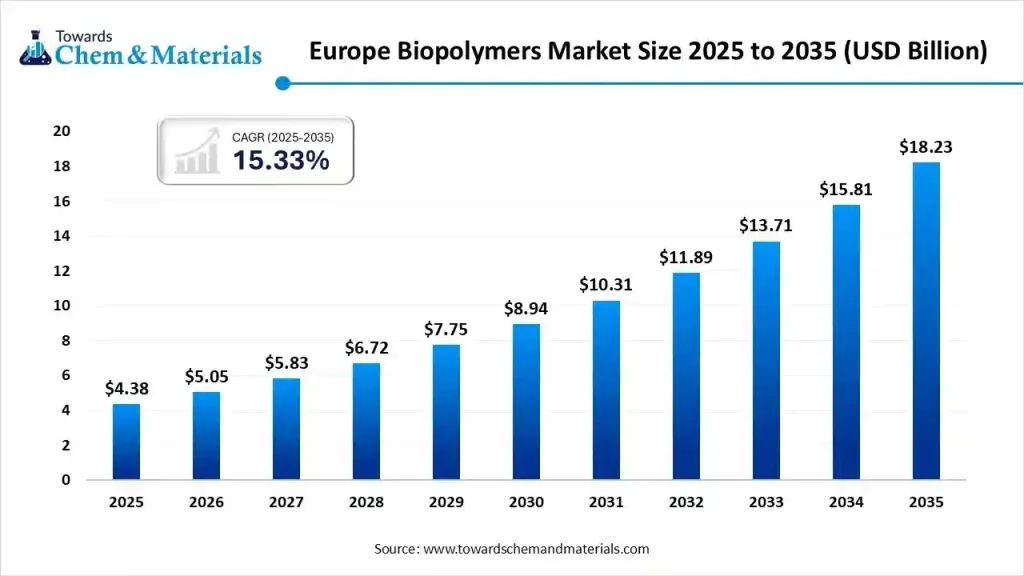

The European biopolymers landscape stands at a pivotal junction in 2025, actively driving the global transition away from fossil-fuel-based plastics. Valuing the market at an impressive USD 4.38 billion this year, industry analysts project a steep ascent. The market expects to surpass $5.05 billion in 2026 and will likely achieve a substantial USD 18.23 billion by 2035, expanding at a robust Compound Annual Growth Rate (CAGR) of 15.33% across this forecast period. This dramatic expansion is not incidental; it reflects a powerful synergy between intensifying environmental legislation, crucial technological innovations, and overwhelming consumer demand for demonstrably sustainable products.

Biopolymers, or bioplastics, involve the production and trade of polymers derived from biodegradable or renewable sources. These materials directly serve as sustainable alternatives to conventional plastics, primarily addressing the vast packaging needs and aligning with the rigorous sustainability goals set by the European Union.

Get All the Details in Our Solutions –Download Sample: https://www.towardschemandmaterials.com/download-sample/6079

Key Takeaways for 2025

As the market establishes its foundation in 2025, specific segments drive current demand and growth:

- Product Dominance: The bio-PE (bio-polyethylene) segment claims the largest share of the market. Its compatibility with existing polyethylene infrastructure and its bio-based origin make it an immediate and practical substitution choice for manufacturers.

- Application Leadership: The bottle segment holds the largest market share, highlighting the immediate priority to decarbonize high-volume, single-use rigid packaging.

- End-Use Powerhouse: The packaging sector dominates the market share, functioning as the primary accelerator for biopolymer adoption across food, beverage, and personal care industries.

2025 Buyer Playbook: What Actually Decides Deals

In 2025, buyers — spanning from major fast-moving consumer goods (FMCG) brands to specialty medical device manufacturers — make procurement decisions based on an intricate blend of three critical factors: Compliance, Performance, and Supply Chain Resilience.

- Regulatory Certainty: Companies prioritize materials that ensure immediate and future compliance with stringent EU regulations, such as those governing packaging and packaging waste. A certified compostable or verifiable bio-based material significantly de-risks future product lines.

- Performance Parity: Biopolymers must perform as effectively as their fossil-fuel counterparts. Deals are finalized when materials, such as bio-PE or high-performance bio-polyamides, offer comparable mechanical strength, barrier properties, and thermal stability while maintaining processability on existing manufacturing equipment.

- Scalable Feedstock: Buyers seek assurance of a stable, sustainable, and non-food-competitive raw material supply. Innovations in feedstock, such as those leveraging agricultural waste or synthetic biology (e.g., microbial fermentation for PHA), enhance supply chain resilience and secure long-term contracts.

- End-of-Life Solution: The deciding factor often pivots on the material’s certified end-of-life pathway — whether it is compatible with existing mechanical recycling streams (like bio-PE) or certified for industrial composting (like PLA or PBAT).

Quick Comparison Matrix

The European biopolymers ecosystem divides naturally into material innovators and market integrators.

Material innovators, such as BASF, Novamont, and NatureWorks, dedicate their efforts to creating the fundamental building blocks. BASF focuses on complex biodegradable compounds like ecoflex® and ecovio® that enable organic recycling for waste collection. Contrastingly, NatureWorks champions polylactic acid (PLA) with Ingeo™, betting on a solution that is both bio-based and recyclable via advanced sorting technologies. Novamont commits to a fully integrated bioeconomy, converting industrial sites to produce their signature Mater-Bi® from renewable agricultural sources.

Meanwhile, chemical synthesis firms like Arkema and Versalis focus on high-performance applications. Arkema utilizes specialty bio-based polyamides, Rilsan® PA11, derived from castor oil, to replace metal in demanding automotive and electronics sectors. Versalis, leveraged through its ownership of Novamont, focuses on integrating these bio-based solutions into the mainstream food packaging market.

The market integrators, including packaging giants Mondi Group and Amcor, act as the final bridge to the consumer. Mondi offers industrially compostable paper packaging and mono-material solutions, while Amcor drives adoption by substituting conventional plastics with drop-in, bio-based alternatives, such as bio-PE. Lastly, leaders in regulatory and performance compliance like DuPont ensure high-end, demanding sectors like medical devices and pharmaceuticals adopt these advanced, often customized, bio-materials.

For more information, visit the Towards Chemical and Materials website or email the team at [email protected]| +1 804 441 9344

More Insights in Towards Chemical and Materials:

· U.S. Biopolymers Market: The U.S. biopolymers market size is calculated at USD 5.01 billion in 2025 and is predicted to increase from USD 5.81 billion in 2026 and is projected to reach around USD 22.16 billion by 2035, The market is expanding at a CAGR of 16.03% between 2026 and 2035. The global shift towards plastic dependence reduction has fueled sector growth in the past few years.

· Biopolymers Market : The global biopolymers market size was valued at USD 19.85 billion in 2024, grew to USD 21.93 billion in 2025, and is expected to hit around USD 53.68 billion by 2034, growing at a compound annual growth rate (CAGR) of 10.46% over the forecast period from 2025 to 2034. The sudden shift towards sustainable manufacturing practices is expected to attract increased capital and investment in manufacturing.

· Biopolymer Coatings Market: The global biopolymer coatings market size is calculated at USD 40.01 billion in 2025 and is predicted to increase from USD 44.23 billion in 2026 and is projected to reach around USD 109.08 billion by 2035, The market is expanding at a CAGR of 10.55% between 2025 and 2035. Increasing consumer demand for sustainable products is the key factor driving market growth.

· Lignin-based Biopolymers Market: The global lignin-based biopolymers market size accounted for USD 1.32 billion in 2024 and is predicted to increase from USD 1.38 billion in 2025 to approximately USD 2.07 billion by 2034, expanding at a CAGR of 8.11% from 2025 to 2034.

·Polymer Coated Fabrics Market : The global polymer coated fabrics market size is calculated at USD 24.06 billion in 2025 and is predicted to increase from USD 25.32 billion in 2026 and is projected to reach around USD 40.13 billion by 2035, The market is expanding at a CAGR of 5.25% between 2025 and 2035

What’s Next (2025–2030 Outlook)

The outlook between 2025 and 2030 anticipates rapid market maturity. The primary engine of growth will shift from simple substitution to high-performance integration.

- Bio-PET and Films Drive Volume: While bio-PE and bottles dominate initially, the bio-PET product segment and the films application segment are poised for the fastest CAGR over the forecast period. Bio-PET’s structural integrity makes it ideal for beverage and food containers, and the massive market for flexible packaging (films) means even marginal penetration will translate into immense volume growth.

- Automotive Decarbonization: The automotive segment expects to grow at the fastest CAGR among all end-uses. Manufacturers increasingly use biopolymers for durable interior parts and lightweight components, reducing overall vehicle mass and carbon footprint.

- Advanced Feedstock Innovation: Ongoing innovations in feedstock development, particularly synthetic biology like microbial fermentation for PHA (polyhydroxyalkanoates), will pave the way for cost-effective and scalable biopolymer manufacturing. This move reduces reliance on first-generation feedstocks, improving sustainability credentials.

- Circular Economy Mandate: The market sees a pronounced shift toward bio-based but non-biodegradable plastics. Businesses are actively seeking durable, high-performance substitutes that maintain compatibility with established mechanical recycling systems, aligning with the circular economy principle of maximizing material use rather than purely composting.

Why Competition Is Intensifying

Competition intensifies due to three key pressures converging simultaneously:

- Regulatory Pressure: The rapid implementation of strict environmental regulations and policies by the European Commission necessitates immediate material changes for packaging, agricultural films, and consumer goods. This compliance deadline forces companies to procure or develop biopolymer solutions quickly, driving a competitive race for technology and market share.

- Performance Parity: Biopolymer producers have successfully invested in technological innovations that enhance material performance, closing the gap with conventional plastics in terms of durability, barrier protection, and processing capabilities. This technological maturity opens up high-value application sectors like automotive and medical, attracting larger, established chemical companies.

- Consumer Sentiment: Growing consumer demand acts as a persistent market driver. Brands understand that eco-friendly packaging offers a significant competitive advantage, leading them to demand innovative, certified, and cost-competitive materials from their suppliers, thereby intensifying the rivalry among polymer manufacturers.

Europe’s Green Leap: Unpacking the $4.38 Billion Biopolymers Market in 2025

The European biopolymers landscape stands at a pivotal junction in 2025, actively driving the global transition away from fossil-fuel-based plastics. Valuing the market at an impressive USD 4.38 billion this year, industry analysts project a steep ascent.1 The market expects to surpass $5.05 billion in 2026 and will likely achieve a substantial USD 18.23 billion by 2035, expanding at a robust Compound Annual Growth Rate (CAGR) of 15.33% across this forecast period.2 This dramatic expansion is not incidental; it reflects a powerful synergy between intensifying environmental legislation, crucial technological innovations, and overwhelming consumer demand for demonstrably sustainable products.

Biopolymers, or bioplastics, involve the production and trade of polymers derived from biodegradable or renewable sources.3 These materials directly serve as sustainable alternatives to conventional plastics, primarily addressing the vast packaging needs and aligning with the rigorous sustainability goals set by the European Union.4

Key Takeaways for 2025

As the market establishes its foundation in 2025, specific segments drive current demand and growth:

- Product Dominance: The bio-PE (bio-polyethylene) segment claims the largest share of the market. Its compatibility with existing polyethylene infrastructure and its bio-based origin make it an immediate and practical substitution choice for manufacturers.

- Application Leadership: The bottle segment holds the largest market share, highlighting the immediate priority to decarbonize high-volume, single-use rigid packaging.

- End-Use Powerhouse: The packaging sector dominates the market share, functioning as the primary accelerator for biopolymer adoption across food, beverage, and personal care industries.5

2025 Buyer Playbook: What Actually Decides Deals

In 2025, buyers — spanning from major fast-moving consumer goods (FMCG) brands to specialty medical device manufacturers — make procurement decisions based on an intricate blend of three critical factors: Compliance, Performance, and Supply Chain Resilience.

- Regulatory Certainty: Companies prioritize materials that ensure immediate and future compliance with stringent EU regulations, such as those governing packaging and packaging waste. A certified compostable or verifiable bio-based material significantly de-risks future product lines.

- Performance Parity: Biopolymers must perform as effectively as their fossil-fuel counterparts. Deals are finalized when materials, such as bio-PE or high-performance bio-polyamides, offer comparable mechanical strength, barrier properties, and thermal stability while maintaining processability on existing manufacturing equipment.

- Scalable Feedstock: Buyers seek assurance of a stable, sustainable, and non-food-competitive raw material supply. Innovations in feedstock, such as those leveraging agricultural waste or synthetic biology (e.g., microbial fermentation for PHA), enhance supply chain resilience and secure long-term contracts.6

- End-of-Life Solution: The deciding factor often pivots on the material’s certified end-of-life pathway — whether it is compatible with existing mechanical recycling streams (like bio-PE) or certified for industrial composting (like PLA or PBAT).

Quick Comparison Matrix

The European biopolymers ecosystem divides naturally into material innovators and market integrators. Material innovators, such as BASF, Novamont, and NatureWorks, dedicate their efforts to creating the fundamental building blocks. BASF focuses on complex biodegradable compounds like ecoflex® and ecovio® that enable organic recycling for waste collection.7 Contrastingly, NatureWorks champions polylactic acid (PLA) with Ingeo™, betting on a solution that is both bio-based and recyclable via advanced sorting technologies.8 Novamont commits to a fully integrated bioeconomy, converting industrial sites to produce their signature Mater-Bi® from renewable agricultural sources.

Meanwhile, chemical synthesis firms like Arkema and Versalis focus on high-performance applications.9 Arkema utilizes specialty bio-based polyamides, Rilsan® PA11, derived from castor oil, to replace metal in demanding automotive and electronics sectors.10 Versalis, leveraged through its ownership of Novamont, focuses on integrating these bio-based solutions into the mainstream food packaging market.11

The market integrators, including packaging giants Mondi Group and Amcor, act as the final bridge to the consumer.12 Mondi offers industrially compostable paper packaging and mono-material solutions, while Amcor drives adoption by substituting conventional plastics with drop-in, bio-based alternatives, such as bio-PE. Lastly, leaders in regulatory and performance compliance like DuPont ensure high-end, demanding sectors like medical devices and pharmaceuticals adopt these advanced, often customized, bio-materials.13

What’s Next (2025–2030 Outlook)

The outlook between 2025 and 2030 anticipates rapid market maturity. The primary engine of growth will shift from simple substitution to high-performance integration.

- Bio-PET and Films Drive Volume: While bio-PE and bottles dominate initially, the bio-PET product segment and the films application segment are poised for the fastest CAGR over the forecast period. Bio-PET’s structural integrity makes it ideal for beverage and food containers, and the massive market for flexible packaging (films) means even marginal penetration will translate into immense volume growth.

- Automotive Decarbonization: The automotive segment expects to grow at the fastest CAGR among all end-uses. Manufacturers increasingly use biopolymers for durable interior parts and lightweight components, reducing overall vehicle mass and carbon footprint.

- Advanced Feedstock Innovation: Ongoing innovations in feedstock development, particularly synthetic biology like microbial fermentation for PHA (polyhydroxyalkanoates), will pave the way for cost-effective and scalable biopolymer manufacturing.14 This move reduces reliance on first-generation feedstocks, improving sustainability credentials.

- Circular Economy Mandate: The market sees a pronounced shift toward bio-based but non-biodegradable plastics. Businesses are actively seeking durable, high-performance substitutes that maintain compatibility with established mechanical recycling systems, aligning with the circular economy principle of maximizing material use rather than purely composting.

Why Competition Is Intensifying

Competition intensifies due to three key pressures converging simultaneously:

- Regulatory Pressure: The rapid implementation of strict environmental regulations and policies by the European Commission necessitates immediate material changes for packaging, agricultural films, and consumer goods. This compliance deadline forces companies to procure or develop biopolymer solutions quickly, driving a competitive race for technology and market share.

- Performance Parity: Biopolymer producers have successfully invested in technological innovations that enhance material performance, closing the gap with conventional plastics in terms of durability, barrier protection, and processing capabilities.15 This technological maturity opens up high-value application sectors like automotive and medical, attracting larger, established chemical companies.

- Consumer Sentiment: Growing consumer demand acts as a persistent market driver.16 Brands understand that eco-friendly packaging offers a significant competitive advantage, leading them to demand innovative, certified, and cost-competitive materials from their suppliers, thereby intensifying the rivalry among polymer manufacturers.

How These Leaders Compete

Competition among market leaders centers on two areas: technological specialization and value chain control.

Company StrategyFocus AreaCompetitive AdvantageBASF SEDiversified BiodegradablesLeverages scale and R&D to offer performance-driven, certified compostable materials (ecoflex®, ecovio®), providing extensive application support and life cycle analysis to major brands.Novamont S.p.A.Integrated BioeconomyCompetes through a unique, vertically integrated production model, converting brownfield sites and utilizing plant-based sources to produce its flagship Mater-Bi®, ensuring regional sourcing and a dedicated focus on compostability and soil health.Arkema S.A.High-Performance Bio-BasedSpecializes in high-value, non-biodegradable materials (Rilsan® PA11) derived 100% from castor oil, targeting demanding applications (automotive, aerospace) where performance and durability outweigh compostability requirements.Versalis S.p.A.Portfolio DiversificationAs the chemical arm of Eni, it expands its traditional portfolio by integrating Novamont’s technologies, enabling it to offer both conventional and bio-based/compostable solutions, thereby serving a broader range of packaging clients.Mondi GroupPackaging InnovationCompetes by focusing on end-use solutions, rapidly developing recyclable paper-based and mono-material plastic structures, including compostable papers, to help brand owners meet their sustainability commitments.Amcor LimitedDrop-in SubstitutionUtilizes its massive global packaging footprint to promote the easy substitution of conventional plastics with materials like bio-PE, offering customers a simple, low-risk route to reducing their carbon footprint without changing established recycling practices.NatureWorks LLCPLA Specialization & InfrastructureFocuses almost entirely on Ingeo™ PLA, competing by driving improvements in mechanical and thermal properties and actively working with recyclers (using NIR sorting) to build a viable end-of-life infrastructure for its material.DuPont de Nemours, Inc.Specialty & Regulatory ComplianceServes as a key enabler in highly regulated industries, leveraging its expertise in high-performance polymers and additives to help customers in sectors like medical and pharmaceutical packaging integrate advanced, compliant, and durable bio-based solutions.

Deep Dive: Major Player Profiles

BASF SE

BASF, a global chemical powerhouse, positions itself as a leader in creating certified compostable biopolymers, notably ecoflex® (PBAT) and its compound ecovio® (PBAT/PLA).17 The company competes by providing highly researched and rigorously tested biodegradable materials that actively contribute to the circular economy by enabling the collection and organic recycling of food waste, which prevents microplastic accumulation.18 They actively partner with customers to conduct life cycle assessments, ensuring that the use of their biopolymers yields genuine ecological benefits.

Novamont S.p.A.

An Italian-based global leader in biodegradable and compostable bioplastics, Novamont is fundamentally committed to the circular bioeconomy.19 Their core product is the Mater-Bi® family of bioplastics, which utilizes renewable, plant-based sources.20 Novamont’s competitive edge lies in its unique “Living Chemistry” model, which involves converting decommissioned industrial sites into bio-refineries.21 This approach creates integrated agricultural supply chains and guarantees that its bioplastics biodegrade effectively in diverse environments, including industrial compost, soil, and water.

Arkema S.A.

Arkema focuses on high-performance materials, particularly specialty polyamides.22 Their most significant offering in the bio-based space is Rilsan® polyamide 11 (PA11), which is derived 100% from sustainably sourced castor oil.23 Unlike compostable bioplastics, Arkema’s materials are designed for extreme durability, mechanical strength, and thermal resistance, targeting demanding sectors like automotive and 3D printing. They integrate this material into a circular model through their Virtucycle® program, which facilitates the recycling of their high-performance polymers.24

Versalis S.p.A.

The chemical company of the Italian energy group Eni, Versalis has significantly amplified its position in the biopolymers market through its control of Novamont. While Versalis produces a broad array of traditional polymers, their biopolymer strategy focuses on enriching their product portfolio with Novamont’s advanced biodegradable and compostable solutions, such as Mater-Bi.25 This integration allows Versalis to directly address the sustainability requirements of the food packaging sector while simultaneously pushing for mechanical recycling innovations through initiatives like the REFENCE® recycled polymer range.26

Mondi Group

Mondi is a leading global packaging and paper group that actively facilitates the market shift toward sustainable packaging.27 They compete not as a pure chemical manufacturer but as a solutions provider, developing cutting-edge end-products. Their offerings include compostable paper packaging under the re/grow Sustainex® range and innovative mono-material plastic structures that simplify recycling.28 Mondi’s strategy is to enable brand owners to move away from multi-material, difficult-to-recycle packaging structures.29

Amcor Limited

As one of the world’s largest packaging companies, Amcor competes by deploying a global strategy centered on high-volume, low-risk sustainability solutions. They actively promote the use of bio-based materials, such as bio-PE, which serves as a “drop-in” alternative.30 Bio-PE maintains the exact performance characteristics and recyclability of fossil-based PE but significantly lowers the packaging’s carbon footprint by utilizing renewable feedstock.31 Amcor’s scale and commitment to making all packaging recyclable or reusable by 2025 make them a powerful driver of bio-based material adoption.

NatureWorks LLC

NatureWorks is a focused specialist, globally known for its proprietary biopolymer Ingeo™ (PLA), derived from fermented plant sugars.32 They compete by offering a low-carbon, renewable-source alternative to petrochemical plastics and actively solving the infrastructure challenge. NatureWorks collaborates with recyclers to ensure Ingeo is detectable and separable in the recycling stream via Near-Infrared (NIR) sorting technology. Their continuous product innovation, such as the Ingeo™ Extend platform, aims to improve material performance and accelerate compostability for specialized applications.33

DuPont de Nemours, Inc.

DuPont, a materials science and specialty products company, supports the biopolymers movement primarily by enabling high-end, demanding applications.34 They leverage their vast expertise in high-performance polymers, resins, and sealants to develop advanced solutions for sectors like healthcare and medical devices. DuPont ensures biopolymers and related materials meet the stringent regulatory compliance and extreme performance requirements (e.g., sterilization, barrier protection) needed in these critical end-use applications, often playing a role in the “Regulatory Compliance” stage of the value chain.

Frequently Asked Questions

What factors are driving the exceptional growth rate predicted for the European biopolymers market

The growth is primarily driven by three converging forces. First, stringent European Union environmental policies enforce immediate changes in packaging and manufacturing practices. Second, sustained technological breakthroughs ensure biopolymers achieve mechanical and thermal performance parity with conventional plastics.35 Third, and perhaps most powerful, is the soaring consumer preference for eco-friendly and visibly sustainable products, compelling brands to adopt bio-based alternatives.

What is the defining characteristic of the European biopolymers market composition in 2025

In 2025, the market structure is defined by the high adoption of bio-based polyethylene (bio-PE) and its dominant end-use in the packaging sector, specifically for bottles. This dominance suggests manufacturers initially prioritize bio-based materials that offer a straightforward “drop-in” replacement, allowing them to lower carbon footprints without extensively altering existing production lines or recycling infrastructures.

How is the biopolymers value chain evolving beyond raw material production

The value chain is evolving to prioritize integration and end-of-life solutions. Material producers increasingly focus on innovations like microbial fermentation for PHA to secure scalable, non-food-competitive feedstock.36 Simultaneously, packaging giants are focusing on incorporating these new polymers into recyclable mono-material structures or certified compostable designs, ensuring the final product actively supports circular economy mandates, whether through composting or advanced recycling.

Why are non-biodegradable bio-based plastics gaining significant market traction

The market is shifting toward durable, bio-based plastics that are not necessarily compostable but are compatible with existing mechanical recycling infrastructure. This trend aligns with the circular economy goal of keeping materials in use for as long as possible. Companies seek substitutes that maintain high performance (like bio-PE or bio-polyamides) but reduce reliance on fossil fuels, making them environmentally preferable and recyclable in established streams.

Which high-growth segments are expected to shape the market between 2026 and 2035

Moving forward, the fastest growth is predicted to occur in the bio-PET product segment and the films application segment. Furthermore, the automotive sector is projected to exhibit the fastest growth among end-use industries. This signifies a maturation of the market, where biopolymers successfully penetrate high-value, durable goods and high-volume, complex flexible packaging applications.

Immediate Delivery Available | Buy This Premium Research Report@ https://www.towardschemandmaterials.com/checkout/6079

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Email: [email protected]

Leave a Reply