Executive Summary

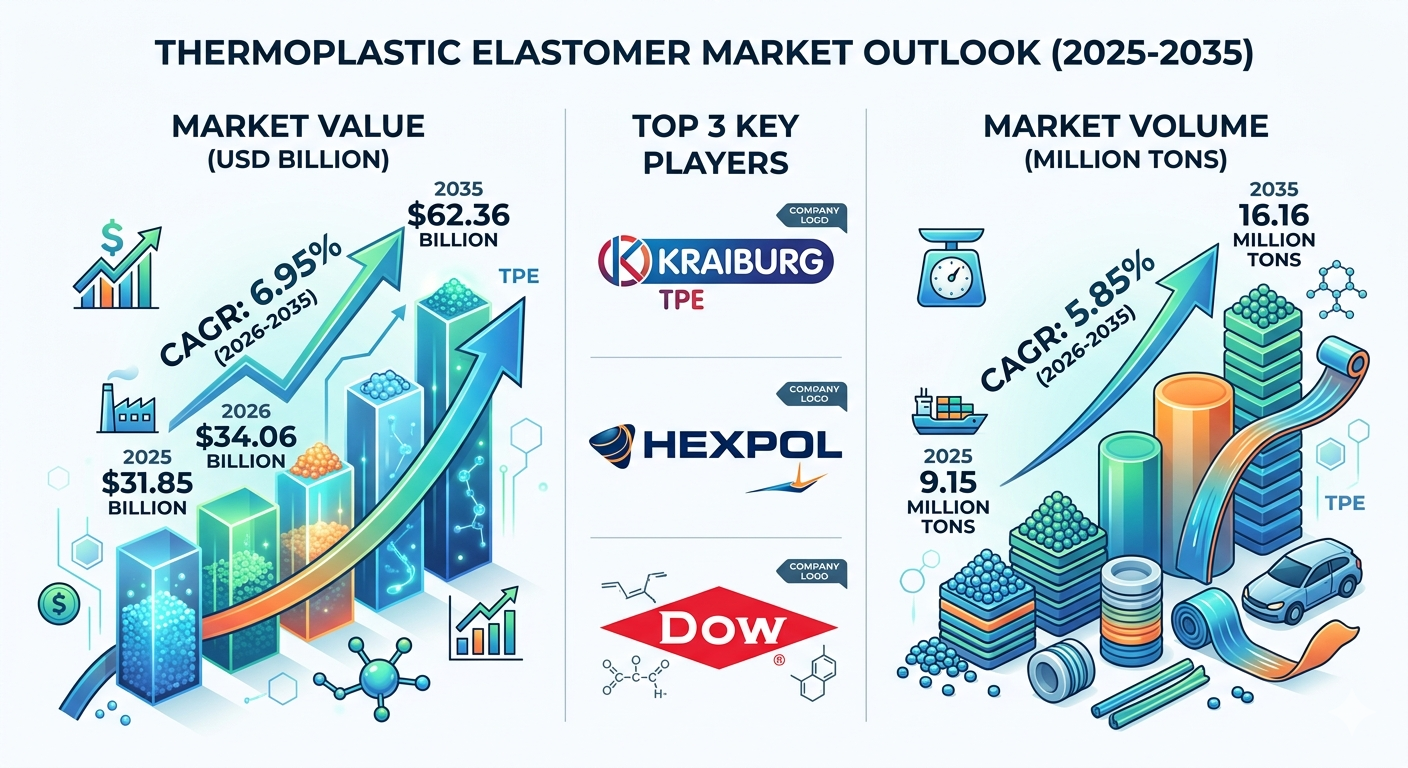

The global Thermoplastic Elastomer (TPE) market is undergoing a structural transition driven by lightweighting mandates in automotive engineering, rapid industrialization, and a secular shift toward advanced flexible polymer formulations. The global thermoplastic elastomer market size was valued at USD 31.85 billion in 2025 and is estimated to reach USD 34.06 billion in 2026. Propelled by high-performance demand across the automotive, medical, and packaging landscapes, the market is projected to reach USD 62.36 billion by 2035. This trajectory exhibits a compound annual growth rate (CAGR) of 6.95% over the forecast period from 2026 to 2035.

In terms of volumetric consumption, the industry is projected to scale from 9.15 million tons in 2025 to 16.16 million tons by 2035, expanding at a CAGR of 5.85%. This research piece evaluates core macro dynamics, legislative frameworks, processing innovations, and the granular financial footprints of the industrial entities steering this market.

Market Overview

What is the structural configuration of the Thermoplastic Elastomer Market?

Thermoplastic Elastomers represent a highly versatile class of copolymers or physical blends of polymers that blend the functional performance characteristics of vulcanized rubber with the processing efficiencies and recyclability of conventional thermoplastics. Unlike thermoset rubbers, which require chemically permanent cross-linking (vulcanization), TPEs rely on physical cross-linking networks that dissociate under thermal stress. This allows them to be repeatedly melted, reshaped, and recycled without significant material degradation.

The structural landscape is defined by its diverse processing compatibility, primarily dominating injection molding applications, while rapidly expanding into additive manufacturing pathways like 3D printing. The materials provide structural design flexibility, extensive hardness configurations (ranging from ultra-soft grades to rigid variations), and excellent chemical, thermal, and abrasion resistance. These inherent performance benefits position TPEs as the standard alternative to traditional latex, silicone, and PVC configurations across critical industrial sectors.

What are the key factors driving the market?

-

Aggressive Automotive Lightweighting and Decarbonization: Global automakers are actively re-engineering structural and interior components to curb vehicle weight, directly improving internal combustion engine (ICE) efficiency and extending electric vehicle (EV) battery ranges. TPEs are displacing dense thermoset rubbers in weatherstripping, interior panels, and under-the-hood seals due to their favorable strength-to-weight ratios and high chemical stability.

-

Biocompatible Material Shift in Medical Manufacturing: Healthcare OEMs are rapidly transitioning away from natural rubber latex and flexible PVC due to allergenicity concerns and regulatory crackdowns on specific phthalate plasticizers. TPE formulations offer pristine, latex-free compliance, excellent sterilization stability, and highly predictable elastomeric recovery, making them ideal for modern medical tubes, syringe tips, and wearable devices.

-

Superior Processing Efficiencies over Thermosets: Because TPEs eliminate the energy-intensive, time-consuming vulcanization cycle, processing steps are significantly shortened. The capacity to run short cycle times using high-throughput injection molding lowers per-unit manufacturing costs, cuts energy consumption, and reduces scrap rates through immediate re-granulation.

What are the primary market constraints?

-

Elevated Raw Material Input Costs: The production of advanced engineering TPE subclasses—such as thermoplastic polyurethanes (TPUs) and thermoplastic vulcanizates (TPVs)—depends heavily on complex, raw chemical precursors derived from petrochemical loops. High price volatility in base monomers can squeeze processing margins for tier-1 convertors.

-

Thermal Performance Limitations: While TPEs excel across broad thermal envelopes, their physical cross-linking mechanism makes them inherently susceptible to structural softening and mechanical creep at sustained, high-temperature thresholds. This performance gap can limit their use in extreme, heavy-duty industrial environments compared to true thermoset networks.

Market Insights & Benefits

Why is the Thermoplastic Elastomer Market important?

The strategic importance of the TPE market rests on its role as an industrial bridge between design flexibility and circular economy goals. As regulatory bodies tighten extended producer responsibility (EPR) laws, components must be designed from the start with end-of-life recycling in mind. TPEs fulfill this requirement by being easily re-meltable, allowing multi-material assemblies to be processed efficiently. Furthermore, their multi-functional performance profiles allow single TPE formulations to replace complex multi-component rubber-and-plastic setups, simplifying supply chains and lowering systemic failure rates in field operations.

What are the primary benefits of utilizing TPEs?

-

Design Freedom and Multi-Component Overmolding: TPEs adhere exceptionally well to rigid thermoplastic substrates via co-injection or overmolding. This enables the high-speed production of soft-touch ergonomic grips, structural dampeners, and integrated sealing gaskets without the need for manual adhesives or mechanical fasteners.

-

Broad Tailorable Hardness Ranges: Formulators can adjust durometer values anywhere from ultra-soft gel options (Shore OO scale) up to highly rigid, impact-resistant structures (Shore D scale), meeting precise industrial specifications.

-

Inherent Chemical and Environmental Resilience: Advanced grades provide excellent barrier resistance against ozone degradation, UV exposure, aggressive hydraulic fluids, and oxidative environments, preserving component longevity.

Market Recent Government Initiatives

How are international regulations steering market expansion?

-

EU End-of-Life Vehicles (ELV) Directive: Stringent European mandates requiring high recyclability metrics per vehicle are driving European markets (holding a 26% share in 2025) to replace thermoset rubbers with fully circular TPE options, generating a stable 6.40% regional CAGR.

-

FDA and European Pharmacopoeia Phthalate Restrictions: Global health authorities have restricted specific low-molecular-weight phthalate plasticizers historically used to soften medical PVC. This regulatory shift accelerates the 8.9% CAGR seen in the medical segment as manufacturers turn to inherently flexible, pure TPE alternatives.

-

Corporate Average Fuel Economy (CAFE) Standards: Continually rising fuel efficiency targets globally force automotive supply chains to replace heavy under-hood components with lightweight high-performance engineering elastomers (TPVs and TPUs), sustaining the automotive segment’s 33% dominant market share.

Competitive Landscape: Top Companies Profiled

BASF SE

-

About: Headquartered in Ludwigshafen, Germany, BASF SE is a global chemical manufacturing giant operating across intensive functional materials and materials technologies segments.

-

Products: Key TPE products include the Elastollan® Thermoplastic Polyurethane (TPU) series, widely recognized for excellent abrasion resistance, structural elasticity, and chemical durability across automotive and cable jacket applications.

-

Market Capitalization: Approximately EUR 47.3 billion (~USD 53.4 billion) as of May 2026.

Covestro AG

-

About: Spun out originally from Bayer, Covestro AG is a premier global producer of high-performance polymer materials, specializing in polyurethane and polycarbonate solutions.

-

Products: Markets the highly adaptable Desmopan® and Texin® TPU product portfolios, utilized globally in electronic enclosures, automotive interior surfaces, and medical device parts.

-

Market Capitalization: Approximately EUR 11.3 billion (~USD 13.1 billion) as of May 2026.

Arkema

-

About: Headquartered in France, Arkema is a leading global specialty chemicals enterprise structured around advanced materials, coating solutions, and adhesive systems.

-

Products: Celebrated for its ultra-premium Pebax® Polyether Block Amide (PEBA) thermoplastic elastomer line, which sets performance benchmarks in high-end athletic footwear, sports equipment, and medical catheters due to its energy return and lightweight characteristics.

-

Market Capitalization: Approximately EUR 4.5 billion (~USD 5.2 billion) as of May 2026.

Evonik Industries

-

About: Evonik Industries is a German specialty chemicals manufacturer focused on high-margin chemical matrices and specialty polymer modification technologies.

-

Products: Manufactures the Vestamid® E (PEBA) elastomer lines, prized for low-temperature impact strength, chemical resistance, and dimensional stability in extreme industrial environments.

-

Market Capitalization: Approximately USD 9.2 billion as of May 2026.

DuPont

-

About: An American multi-industrial innovator delivering highly specialized material portfolios to electronics, transportation, and construction markets.

-

Products: Produces the widely specified Hytrel® Thermoplastic Polyester Elastomer (TPC-ET) series, bridging the performance gap between rubbers and rigid plastics by providing flex-fatigue resistance and structural strength.

-

Market Capitalization: Approximately USD 21.1 billion as of May 2026.

Lubrizol Corporation

-

About: A specialty chemical company owned by Berkshire Hathaway, focused on advanced rheology modifiers, specialty additives, and engineered polymers.

-

Products: Offers the Estane® TPU asset base, a highly flexible polymer line utilized in demanding industrial applications, protective films, smart wearables, and medical devices.

-

Market Capitalization: Private Entity (Subsidiary of Berkshire Hathaway; standalone public market capitalization is not reported).

China Petrochemical Corporation (Sinopec Group)

-

About: Based in Beijing, Sinopec is one of the world’s largest oil refining, gas, and petrochemical conglomerates, controlling massive upstream and downstream supply networks.

-

Products: Mass-produces industrial-grade Styrenic Block Copolymers (SBC), Styrene-Butadiene-Styrene (SBS), and Styrene-Ethylene-Butylene-Styrene (SEBS) variants tailored for high-volume compounding, adhesive manufacturing, and asphalt modification.

-

Market Capitalization: State-owned enterprise / highly capitalized parent conglomerate holding multi-billion dollar public subsidiaries.

LG Chem

-

About: The largest chemical enterprise in South Korea, LG Chem possesses a highly diversified market presence stretching from petrochemical production to advanced battery materials.

-

Products: Manufactures the Keyflex® BT line of thermoplastic polyester elastomers (TPC-ET) alongside high-purity Polyolefin Elastomers (POE) engineered to improve impact resistance in automotive bumper assemblies.

-

Market Capitalization: Approximately USD 22.4 billion as of May 2026.

LCY Chemical Corporation

-

About: Headquartered in Taiwan, LCY Chemical Corporation focuses on performance plastics, solvents, and specialty electronic chemicals.

-

Products: A highly integrated manufacturer of Styrenic Block Copolymers (SBC), including Globalprene® SBS, SIS, and SEBS grades used in hot-melt adhesives, polymer modification, and elastic films.

-

Market Capitalization: Approximately USD 2.8 billion (Delisted from TWSE via private equity buyout, operating as an integrated private multinational group).

Dynasol Elastomers

-

About: A specialized joint venture between Repsol and Grupo KUO, creating a major global contender in the synthetic rubber and styrenic block copolymer sectors.

-

Products: Offers Calprene® and Solprene® solution-polymerized SBC structures, providing excellent elasticity, compound stability, and clarity in modified asphalt and consumer goods compounding.

-

Market Capitalization: Privately held joint venture matrix operation.

EMS-CHEMIE HOLDING AG

-

About: A Swiss chemical holding group operating extensively in high-performance polymers and specialty structural compounds.

-

Products: Offers Grilamid® EA and Grilflex® polyether amide TPE configurations, designed for fuel-line management, electronic components, and precision machinery seals.

-

Market Capitalization: Approximately CHF 15.6 billion (~USD 17.0 billion) as of May 2026.

Kraton Polymers LLC

-

About: A leading global producer of styrenic block copolymers and bio-based chemicals derived from pine wood pulping co-products.

-

Products: Developed the original Kraton® D (SBS/SIS) and Kraton® G (SEBS/SEPS) technological architectures, which are used globally in consumer care items, medical packaging, and compound modifications.

-

Market Capitalization: Acquired by DL Chemical; operates as an integrated private subsidiary.

Recent Developments by Major Companies

What strategic actions are market leaders taking to maintain competitive positioning?

The competitive landscape is seeing increased investment in sustainable production and targeted joint ventures. Market leaders are shifting away from general, low-margin products toward high-purity, bio-attributed, and circular elastomer grades.

-

BASF SE expanded its global footprint by scaling up bio-attributed and certified recycled-content Elastollan® TPU options. This helps processing clients track and reduce carbon emissions across their supply chains.

-

Covestro AG finalized deep-tier integration protocols for its high-performance circular TPU lines. These formulations integrate mechanically recycled post-industrial waste streams directly back into high-end automotive interior formulations.

-

Arkema invested heavily in expanding its bio-based Pebax® production capacity in France and Asia. This expansion directly targets high-performance sports and medical device sectors seeking lightweight materials with a reduced carbon footprint.

-

Kraton Polymers (under DL Chemical ownership) launched hydrogenated styrenic block copolymers (HSBC) engineered for complex medical packaging. This release supports the industry’s shift toward clean, PVC-free materials.

Future of the Market & Conclusion

The global Thermoplastic Elastomer market is entering a mature yet highly innovative growth phase. Its trajectory will be closely tied to advancements in processing technologies and sustainable chemistry. Over the next decade, the adoption of TPEs within advanced manufacturing will accelerate, led by the 3D Printing Segment’s rapid 10.4% CAGR. This shift will turn elastomeric prototyping into scalable, digitized production for personalized medical components and on-demand automotive parts.

Looking toward 2035, real-time material engineering will play a larger role, bringing functional smart TPEs with shape-memory properties and self-healing behaviors to the market. Companies that invest in high-performance chemistries like TPUs and bio-based alternatives, while securing reliable raw material supply chains, will be best positioned to capture high-margin growth. As industries continue to balance performance with sustainability, TPEs remain a key material solution for next-generation product design.

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Email: [email protected]

Leave a Reply