Executive Summary

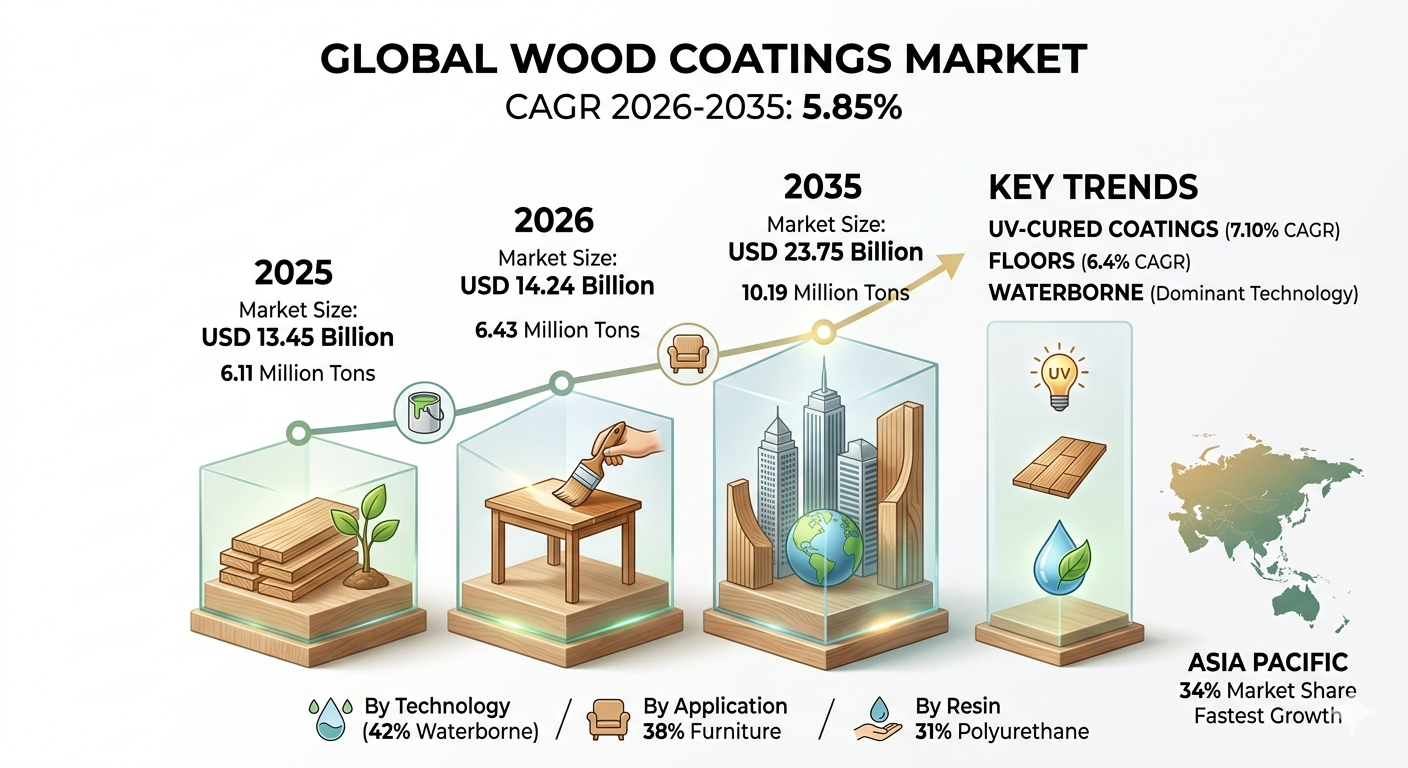

The global wood coatings market is experiencing a significant phase of structural evolution. Valued at USD 13.45 billion in 2025, the market is estimated to reach USD 14.24 billion in 2026 and is projected to expand to USD 23.75 billion by 2035. This long-term growth trajectory represents a stable compound annual growth rate (CAGR) of 5.85% during the forecast window from 2026 to 2035.

In terms of product volume, the market is anticipated to scale from 6.11 million tons in 2025 to 10.19 million tons by 2035, exhibiting a parallel volume CAGR of 5.25%. The foundational momentum of this industry is primarily anchored by rapid urbanization, strong residential real estate expansions, and a decisive, regulatory-driven shift toward ultra-low emission formulation technologies across major economic zones.

Market Overview

Why Is the Wood Coatings Market Important?

Wood is an inherently porous organic material susceptible to moisture infiltration, UV degradation, thermal expansion, and microbiological threats such as fungal rot. High-quality wood coatings—ranging from specialized lacquers and varnishes to heavy-duty polyurethanes—serve as essential protective barriers that prevent structural warping, physical decay, and cosmetic scratching.

Beyond maintaining physical integrity, these finishes enhance the natural aesthetics and grain definition of the timber, thereby directly driving value creation within the global premium furniture, custom cabinetry, and high-end flooring markets. Furthermore, modern architectural trends rely heavily on industrial wood coatings to extend the life cycles of exterior decking and joinery exposed to harsh weather conditions.

What Is the Core Structure of the Wood Coatings Market?

The structural framework of the wood coatings industry is highly dependent on downstream architectural and manufacturing activities. The market relies on the formulation of advanced resins, solvents, additives, and curing systems to satisfy specific end-use demands.

Residential applications continue to form the baseline of volume consumption, while the industrial processing sector dictates performance standards by implementing rapid-curing, inline finishing processes. Geographically, the market acts as an economic bridge connecting raw chemical material supply chains with major global furniture manufacturing hubs and local residential renovation sectors.

Market Dynamics

What Are the Key Factors Driving the Market?

-

Accelerated Urbanization and Real Estate Growth: Rapid population shifts into urban centers within emerging economies continue to trigger massive public and private construction projects, naturally multiplying the installation of wooden fixtures, doors, windows, and floors.

-

Furniture Production Scaling Globally: The steady expansion of both residential furniture consumption and international ready-to-assemble (RTA) furniture exports provides a continuous demand loop for high-volume industrial wood finishes.

-

Rapid Adoption of Curing Innovations: Industrial manufacturers are increasingly integrating Ultraviolet (UV) and electron beam (EB) curing lines into their operations. These systems provide near-instant drying capabilities, maximizing production throughput and reducing warehouse floor footprint.

What Are the Primary Restraints Limiting Wood Coatings Adoption?

-

Stringent Environmental Emission Mandates: Environmental Protection Agencies worldwide are strictly enforcing low volatile organic compound (VOC) limits. This ongoing regulatory pressure forces manufacturers to incur heavy formulation and raw material R&D costs to phase out traditional, high-performing solvent-borne baselines.

-

Raw Material Cost Volatility: Unpredictable price spikes in core resins, chemical additives, and pigments put significant pressure on processing margins, occasionally forcing manufacturers to pass costs onto consumer-facing furniture segments.

What Is the Impact of Key Market Trends?

The definitive trend steering the modern industry is the aggressive transition from traditional solvent-based chemistries toward waterborne, powder, and bio-derived hybrid alternatives. Concurrently, consumer preferences are shifting away from generic paints toward high-clarity finishing materials that preserve and showcase natural wood grains. This visual demand has led to a major rise in specialized matte, ultra-glossy, and scratch-resistant smart finishes.

Market Segments & Insights

Which Segment Accounted for the Largest Market Share?

The Waterborne Coatings segment and the Residential segment dominated their respective areas, capturing 42% and 46% of the global revenue shares in 2025. The dominance of waterborne technologies is a direct result of strict global environmental regulations that push industrial and DIY users away from high-VOC alternatives. Meanwhile, the residential segment’s top position highlights the massive scale of housing construction and home renovation investments globally.

Summary Data Table: 2025 Market Share Breakdown

| Segment Category | Sub-Segment Name | 2025 Revenue Share (%) | Key Drivers & Performance Attributes |

| Resin Type | Polyurethane (PU) | 31% | Superior abrasion resistance, scratch prevention, and high-end durability. |

| Resin Type | Acrylic | 24% | Excellent non-yellowing traits; projected to expand at a 6.30% CAGR. |

| Technology | Waterborne | 42% | Low VOC profile, reduced odor, and excellent eco-friendly regulatory alignment. |

| Technology | UV-Cured | 16% | Instant curing time; anticipated to grow at the fastest CAGR of 7.10%. |

| Application | Furniture | 38% | High volume demand from global residential and commercial furniture makers. |

| Application | Flooring | 16% | Driven by hardwood floor trends; expanding at a 6.4% CAGR. |

| End-Use | Residential | 46% | Driven by home renovations, new housing projects, and DIY interior upgrades. |

| End-Use | Institutional | 9% | Growth focused on heavy-duty public infrastructure wood installations. |

| Geographic Region | Asia Pacific | 34% | Dominant global position fueled by urbanization and regional manufacturing hubs. |

What Is the Segment Growth Outlook?

The UV-Cured Coatings segment is projected to grow at the fastest tech-based CAGR of 7.10% through 2035. This rapid adoption is driven by automated industrial finishing lines that rely on instant cross-linking to skip traditional thermal drying steps.

From an application perspective, the wood flooring segment is positioned for the fastest expansion at a 6.4% CAGR. This trend is propelled by growing global consumer investments in premium hardwood remodeling, luxury real estate projects, and weather-resistant outdoor decking.

Regional Insights

How Did Asia Pacific Dominate the Wood Coatings Market?

The Asia Pacific region held the leading position in the global market, accounting for a dominant 34% revenue share in 2025, and is projected to expand at the fastest CAGR of 7.20% over the forecast window. Valued at USD 4.57 billion regionally in 2025 and on track to reach USD 8.19 billion by 2035, the region’s top spot is supported by immense furniture manufacturing corridors in China and Vietnam. These hubs process and finish massive volumes of consumer goods for global retail export. Concurrently, booming construction and real estate sectors in India and Indonesia continue to absorb immense volumes of decorative architectural finishes.

Western and Latin American Regional Dynamics

Europe held a solid 27% market share in 2025, with its growth path strictly tied to ECHA, REACH, and EU Green Deal directives that mandate low chemical emissions. This regulatory focus has turned Germany, Italy, and France into premium hubs for bio-based and waterborne wood coating innovations.

North America accounted for 24% of global revenue in 2025, driven by strong residential remodeling cycles in the United States and massive timber construction corridors in Canada. Latin America (8% share) and the Middle East & Africa (7% share) are maintaining positive growth tracks, powered respectively by Brazil’s large-scale furniture manufacturing corridors and the UAE and Saudi Arabia’s massive luxury real estate developments.

Benefits of Using Advanced Wood Coatings

-

Extreme Mechanical and Abrasion Resistance: Polyurethane and hybrid resin coatings create tough surface barriers that easily absorb heavy impacts and resist scratching in high-traffic environments.

-

Long-Term Weather and UV Protection: Premium exterior formulations shield wood substrates from intense solar radiation and moisture, preventing color fading, surface cracking, and internal rot.

-

Drastic Improvements in Factory Productivity: Modern UV-curable coatings dry almost instantly when exposed to ultraviolet light. This allows production lines to run continuously, speeding up packaging and shipping times.

-

Healthy Indoor Air Quality Compliance: Advanced waterborne options emit minimal VOCs. This ensures industrial plants and residential interiors easily comply with strict modern green building certifications.

Competitive Landscape

Top Companies in the Wood Coatings Market

The Sherwin-Williams Company (US)

-

About: A global leader in the development, manufacture, and sale of paints and high-performance industrial coatings.

-

Products: Extensive professional wood stains, protective lacquers, varnishes, and low-VOC waterborne finishes.

-

Market Capitalization: Valued at approximately USD 75.30 billion as of June 2026.

PPG Industries, Inc. (US)

-

About: A major multinational manufacturer supplying specialty paints, industrial coatings, and advanced chemical materials globally.

-

Products: High-durability polyurethane wood finishes, quick-cure industrial coatings, and eco-friendly architectural wood stains.

-

Market Capitalization: Valued at approximately USD 28.50 billion as of mid-2026.

Akzo Nobel N.V. (NL)

-

About: A specialized global paints and performance coatings company focusing on sustainable finishes and innovative chemical formulations.

-

Products: Sikkens wood finishes, RUBBOL bio-based waterborne coatings, and specialized wood laminating resins.

-

Market Capitalization: Valued at approximately USD 13.10 billion as of June 2026.

Nippon Paint Holdings Co., Ltd. (JP)

-

About: The dominant paint and chemical coatings manufacturer across the Asia-Pacific region, continuously expanding its global footprint.

-

Products: Hydro-wood waterborne coating systems, low-emission furniture varnishes, and automated viscosity-controlled industrial finishes.

-

Market Capitalization: Valued at approximately USD 14.06 billion as of June 2026.

RPM International Inc. (US)

-

About: A multinational holding company that owns specialized chemical formulation brands serving both industrial and DIY consumers.

-

Products: Rust-Oleum decorative wood stains, Varathane finishes, and FinishWorks specialized industrial coatings.

-

Market Capitalization: Valued at approximately USD 13.40 billion as of June 2026.

What Is the Status of Recent Strategic Developments?

The competitive landscape highlights an active industry focus on sustainable chemical engineering and expanded industrial market offerings:

-

March 2026: Pittsburgh Paints Company expanded its commercial reach by launching the dedicated Tru-Industrial coatings brand. The new portfolio features solvent-based (TRU-SOLV MAX), waterborne (H-TRU-O MAX), and specialized shed coatings (TRU-SHED MAX) designed to bring long-lasting protection to heavy-duty industrial applications.

-

February 2025: AkzoNobel’s Sikkens Wood Coatings business launched RUBBOL WF 3350 from its facility in Malmö, Sweden. This sustainable, sprayable opaque waterborne wood finish contains 20% plant-derived bio-based content verified by C-14 testing, proving that eco-friendly formulations can deliver top-tier weather resistance.

What Is the Regulatory Landscape Governing Wood Coatings?

Global regulatory bodies enforce strict guidelines to manage chemical emissions and improve workplace safety:

-

United States: The EPA and OSHA enforce the Clean Air Act and National VOC Emission Standards. This oversight accelerates the market shift toward water-based and UV-cured formulations to minimize volatile chemical releases and protect workers.

-

European Union: Managed by the ECHA, regulations like REACH and the Industrial Emissions Directive (IED) set tight caps on industrial solvent emissions, pushing companies to adopt bio-based alternatives.

-

China: The Ministry of Ecology and Environment (MEE) applies strict VOC Emission Control Standards, requiring factories to phase out traditional solvent-borne formulas to back national industrial green initiatives.

-

India: The CPCB and Bureau of Indian Standards (BIS) manage local air quality and coating safety rules, steering the expanding furniture sector toward healthier indoor air quality formulations.

What Are the Recent Government Initiatives Supporting the Market?

Governments around the world are implementing green build mandates and tax incentives to encourage the use of low-emission surface technologies. In Western Europe, public funding under the EU Green Deal’s “Renovation Wave” favors building materials that carry certified low-VOC profiles.

In the United States, federal tax credits for energy-efficient renovations have spiked demand for durable coatings that extend the lifespan of exterior doors and windows. At the same time, strict green building compliance certificates across Asia-Pacific are encouraging commercial real estate developers to use waterborne and zero-VOC powder systems in public spaces.

What Is the Future of the Market?

The future of the wood coatings industry will be shaped by advanced bio-refining techniques and the commercialization of smart finishes. Over the next ten years, traditional oil-derived resins will increasingly be replaced by plant-based, renewable chemical alternatives to meet corporate net-zero commitments.

At the same time, nanotechnology will continue to drive innovations like self-healing clear coats that can automatically repair micro-scratches when exposed to ambient sunlight. While traditional solvent-borne formulations will still be used for highly specific, heavy-duty industrial tasks, market value and growth will increasingly cluster around automated UV-cured lines and bio-hybrid waterborne technologies. This shift will redefine wood preservation standards through 2035.

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Email: [email protected]

Leave a Reply