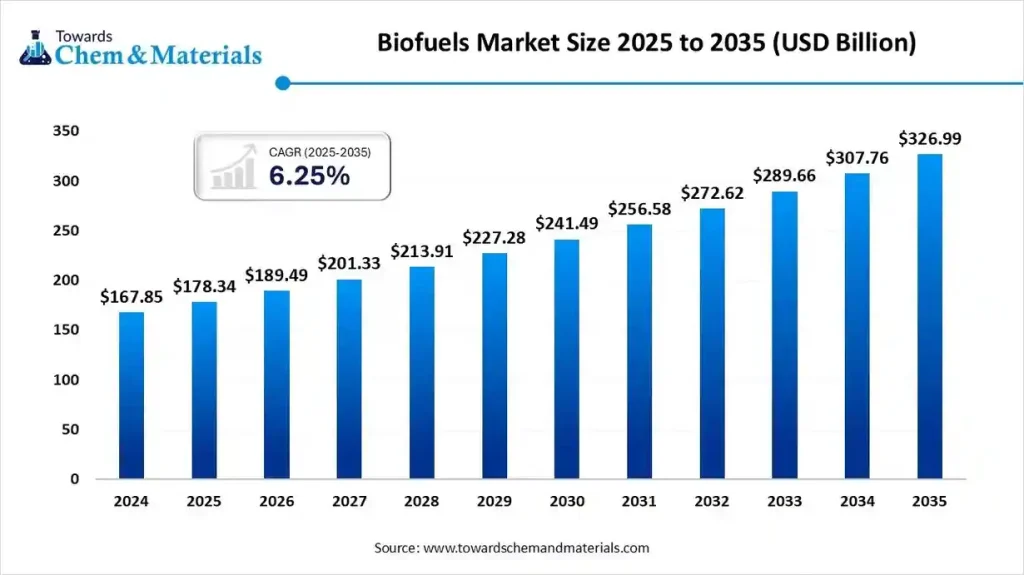

The biofuels market is entering 2025 with exceptional momentum. As climate targets tighten and energy security becomes a national priority across the world, governments and industries are doubling down on renewable liquid fuels. The global biofuels market is expected to expand from USD 178.34 billion in 2025 to USD 326.99 billion by 2035, moving at a steady 6.25% CAGR.

Get All the Details in Our Solutions — Download Sample: https://www.towardschemandmaterials.com/download-sample/6010

Bioethanol and biodiesel continue to dominate the sector, while advanced feedstock — from algae to agricultural residues — is unlocking new scalability and cost breakthroughs.

Key Takeaways for 2025

- Europe leads the world with a 43.5% market share in 2024 and enters 2025 with strong biofuel blending mandates.

- Asia Pacific accelerates fastest, growing at a 9.0% CAGR, driven by India, China, and Southeast Asia’s rapidly expanding transport sector.

- Bioethanol accounts for 47.6% of the 2024 market; it remains the most widely adopted biofuel type in 2025.

- Biodiesel grows strongly, projected to expand at 7.6% CAGR.

- Corn & sugarcane feedstock dominate with a 48.5% share, especially in the U.S., Brazil, and Southeast Asia.

- Algae-based fuels gain real traction, showing a 7.7% CAGR and emerging as the next major frontier.

- Automotive uses more than half (54.3%) of global biofuels today, while

- Aviation emerges as the fastest-growing end-use at 7.8% CAGR, fueled by Sustainable Aviation Fuel (SAF) mandates.

Biofuel Boost: Why the Market Is Growing So Fast

Biofuels benefit from a rare convergence of political will, technological progress, and global energy demand. In 2025, governments are rewriting transport fuel regulations to conform with decarbonization deadlines. The International Energy Agency estimates that global biofuel demand will jump over 11% between 2023–2025, fueled by newer clean-fuel policies across the U.S., Europe, India, and Latin America.

Air quality improvement is another major driver. Ethanol and biodiesel blends dramatically lower sulphur, particulate matter, and carbon monoxide emissions — supporting WHO-backed public health priorities.

Energy security concerns also play a critical role. As geopolitical disruptions put pressure on crude oil supply chains, more countries are shifting toward localised fuel production. Biofuels help nations reduce reliance on imported petroleum while supporting domestic agriculture and bioenergy industries.

What Are Biofuels? A 2025 Explanation

Biofuels are renewable energy sources produced from organic biomass such as corn, sugarcane, vegetable oils, forestry residues, organic waste, and algae. They can exist in liquid, gaseous, or solid form. The most common in 2025 include:

- Bioethanol — A clean-burning renewable alcohol, primarily blended with gasoline.

- Biodiesel — A renewable diesel alternative made from vegetable oils and animal fats.

- Biogas/Biomethane — Produced from waste decomposition, used for power, heating, or transport.

- Biomethanol and bio-naphtha — Emerging fuels increasingly used in marine and petrochemical sectors.

Biofuels reduce lifecycle greenhouse gases significantly compared with traditional fossil fuels, and their adoption is central to achieving global climate targets.

2025 Buyer Playbook: What Actually Decides Deals

1. Feedstock Security

Companies increasingly prioritize suppliers that ensure consistent, scalable, traceable biomass. Buyers favor producers with multi-feedstock flexibility (corn, sugarcane, waste oils, algae).

2. Compliance Readiness

Government mandates are tightening. Buyers focus on partners that meet or exceed:

- EU RED II/RED III thresholds

- U.S. Renewable Fuel Standard (RFS)

- India’s E20 ethanol targets

- Aviation SAF requirements

3. Production Cost Stability

Producers with advanced fermentation, enzymatic processing, or waste-to-fuel technologies deliver more stable pricing — crucial in volatile energy markets.

4. Carbon Intensity (CI) Scores

Top buyers choose suppliers with low CI scores, because it unlocks incentives and credits.

5. Blending Compatibility & Infrastructure

Refiners, distributors, and airlines partner with fuel makers who provide seamless integration into existing pipelines and engines.

6. Long-Term Offtake Agreements

Airlines, automakers, and logistics companies now prefer multi-year contracts to ensure predictable supply and pricing.

Quick Comparison Matrix (Explained, Not in Table Format)

- Bioethanol vs Biodiesel:

Bioethanol is more widely used in gasoline engines, while biodiesel fits diesel engines and heavy-duty vehicles. Bioethanol dominates in volume, but biodiesel leads in energy density. - Corn/Sugarcane vs Algae Feedstock:

Corn and sugarcane are proven and scalable today; algae is the future due to its extremely high yield per acre and ability to grow in non-arable areas. - Automotive vs Aviation Demand:

Automotive currently consumes the largest share, but aviation is the fastest-growing sector due to aggressive SAF mandates. - Europe vs Asia-Pacific Markets:

Europe regulates the market heavily and leads in adoption; Asia-Pacific grows fastest due to large fuel demand and expanding renewable policies.

What’s Next (2025–2030 Outlook)

1. Sustainable Aviation Fuel Becomes the Star

SAF mandates in the EU, U.S., India, and Japan will multiply market demand by 2030.

2. Algae and Waste-Based Biofuels Scale Up

Advanced feedstocks transition from pilot scale to commercial adoption.

3. Biofuel Refineries Become More Integrated

Hybrid facilities producing ethanol, biodiesel, renewable diesel, and SAF under one roof will dominate.

4. Carbon Pricing Reshapes Market Dynamics

Nations with strong carbon pricing mechanisms will see faster adoption of biofuels as fossil fuel costs rise.

5. Biofuel Exports Surge

Brazil, U.S., Indonesia, and India will become global export hubs.

6. Blending Limits Rise Worldwide

Countries will shift from E10 to E20–E27 for ethanol and B7 to B20 for biodiesel by 2030.

Why Competition in Biofuels Is Intensifying

- Global mandates are expanding, forcing rapid industry-wide procurement.

- Capital investment surges, especially into SAF, renewable diesel, and hydrogenated biofuels.

- Technological breakthroughs reduce production cost and increase conversion efficiency.

- New entrants — including oil companies — are entering the market, raising competitive pressure.

- Countries race to secure feedstock as demand outpaces agricultural supply.

Invest in Premium Global Insights — Immediate Delivery Available @

https://www.towardschemandmaterials.com/checkout/6010

How These Leading Companies Compete (In-Depth Profiles)

1. POET LLC

POET stands as one of the world’s largest bioethanol producers. The company thrives through:

- High-efficiency fermentation technologies

- Strong Midwest feedstock networks

- Deep partnerships with fuel blenders and automakers

- Heavy investment in cellulosic ethanol and carbon capture

POET competes on scale, sustainability, and agricultural integration.

2. ADM (Archer Daniels Midland)

ADM leverages its global supply chain strength to dominate both ethanol and biodiesel markets. Its key competitive advantages include:

- A massive, vertically integrated grain supply ecosystem

- Continuous R&D in enzyme technologies

- Large export capabilities

- Fast adoption of advanced biofuel refining

ADM competes on global infrastructure, reliability, and innovation.

3. Neste

Neste leads the world in renewable diesel and sustainable aviation fuel. The company is recognized for:

- Its world-leading hydrogenated vegetable oil (HVO) technology

- Strong partnerships with airlines

- Multicontinent refineries

- An aggressive expansion strategy into Europe, Singapore, and the U.S.

Neste competes on premium quality fuels, low carbon intensity, and SAF leadership.

4. BP (bp Biofuels)

BP is expanding aggressively into renewable fuels through investments in bioethanol, biogas, and renewable diesel. The company’s strategy includes:

- Converting aging refineries into bioenergy hubs

- Joint ventures in Brazil for sugarcane ethanol

- Expanding its SAF portfolio

- Integrating biofuels into bp’s EV & hydrogen ecosystem

BP competes on energy diversification and large-scale infrastructure transformation.

5. Renewable Energy Group (a Chevron company)

REG (now part of Chevron) focuses heavily on biodiesel and renewable diesel. Its strengths include:

- Flexible feedstock technology (including waste oils)

- Strong domestic U.S. market coverage

- Increasing investment in renewable diesel refining

- Carbon-intensity optimization technologies

REG competes on feedstock flexibility, low-carbon intensity, and refinery innovation.

6. Green Plains Inc.

Green Plains has transformed from a traditional ethanol producer into a biorefinery technology company, leveraging:

- High-protein feed co-products

- Advanced fermentation systems

- Technology partnerships for next-gen biofuels

Green Plains competes on biorefinery diversification and technology-driven efficiency.

7. Verbio

Verbio is a European giant known for renewable biomethane, biodiesel, and bioethanol. Its edge comes from:

- Strong waste-to-energy solutions

- High efficiency in biogas production

- Growing operations in the U.S.

Verbio competes on sustainability, waste utilization, and renewable gas expertise.

8. Wilmar International

Wilmar leverages Asia’s largest agricultural network to lead biodiesel production. It benefits from:

- Extensive palm oil supply chains

- Large refinery capacity

- Export presence in Europe and China

Wilmar competes on feedstock dominance and Asian market scale.

For more information, visit the Towards Chemical and Materials website or email the team at [email protected]| +1 804 441 9344

More Insights in Towards Chemical and Materials:

- U.S. Biofuels Market: The U.S. Biofuels market is projected to grow from USD 36.76 billion in 2025 to USD 109.65 billion by 2035, growing at a compound annual growth rate (CAGR) of 11.55% over the forecast period from 2025 to 2035.

- Biohydrogen Market : The global biohydrogen market is projected to grow from USD 76.78 million in 2025 to USD 157.80 million by 2035, growing at a compound annual growth rate (CAGR) of 7.47% over the forecast period from 2025 to 2035.

- Bio-Renewable Chemicals Market : The global bio-renewable chemicals market size was valued at USD 15.11 billion in 2024 and is growing to approximately USD 39.01 billion by 2034, with a developing compound annual growth rate (CAGR) of 9.95% over the forecast period 2025 to 2034.

- Biofertilizer Market : The global biofertilizer market is projected to grow from USD 3.31 billion in 2025 to USD 11.08 billion by 2035, growing at a compound annual growth rate (CAGR) of 12.85% over the forecast period from 2025 to 2035.

- Bio-Based Polypropylene Market : The global bio-based polypropylene market size is calculated at USD 357.67 million in 2025 and is expected to reach USD 6,977.54 million by 2034, growing at a CAGR of 39.11% from 2025 to 2034.

Conclusion: The Biofuels Industry Enters Its Most Transformative Decade

As governments enforce stricter carbon reduction laws, and industries compete for cleaner fuels, the biofuels market is set for major expansion. From automotive to aviation, biofuels are becoming a central pillar of global decarbonization strategies.

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Email: [email protected]

Leave a Reply