Executive Summary

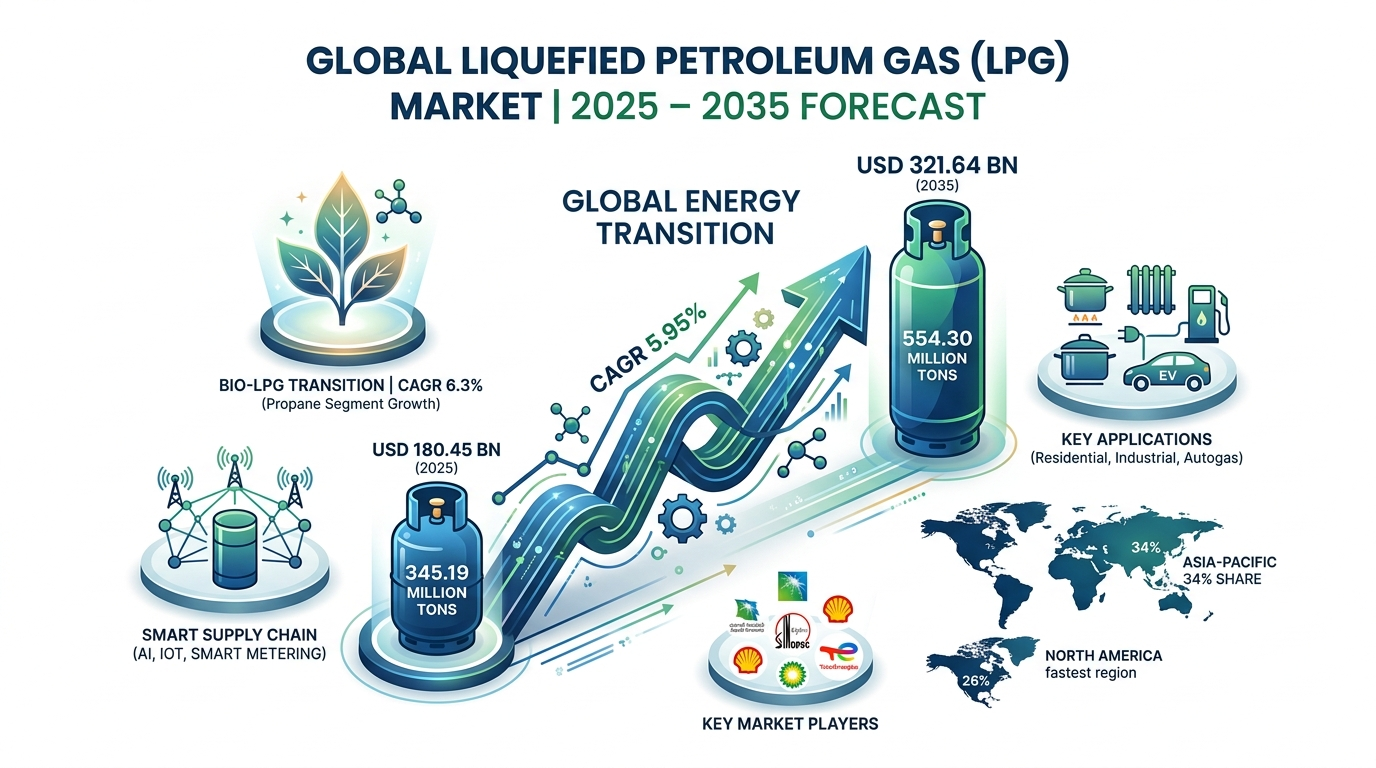

The critical role of gaseous hydrocarbons in balancing energy security with environmental stewardship remains highly pivotal. The global Liquefied Petroleum Gas (LPG) market size was estimated at USD 180.45 billion in 2025 and is projected to scale to an anticipated valuation of USD 321.64 billion by 2035. Over the forecast timeline spanning 2026 to 2035, this foundational low-carbon sector is positioned to expand at a steady Compound Annual Growth Rate (CAGR) of 5.95%.

In terms of physical production volume, the marketplace is forecasted to rise from 345.19 million tons in 2025 to 554.30 million tons by 2035, representing a volumetric CAGR of 4.85%. The structural evolution of the market is heavily propelled by strategic moves toward localized shale gas extraction, bio-synthetic transition loops, automated telemetry, and stringent cross-border clean cooking initiatives.

Market Overview & Architectural Significance

What is the Fundamental Value of the LPG Market?

The global Liquefied Petroleum Gas market functions as a resilient bridge toward low-carbon infrastructure, serving as an exceptional high-calorific feedstock and versatile fuel choice across multiple processing nodes. Produced as a non-discretionary co-product of natural gas processing and crude petroleum refining, LPG addresses the critical trilemma of energy cost, carbon reduction, and continuous baseload reliability. Its low greenhouse gas emission profile and ease of compression allow it to act as an immediate, plug-and-play energy security option for off-grid communities, large-scale industrial manufacturing, and expanding urban centers globally.

What Are the Key Structural Benefits of Using LPG?

-

High Thermal Density and Efficiency: LPG provides exceptional heat output with soot-free combustion, ensuring highly predictable thermal accuracy for sensitive operations like metal processing and kiln firing.

-

Portability and Grid Independence: It allows for seamless packaging into high-pressure cylinders or delivery via specialized cryogenic tankers, offering stable utilities without requiring multi-billion-dollar piped network footprints.

-

Immediate Carbon Reductions: Shifting residential and light commercial users away from solid fuels (such as coal or biomass) directly curtails indoor air pollution and heavy carbon intensity.

-

Feedstock Adaptability: Serves as an excellent, sulfur-free chemical input for stream cracking and propane dehydrogenation (PDH) loops to manufacture essential high-value polymers.

In-Depth Market Dynamics & Driving Factors

What Are the Primary Factors Driving Market Expansion?

-

Aggressive State Mandates for Clean Cooking Fuel: Major public health campaigns across emerging economies actively incentivize households to swap toxic solid fuels for reticulated or cylinder-based LPG.

-

Booming Global Shale Gas Extraction: The continuous expansion of non-associated gas fields ensures a highly reliable, high-volume baseline of natural gas liquids (NGLs), reducing production cost volatility.

-

Emergence of Hybrid Energy Microgrids: Industrial operators are increasingly deploying mixed solar-wind systems utilizing backup LPG generators to safeguard remote operations against weather-driven power disruptions.

What Factors Restrain Market Progression?

-

High Initial Logistics Costs: Storing and transporting highly flammable, pressurized gases demands specialized maritime carriers, heavy bulk terminals, and precise leakage testing arrays. This heavy capital layout can slow initial expansion across lower-income regions.

Key Market Trends & Advanced Technological Shifts

What Key Technological Trends Are Altering the LPG Industry?

The contemporary LPG market is undergoing an automated overhaul driven by the Industrial Internet of Things (IIOT) and Edge AI. Bottling plants are rapidly incorporating automated, high-speed vision lines to detect microscopic valve defects before delivery. Concurrently, utility companies are rolling out smart cylinders with integrated telemetry sensors. These sensors feed real-time usage data directly to regional distribution centers, optimizing transport routing, cutting down delivery footprints, and eliminating localized stockouts.

The Transition to Sustainable Bio-LPG Formulations

Furthermore, heavy research and capital investments are flowing into bio-LPG derived from organic waste streams, vegetable oils, and biological residues. Because renewable propane functions as a drop-in molecule within current logistics assets, it allows automotive commercial fleets and high-volume industrial users to hit strict carbon-neutral targets without requiring costly modifications to their existing handling infrastructure.

Segmental Analysis & Dominant Market Share

Which Segment Accounted for the Largest Market Share?

The Natural Gas-Based LPG segment dominated the industry, holding 54% of the global revenue share in 2025 and projecting the fastest segment expansion at a 6.30% CAGR. This dominant position is supported by its superior chemical consistency, lower sulfur content, and direct volume extraction during natural gas liquid processing.

-

Propane Product Type (49% Revenue Share in 2025): Leads the market and is expanding at a 6.10% CAGR, owing to its reliable high vapor pressure for off-grid space heating and polymer manufacturing.

-

Residential Application (41% Market Share in 2025): Represents the largest application base, functioning as an inelastic domestic energy resource for space heating and cooking.

-

Cylinder Distribution Channel (58% Total Share in 2025): Commands the channel segment due to its high touchpoint frequency in consumer markets, although the Bulk & Tanker segment is growing rapidly at a 6.20% CAGR.

-

Household End-Use Industry (39% Market Share in 2025): Dictates dominant consumption curves, while the Automotive segment targets the fastest growth at a 6.90% CAGR due to rising conversion incentives for commercial transit fleets.

Global LPG Value, Volume, and Pricing Forecast

| Market Attribute | 2025 (Base Year) | 2026 (Forecast Start) | 2035 (Target Year) | Sector CAGR (2026–2035) |

| Market Value (USD) | $180.45 Billion | $191.19 Billion | $321.64 Billion | 5.95% |

| Market Volume (Tons) | 345.19 Million | 361.93 Million | 554.30 Million | 4.85% |

| Avg. Mfg Price / Ton | $415 | — | — | Pricing CAGR: |

| Avg. Selling Price / Ton | $625 | — | — | 3.70% |

Regional Landscape & Geographic Trends

How Did Asia-Pacific Dominate the LPG Landscape?

The Asia-Pacific region represents the largest economic theater for the LPG sector, securing a commanding 34% global market share in 2025. Valued at USD 61.35 billion in 2025, the regional market is on track to hit USD 110.97 billion by 2035, advancing at the fastest rate with a 6.80% CAGR.

This massive growth is anchored by extensive propane dehydrogenation (PDH) assets across China and large-scale state fuel substitution efforts in India. China operates as a key global import hub and a major pricing driver, utilizing automated smart utility grids and expanding its chemical manufacturing infrastructure to build integrated energy-to-chemical setups.

North American Growth Trajectory

North America captured 26% of the global market share in 2025 and is tracking a steady 5.50% CAGR. The region maintains a highly resilient position as a leading net exporter, supported by deep natural gas liquid extraction networks along the U.S. Gulf Coast. This region also serves as a hub for sustainable product development, leading the deployment of bio-LPG via localized tax credits and green energy initiatives.

Recent Government Initiatives & Regulatory Landscape

National policy shifts continue to reshape global production and trade frameworks:

-

European Union: Driven by the EU Gas Storage Regulations and Decarbonization Acts, policies enforce strict reporting protocols while promoting alternative, non-fossil bio-LPG options to advance net-zero corporate compliance targets.

-

North America: The implementation of the Renewable Fuel Standard (RFS) alongside targeted federal investment credits provides robust financial incentives for bio-based scaling, while EPA methane rules keep upstream resource recovery tight.

-

Asia-Pacific: Governments prioritize local energy sovereignty by managing floating storage regasification unit (FSRU) terminal licensing and providing targeted consumer subsidies to expand reticulated pipelines in high-density areas.

Competitive Landscape & Top Companies

The global liquefied petroleum gas market features international oil companies and state-backed energy enterprises focused on long-term supply agreements and deep petrochemical integration.

1. Saudi Arabian Oil Co. (Saudi Aramco)

-

About: Headquartered in Dhahran, Saudi Arabia, Saudi Aramco is the largest integrated oil and gas enterprise globally, managing massive upstream reserves and an extensive NGL recovery network.

-

Products: High-purity commercial propane, commercial butane, and tailored seasonal LPG mixtures distributed to major global industrial hubs.

-

Market Capitalization: Approximately USD 1.84 Trillion (May 2026).

2. China Petroleum & Chemical Corporation (Sinopec)

-

About: Based in Beijing, China, Sinopec is one of the world’s largest refining, gas processing, and petrochemical conglomerates, functioning as a primary producer and consumer of chemical feedstocks.

-

Products: Refinery-based LPG, specialized polymer-grade propane, mixed butane fractions, and automated retail cylinder delivery networks.

-

Market Capitalization: Approximately HKD 610.50 Billion (~USD 78.10 Billion) (May 2026).

3. TotalEnergies SE

-

About: Operating out of Courbevoie, France, TotalEnergies is a major global energy player actively executing a broad transition into biofuels, green hydrogen, and renewable gas portfolios.

-

Products: Eco-friendly Bio-LPG, wholesale bulk tanker gas supply, marine autogas solutions, and digital cylinder distribution tracking assets.

-

Market Capitalization: Approximately EUR 148.90 Billion (~USD 161.40 Billion) (May 2026).

What Strategic Industry Agreements Have Been Signed Recently?

-

November 2025: Indian state-run oil companies (IOCL, BPCL, and HPCL) successfully completed long-term import arrangements with major U.S. suppliers. This framework secures the consistent delivery of 2.2 million metric tonnes per annum of LPG sourced directly from the U.S. Gulf Coast, stabilizing supply resilience for the 2026 trading year.

-

April 2025: Sinopec and Saudi Aramco finalized a joint venture framework agreement focused on expanding the Yanbu refinery in Saudi Arabia. This major project includes the integration of a large-capacity mixed-feed steam cracker and an aromatics plant, creating a highly streamlined downstream refining and chemical complex.

Future Horizon: The Strategic Outlook

The global LPG market is positioned for continuous evolution, driven by its dual identity as an essential transitional fuel and a reliable chemical feedstock. As conventional crude refining faces changing dynamics from vehicle electrification, the market will increasingly lean on natural gas liquids and shale extraction to maintain steady supply liquidity.

The long-term commercial edge will belong to chemical and energy producers that successfully integrate digital asset tracking, expand smart piped networks, and scale up domestic bio-LPG sourcing. By maintaining competitive pricing against alternative natural gas paths and securing long-term trade agreements, LPG will preserve its vital role in the global energy matrix over the coming decade.

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Email: [email protected]

Leave a Reply