Executive Summary

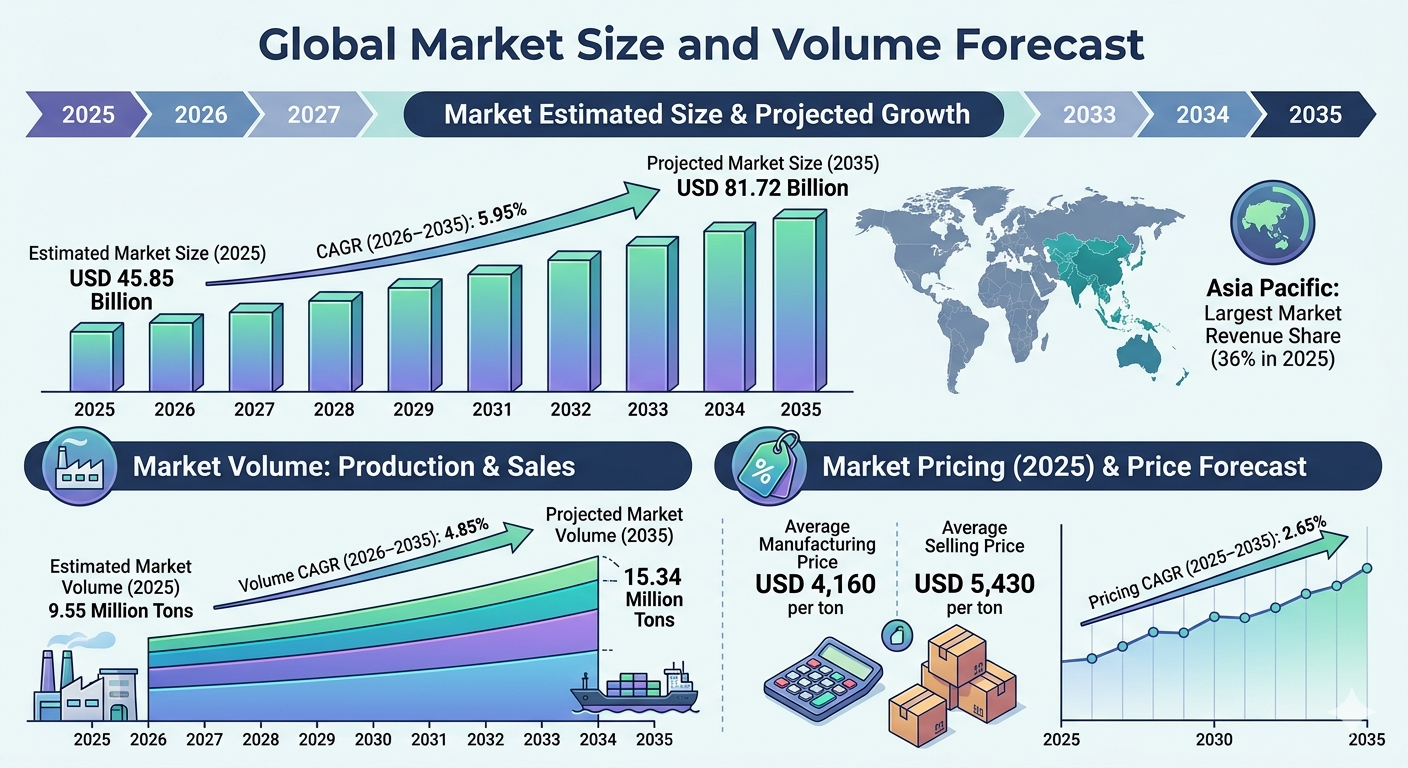

The global synthetic lubricants market is undergoing a fundamental transformation, driven by the dual requirements of extreme performance and environmental sustainability. Valued at USD 45.85 billion in 2025, the market is on a steady growth trajectory, projected to reach USD 81.72 billion by 2035 at a CAGR of 5.95%. As industries pivot toward more efficient, longer-lasting, and cleaner-burning solutions, synthetic lubricants have emerged as the standard for high-performance automotive and industrial machinery. By 2032, the market is poised to secure a dominant position in the global specialty chemicals landscape as manufacturers continue to refine base oil formulations to meet the evolving demands of modern engineering.

Market Overview

Synthetic lubricants are engineered fluids designed to provide superior performance, longevity, and protection compared to conventional mineral oils. By utilizing advanced base oils like polyalphaolefins (PAO) and esters, these lubricants offer enhanced thermal stability, lower volatility, and better flow characteristics across extreme temperature ranges. The transition toward synthetic products is now a core industrial requirement, ensuring that high-speed manufacturing components and advanced engine systems operate with maximum efficiency and minimal downtime.

What Are the Key Factors Driving the Market?

The market expansion is underpinned by three critical pillars: the increasing technical requirements of modern machinery, the global shift toward electric vehicles (EVs), and the pressure of tightening environmental regulations. Modern engines and industrial automation require lubricants that can withstand higher stress and heat, which traditional mineral oils cannot manage. Additionally, as automotive OEMs focus on fuel efficiency and extended service intervals, synthetic lubricants offer the necessary chemical stability to support these goals. Finally, environmental mandates are pushing the industry toward bio-degradable and low-emission synthetic solutions, ensuring that performance does not come at the cost of sustainability.

Market Recent Government Initiatives

Global regulatory frameworks are serving as a major catalyst for market growth. Stringent emissions standards, such as Euro 7 and similar mandates in North America and Asia, effectively compel vehicle manufacturers to adopt high-performance synthetic lubricants to achieve necessary fuel economy improvements. Furthermore, government-led industrial energy efficiency programs are incentivizing the use of advanced lubricants in manufacturing plants, as these products significantly reduce energy consumption and mechanical friction, aligning with broader national carbon neutrality targets.

Benefits of Using Synthetic Lubricants

The primary benefit of using synthetic lubricants is operational excellence. These fluids provide superior thermal stability, allowing machinery to operate in wider temperature ranges without compromising protection. Users experience extended drain intervals, which reduces maintenance costs and minimizes the waste generated by frequent oil changes. In an era where downtime is measured in thousands of dollars per hour, the ability of synthetic lubricants to safeguard assets against wear, oxidation, and sludge buildup makes them an indispensable investment for heavy-duty industrial and automotive operations.

Which Segment Accounted for the Largest Market Share?

In 2025, the Automotive segment held the dominant position with a 52% market share, reflecting the heavy reliance of the transport sector on performance-grade fluids. Regarding base oil types, the Polyalphaolefins (PAO) segment commanded the largest share at 39%, thanks to its exceptional thermal stability. Geographically, the Asia Pacific region led the market with a 36% revenue share, driven by rapid industrialization and a massive, growing vehicle population in China, India, and Japan.

| Metric | 2025 (Base) | 2035 (Projected) |

| Global Market Size | USD 45.85 Billion | USD 81.72 Billion |

| Global Market Volume | 9.55 Million Tons | 15.34 Million Tons |

| CAGR (2026-2035) | – | 5.95% |

Competitive Landscape

The competitive landscape is characterized by high-stakes innovation and strategic portfolio management. Major players are moving away from commodity lubricants toward specialized, high-margin synthetic solutions. Strategic moves often involve deep technical collaborations with automotive OEMs to develop “factory-fill” fluids that are tailored to specific engine architectures. Recent developments focus on synthesizing “greener” esters that offer the performance of PAOs while meeting stringent biodegradability requirements. This trend ensures that industry leaders can capture both the high-performance and eco-conscious segments of the market.

Top Companies Profiled

-

ExxonMobil: A global leader in synthetic base stocks (Mobil 1). Known for high-performance automotive and industrial lubricants.

-

Shell: Focuses on gas-to-liquid (GTL) technology and extensive aftermarket reach.

-

Chevron Corporation: Emphasizes high-quality base oil production and specialized industrial additives.

-

BP (Castrol): Highly regarded for R&D in transmission and engine oil efficiency for performance vehicles.

-

TotalEnergies: Actively investing in sustainable and low-carbon lubricant technologies.

Recent Developments by Major Companies

Industry leaders are currently optimizing their supply chains to prioritize high-performance base oils. Recent strategic developments include the deployment of AI-driven predictive maintenance services that monitor lubricant health in real-time, allowing industrial users to optimize fluid change cycles precisely. Major companies have also invested heavily in “low-viscosity” lubricant technology, which is critical for reducing friction in modern internal combustion engines and EV gearboxes. By combining hardware expertise with advanced chemical engineering, these firms are successfully moving from simple product suppliers to holistic “tribology partners” for their industrial and automotive clients.

Future Outlook

Looking toward 2035, the future of the synthetic lubricants market is intrinsically linked to the energy transition. As automotive fleets move toward electrification, the demand for traditional engine oils will evolve into a demand for specialized cooling and gear fluids for electric powertrains. The market will continue to reward those who invest in sustainable chemistry and high-performance base stock manufacturing. Ultimately, synthetic lubricants will remain a cornerstone of global industrial efficiency, proving that even in a greener future, the science of reducing friction is essential to industrial and transportation success.

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Email: [email protected]

Leave a Reply