The global manufacturing sector is undergoing a profound paradigm shift, evolving from static, structural substrates to dynamic, intelligent systems. At the forefront of this physical metamorphosis is the Global Shape Memory Materials (SMM) Market. Characterized by alloys, polymers, and ceramics capable of “remembering” and reverting to their original macroscopic geometry upon exposure to an external thermal, magnetic, or electrical stimulus, these advanced functional materials are redefining product design metrics across critical high-reliability industries.

Executive Summary

The global shape memory materials market represents one of the fastest-growing sectors within advanced metallurgy and functional polymer chemistry. Driven by extreme miniaturization demands in minimally invasive medical procedures, adaptive aerodynamics in aerospace engineering, and solid-state actuation in consumer electronics, the market is scaling rapidly.

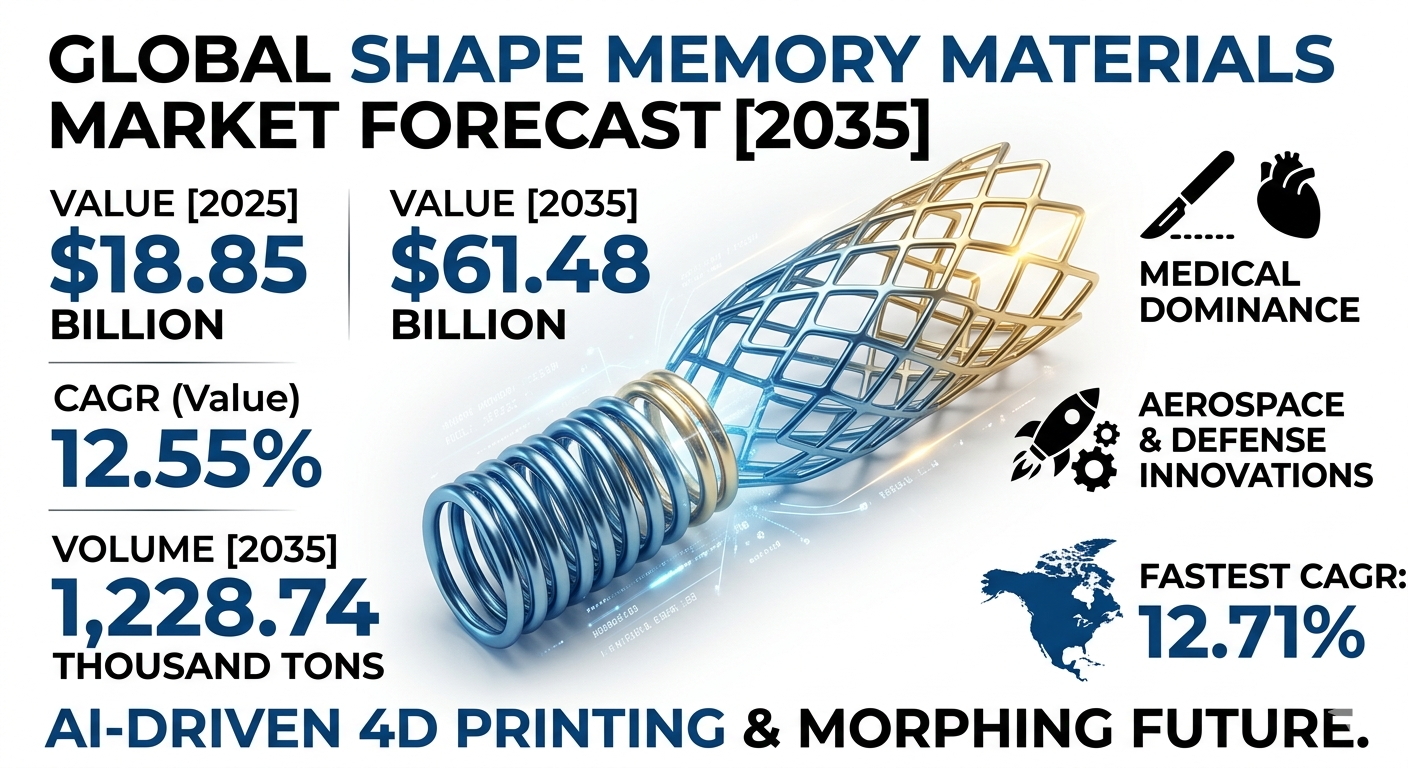

Valued at USD 18.85 billion in 2025, the global market is estimated to reach USD 21.22 billion in 2026. Projections indicate that the industry will expand to USD 61.48 billion by 2035, exhibiting a remarkable value compound annual growth rate (CAGR) of 12.55% over the 2026–2035 forecast period.

In terms of physical volume, the industry is transitioning from a high-margin, niche framework to scalable industrial production, projected to grow from 429.25 thousand tons in 2025 to 1,228.74 thousand tons by 2035, registering a volume CAGR of 11.09%. Looking at intermediate milestones, the market is positioned to surpass USD 41.5 billion by 2032, sustained by structural supply-chain optimization and expanded commercialization of shape memory polymers (SMPs).

Comprehensive Market Overview

What is the Shape Memory Materials Market?

The shape memory materials market encompasses the research, synthesis, processing, and commercial distribution of smart material classes exhibiting the Shape Memory Effect (SME) and pseudoelasticity (superelasticity). Unlike conventional engineering materials that undergo permanent plastic deformation under stress or thermal cycling, SMMs leverage reversible solid-state phase transformations.

The most dominant class is the Shape Memory Alloy (SMA), specifically Nickel-Titanium (commonly known as Nitinol), alongside emerging alternatives such as copper-based and iron-based alloys, and Shape Memory Polymers (SMPs). These materials are utilized as responsive components—such as micro-actuators, self-expanding vascular stents, adaptive structural components, and self-healing mechanisms—bridging the gap between sensor input and mechanical output without the need for complex, heavy mechanical assemblies.

Why is the Market Gaining Strategic Importance?

The strategic capitalization of shape memory materials is accelerating due to a confluence of multi-industry demands for:

-

Weight reduction

-

Mechanical simplification

-

Biocompatible device design

In modern infrastructure, aerospace systems, and premium medical therapies, traditional multi-part mechanical actuators (relying on motors, gears, and hydraulic lines) introduce significant failure points, frictional wear, and parasitic weight. SMMs function essentially as solid-state, monolithic mechanisms; the material itself is the actuator. This intrinsic capability allows engineers to eliminate complex sub-assemblies, minimize component profiles, lower energy consumption, and increase overall system reliability.

Market Dynamics & Analytical Insights

Below is a systematic structural breakdown of the global shape memory materials landscape, formatted to address core technical questions asked by procurement, R&D, and financial strategy teams.

What are the Key Factors Driving the Market?

-

Surge in Minimally Invasive Surgeries (MIS): The medical sector remains the foundational anchor for SMM demand. Nitinol’s unique superelasticity and biocompatibility have made it irreplaceable for endovascular guidewires, self-expanding transcatheter heart valves, and neurovascular stents. The material undergoes massive elastic deformation during catheter delivery and flawlessly recovers its expanded functional geometry at body temperature ($A_f \le 37^\circ\text{C}$).

-

Aerospace and Defense Structural Modernization: Next-generation military aircraft, commercial aviation fleets, and satellite systems increasingly integrate SMAs to achieve morphing wing profiles, variable geometry chevrons for noise reduction, and low-shock release mechanisms for space launch fairings.

-

Rapid Consumer Electronics Integration: High-end smartphone camera modules are deploying Nitinol-driven Shape Memory Alloy actuators for Optical Image Stabilization (OIS) and autofocus mechanisms, replacing heavy, fragile voice-coil motors (VCMs) with microscopic, silent wire actuators.

What are the Key Market Trends?

-

Shift Toward Additive Manufacturing (3D Printing): Laser Powder Bed Fusion (LPBF) and Electron Beam Melting (EBM) of Nitinol are transitioning from academic labs to industrial lines. 3D printing enables the fabrication of customized porous orthopedic implants and complex topological lattices that possess specific biomechanical properties matching human cortical bone.

-

Development of High-Temperature Shape Memory Alloys (HTSMAs): Conventional Nitinol operates reliably only below $100^\circ\text{C}$. Intense R&D is focused on ternary systems like Ni-Ti-Hf (Hafnium), Ni-Ti-Zr (Zirconium), and Ni-Ti-Pd (Palladium) to push transformation temperatures beyond $200^\circ\text{C}$ to $400^\circ\text{C}$, opening up downhole oilfield drilling and gas-turbine engine bypass environments.

What are the Restraints Challenging Market Growth?

Despite stellar demand trajectories, high extraction and processing complexities act as structural barriers. Melting and processing Nitinol requires strict atmospheric control (vacuum induction melting or vacuum arc remelting) to prevent oxygen and carbon contamination, which severely degrades fatigue life and alters precisely calibrated transformation temperatures. Furthermore, machining, grinding, and laser welding these hyper-elastic materials requires highly specialized capital equipment, keeping raw material costs high compared to standard titanium or stainless-steel alloys.

Market Recent Government Initiatives

Regulatory frameworks and direct sovereign funding are actively standardizing and accelerating smart material ecosystems worldwide.

-

United States CHIPS and Science Act & DoD Initiatives: The U.S. Department of Defense, via its manufacturing innovation institutes, has funneled dedicated grant allocations toward scaling domestic processing of advanced functional materials. These initiatives focus heavily on securing supply chains for strategic metallurgical products like Nitinol and high-temperature alloys used in defense aerospace, reducing reliance on foreign refining assets.

-

European Union Green Deal & Horizon Europe: Under Horizon Europe’s advanced materials mandate, the EU has funded collaborative consortiums investigating lightweight, bio-based Shape Memory Polymers (SMPs). These programs prioritize the development of recyclable smart plastics designed for automotive active aerodynamics, aiming to improve vehicular energy efficiency and reduce life-cycle carbon footprints.

-

India’s “Make in India” & Defense Indigenization: In alignment with domestic self-reliance initiatives, agencies like Mishra Dhatu Nigam Limited (MIDHANI) have established localized processing capabilities for medical-grade and defense-grade Nitinol formulations, streamlining regional supply chains for medical device manufacturers in the Asia-Pacific theater.

Global Shape Memory Materials Market Share & Value Projections

| Metric / Parameter | 2025 Baseline Value | 2026 Estimated Value | 2035 Projected Value | Forecast Period CAGR (2026–2035) |

| Global Market Value (USD) | $18.85 Billion | $21.22 Billion | $61.48 Billion | 12.55% |

| Global Volume (Thousand Tons) | 429.25 | 456.72 | 1,228.74 | 11.09% |

| North America Market Share | 34.0% ($6.41B) | Leading Region | High Consolidation | 12.71% (Fastest Value Growth) |

Key Market Segments & Trends

Which Segment Accounted for the Largest Market Share?

By a significant margin, the Medical & Healthcare end-use industry and Nickel-Titanium (Nitinol) alloy types dominate global operations. Nitinol accounted for over 52% of total revenue share within the material category in 2025.

Application-wise, Vascular Stents and Minimally Invasive Surgical Tools capture the largest segment share, driven by their critical clinical role where no alternative material can duplicate the combination of elastic strain capacity up to 8% and exceptional biostability.

Regional Growth Characteristics

-

North America (34% Market Share in 2025): The undisputed global powerhouse, North America’s leadership is anchored by an advanced biomedical manufacturing corridor in the United States and massive defense-aerospace investment. The region is expected to expand at the fastest value CAGR of 12.71%, sustained by extensive clinical adoption of next-generation transcatheter devices and high-value defense procurement.

-

Europe: Heavily driven by the automotive manufacturing clusters in Germany and aerospace hubs in France, focus here leans toward active noise cancellation, smart adaptive trim, and deployment mechanisms for commercial aviation.

-

Asia-Pacific: Positioned as the fastest-growing production and high-volume consumption engine. Driven by massive industrial localization in China, Japan, and South Korea, this region is scaling rapidly in the consumer electronics and automotive sub-segments, supported by extensive raw material smelting infrastructure.

Competitive Landscape: Top Companies

The global shape memory materials landscape is highly consolidated in its high-tier metallurgical tiers due to intense capital expenditure constraints and strict certification protocols (such as ISO 13485 for medical devices). Below is a deep profile of the leading industrial actors driving the market.

1. ATI Inc. (Allegheny Technologies)

-

About the Company: Based in Dallas, Texas, ATI is a global producer of technically advanced specialty materials and components. The company operates a highly vertical metallurgical pipeline, specializing in nickel-based, titanium-based, and zirconium-based alloys designed for extreme environments.

-

Core Product Portfolio: High-purity Nitinol bars, wires, plates, and ultra-fine flat wires engineered for vascular intervention devices, orthopedic anchors, and critical high-temperature aerospace fasteners.

-

Estimated Market Capitalization: ~$7.2 Billion

2. SAES Getters S.p.A.

-

About the Company: Headquartered in Milan, Italy, SAES Getters is a pioneer in functional materials and vacuum technology. Following its strategic cash-rich sale of its U.S. Nitinol raw material business (SAES Smart Materials) to Resonetics for $900 million, SAES has re-centered its focus on advanced downstream nitinol component fabrication, micro-tethers, and specialized shape memory polymer matrices.

-

Core Product Portfolio: SmartFlex nitinol actuator wires, bespoke laser-cut components, superelastic micro-tubes, and highly advanced shape memory wires tailored for the robotics and industrial automation sectors.

-

Estimated Market Capitalization: ~$550 Million (Reflecting post-divestiture restructuring)

3. Furukawa Electric Co., Ltd.

-

About the Company: Operating from Tokyo, Japan, Furukawa Electric is a global industrial conglomerate spanning telecommunications, electronics, and advanced metals. Furukawa was one of the historical pioneers in commercializing Nitinol processing techniques outside of North America.

-

Core Product Portfolio: NT-Alloy series (proprietary Nitinol formulations), superelastic engine component components, highly uniform orthodontic archwires, and micro-actuators for commercial optical arrays.

-

Estimated Market Capitalization: ~$2.1 Billion

4. Fort Wayne Metals

-

About the Company: A privately-held specialist manufacturer based in Fort Wayne, Indiana, this company is universally recognized as a foundational standard-setter for fine precision wire drawing used in the medical device sector.

-

Core Product Portfolio: DPS (Drawn Powder Stent) tubing, Nitinol wire variants with precisely tailored plateaus, DFT (Drawn Filled Tube) composite wire combining a Nitinol shell with a highly radiopaque platinum or gold core for high visibility under X-ray fluoroscopy.

-

Estimated Financial Profile: Privately held; estimated annual institutional revenues exceed $450 Million.

Recent Strategic Developments by Major Companies

The structural dynamics of the SMM market are continuously re-shaped by targeted consolidation and asset optimization.

-

Strategic Acquisition of SAES Smart Materials by Resonetics: In a definitive moves altering the raw material pipeline, Resonetics finalized the acquisition of SAES Getters’ raw material smelting and processing business. This structural realignment gives Resonetics complete end-to-end control from vacuum melting to ultra-precise laser cutting, expanding its capacity to serve global medical technology OEMs.

-

Fort Wayne Metals’ Manufacturing Footprint Expansion: To alleviate structural supply backlogs for superelastic wire, Fort Wayne Metals executed multi-million dollar capital expansion programs at its Indiana processing complex. The expansion installs next-generation proprietary continuous drawing furnaces to meet soaring global demand for neurovascular access wires.

-

ATI’s Operational Focus on Aerospace-Grade Alloys: ATI has intentionally shifted its processing lines to capitalize on high-margin commercial aviation production backlogs, increasing capital allocations for large-scale production of high-temperature titanium and nickel-based SMAs utilized in modern narrow-body and wide-body fuel-efficient turbine assemblies.

Future Horizon & Analyst Conclusion

The global shape memory materials market is transitioning from an era of exploratory engineering into an era of deep structural integration. As manufacturing networks successfully navigate the historical constraints of processing costs and atmospheric melting control, SMMs are poised to replace traditional mechanical assemblies at an accelerating rate.

The integration of artificial intelligence and machine learning into computational materials science will further shorten development timelines. AI-driven generative design models are already being deployed to map complex ternary and quaternary phase transformation curves, allowing metallurgists to accurately predict the mechanical fatigue life of novel compositions before striking a single arc in a vacuum furnace.

Over the next decade, the convergence of additive manufacturing and advanced shape memory chemistry will unlock true “4D printing”—the production of three-dimensional physical structures capable of predictable, programmed autonomous morphing over time. For industrial actors, supply chain executives, and design engineers, securing strategic access to SMM sourcing and engineering expertise is no longer merely an innovative research pathway; it is a critical requirement for maintaining competitive product performance across the global industrial landscape.

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Email: [email protected]

Leave a Reply