, and rice are the foundation of global caloric intake, and their vast cultivation areas require the highest total volume of protection chemicals. However, the Fruits and Vegetables segment is seeing higher value growth due to strict residue limits (MRLs) in export markets, necessitating more expensive, low-tox solutions.

By Mode of Application: Foliar Spray vs. Seed Treatment

-

Foliar Spray: Accounted for 55.3% of revenue in 2025. Its ease of use and immediate effect make it the standard for “reactive” pest management.

-

Seed Treatment: Expected to see a surge in adoption as a “proactive” measure. By coating seeds with protective agents before planting, farmers can reduce the total chemical load on the environment and ensure early-stage plant health.

| Company | Key Strategic Focus (2026-2035) |

| BASF SE | Heavy investment in digital farming platforms (Xarvio) and biosolutions. |

| Bayer Cropscience | Focusing on “Short Stature Corn” and biologicals to offset glyphosate litigation. |

| Corteva | Innovation in seed-applied technologies and sustainable chemistry. |

| Syngenta Group | Expanding its “Green Growth” portfolio and strengthening its APAC footprint via ChemChina. |

| FMC Corporation | Leading in the development of new synthetic modes of action to combat resistance. |

Trade Analysis: Import and Export Realities

Trade data reveals the shifting centers of chemical production.

-

Top Exporters: The United States (1,075 shipments) and China (950 shipments) remain the global hubs of agrochemical manufacturing.

-

Emerging Player: India has shown a 90% increase in crop protection exports recently, with major shipments going to Russia, Nigeria, and Vietnam.

-

Top Destinations: Uzbekistan, Russia, and Brazil are among the largest importers, highlighting the critical role these chemicals play in the developing “breadbaskets” of the world.

Regulatory Landscape: A Global Heatmap

Regulatory pressure is the single greatest “restraint” on the market, yet it is also the greatest “driver” of innovation.

-

Europe (EFSA/EC): The most stringent. The EU’s focus on “hazard-based” bans means many traditional active ingredients are being phased out, forcing a rapid (and expensive) switch to biologicals.

-

North America (EPA): Follows a “risk-based” approach. While more lenient than Europe, the EPA is increasing scrutiny on environmental impacts, particularly concerning pollinators.

-

Latin America (Brazil): A high-growth region but currently reforming its Pesticide Law to balance the need for intensive agricultural exports with environmental protection.

Conclusion: The Path Ahead

The Crop Protection Chemicals Market (2026-2035) is evolving from a commodity-based industry into a technology-driven service sector. Success for manufacturers will no longer be measured by the “gallons sold” but by the “yield protected.” As biopesticides merge with precision application and AI-driven forecasting, the industry will move toward a “Zero-Residue” future that satisfies both the hungry world and the cautious regulator.

Frequently Asked Questions

What is the projected CAGR for the crop protection chemicals market? The market is expected to grow at a Compound Annual Growth Rate (CAGR) of 4.49% from 2026 to 2035.

Who are the key stakeholders in the crop protection industry? The primary stakeholders include multinational chemical manufacturers (such as Bayer, Syngenta, and BASF), agricultural cooperatives, government regulatory bodies (like the EPA and EFSA), and commercial farmers.

Which segment is expected to lead the market by 2035? In terms of product type, the herbicides segment currently holds the largest share, but the biopesticides segment is projected to experience the fastest growth rate throughout the forecast period.

Which region dominates the global market in terms of volume? The Asia Pacific region is the dominant market, accounting for a 38.43% volume share as of 2025, largely due to high agricultural activity in China and India.

What are the primary factors driving the growth of biopesticides? The growth of biopesticides is driven by increasing environmental regulations against synthetic chemicals, rising consumer demand for organic food, and the development of Integrated Pest Management (IPM) strategies.

Leave a Reply