The stabilization and modification of high-performance elastomers remain structurally dependent on specialized liquid synthetic rubbers. The global liquid polybutadiene market size was estimated at USD 2.55 billion in 2025 and is projected to reach USD 4.90 billion by 2035. Over the forecast period from 2026 to 2035, this critical polymer additives sector is poised to grow at a Compound Annual Growth Rate (CAGR) of 6.75%.

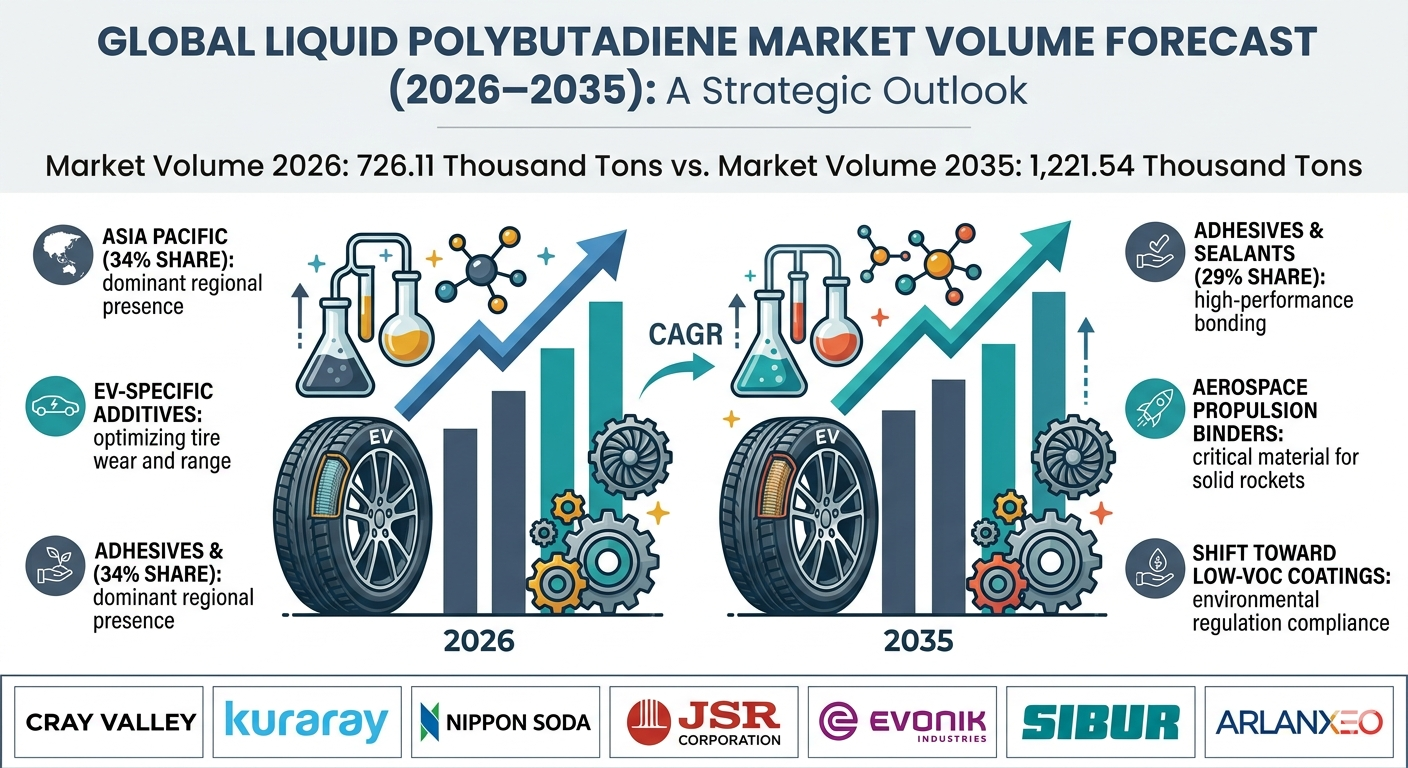

In terms of material volume, the industry is anticipated to scale from 685.33 thousand tons in 2025 to 1,221.54 thousand tons by 2035, exhibiting a volumetric CAGR of 5.95%. This long-term macroeconomic progression is primarily driven by escalating international demand for high-performance elastomers in automotive tires, balanced with high-growth specialty segments in low-volatile organic compound (low-VOC) coatings, bio-based adhesives, and advanced aerospace propulsion binders.

Market Overview & Architectural Significance

Why Is Market Importance Critical to Modern Industry?

The liquid polybutadiene (LPBD) market represents a vital cornerstone for the advanced materials sector, serving as a low-molecular-weight synthetic rubber distinguished by high elasticity, excellent resilience, and exceptional chemical resistance. In an era marked by shifting regulatory pressures and an urgent demand for lightweight structures, LPBD functions as a highly adaptable reactive intermediate.

Its unique fluid nature enables dual functionality: it serves as a co-vulcanizing agent that structurally cross-links rubber matrix networks and a reactive plasticizer that improves standard polymer processability without compromising cross-linked physical integrity. Beyond its fundamental integration into mainstream tire manufacturing, LPBD is a key additive across high-stakes industries, acting as a structural binder for solid rocket propellants, protective electrical potting encapsulation compounds, and heavy-duty industrial sealants.

What Benefits Arise From Using Liquid Polybutadiene?

Integrating liquid polybutadiene into chemical synthesis and elastomeric compounds yields definitive performance enhancements:

-

Superior Mechanical Toughness: Functions as a highly effective impact modifier, significantly improving the crack resistance and structural toughness of brittle plastics and cyclic resins.

-

Low-Temperature Flexibility: Possesses an extremely low glass transition temperature, allowing end products like marine coatings and aerospace components to maintain optimal flexibility and elasticity in sub-zero environments.

-

Optimized Dynamic Rubber Properties: When blended into tire tread compounds, LPBD minimizes rolling resistance to elevate fuel efficiency while expanding surface wear resistance and structural lifespan.

-

Excellent Substrate Adhesion: Delivers robust chemical resistance and high surface wetting properties, serving as a preferred base resin for waterproof construction sealants and strong industrial adhesives.

Technical Framework and In-Depth Market Dynamics

What Are the Key Factors Driving The Market?

-

Surging Demand for Low-Rolling-Resistance Tires: The automotive sector’s rapid shift toward electric vehicles (EVs) mandates structural tire modifications to accommodate heavier battery configurations. High-performance LPBD additives optimize rubber-filler interactions, reducing vehicle energy loss and expanding active battery range.

-

Widespread Infrastructure Modernization and Urbanization: Surging commercial and residential building development globally drives massive volume requirements for low-viscosity construction adhesives and high-purity sealants that rely on polybutadiene backbones to resist environmental weathering.

-

Rising Global Defense and Aerospace Expenditures: Increased geopolitical allocations drive long-term procurement programs for hydroxyl-terminated polybutadiene (HTPB), which operates as the premier high-purity binder matrix for solid rocket motors.

What Are the Primary Restraints Limiting Expansion?

-

Stringent Environmental Frameworks and Regulatory Pressures: Conventional liquid polybutadiene processing loops remain under intense scrutiny due to trace hazardous chemical handling and residual VOC limits. Furthermore, a pronounced lack of widespread technical awareness and limited logistical accessibility across developing economies can hinder initial product adoption rates.

What Is the Core Future Opportunity in the Sector?

-

Green Polymer Synthesis and Bio-Based Formulations: Transitioning manufacturing setups away from fossil-based monomers and toward renewable plant-derived oils or liquid farnesene rubber (LFR) unlocks a strong competitive advantage. This satisfies shifting consumer sustainability expectations while insulating operational costs from petrochemical price volatility.

Key Market Trends & Advanced Technological Shifts

What Technological Innovations Are Transforming the Market?

The liquid polybutadiene landscape is undergoing a major technical transformation led by automation and cleaner chemical architecture. Forward-thinking producers are successfully implementing advanced catalytic polymerization systems to tightly control terminal functionality, vinyl content, and molecular weight distribution.

The primary market emphasis is transitioning toward specialized functionalized liquid rubbers, including carboxyl-terminated (CTPB) and vinyl-terminated (VTPB) variants. These modified polymers are engineered to maximize chemical cross-linking with secondary substrates. This eliminates the need for volatile solvent additives, actively supporting the paint and coatings industry’s global push toward clean, low-VOC formulations.

The Rise of Sustainable Raw Material Synthesis

Concurrently, the integration of bio-based monomers represents a highly prominent trend in the marketplace. Major companies are actively deploying alternative synthesis routes to replace conventional butadiene feedstocks with renewable sugars and terpenes. This facilitates the production of eco-friendly liquid rubbers that maintain performance benchmarks while minimizing the aggregate environmental footprint.

Segmental Architecture & Dominant Market Shares

Which Segments Accounted for the Largest Market Share?

The Medium Molecular Weight segment led the global landscape, commanding 46% of the revenue share in 2025, and is anticipated to post the fastest growth at a 7.10% CAGR. This structural dominance is driven by its exceptional material versatility, providing a balanced viscosity-to-strength profile that satisfies processing needs across multiple industrial sectors.

-

Hydroxyl-Terminated Polybutadiene (HTPB) (51% Type Share in 2025): Dominates the type segment and is projected to expand at a 7.20% CAGR, heavily propelled by its exceptional binding properties and mandatory utilization across defense-related solid propulsion projects.

-

Adhesives & Sealants Application (29% Share in 2025): Holds the premier application position due to surging global construction and infrastructure modernization projects requiring long-lasting environmental seals.

-

Construction End-Use Industry (26% Share in 2025): Establishes the largest end-use footprint, though the Aerospace & Defense end-use segment (18% share) is poised to grow at the fastest 7.50% CAGR due to increased geopolitical investments.

-

Direct Sales Channel (57% Distribution Share in 2025): Dominates the landscape, driven by high-volume, multi-year procurement contracts between primary chemical processors and tier-one automotive or aerospace manufacturers.

Global Liquid Polybutadiene Value, Volume, and Pricing Forecast

| Attribute | 2025 (Base Year) | 2026 (Forecast Start) | 2035 (Target Forecast) | Sector CAGR (2026–2035) |

| Market Value (USD) | $2.55 Billion | $2.72 Billion | $4.90 Billion | 6.75% |

| Market Volume (Tons) | 685.33 Thousand | 726.11 Thousand | 1,221.54 Thousand | 5.95% |

| Avg. Mfg Price / Ton | $2,160 | — | — | Pricing CAGR: |

| Avg. Selling Price / Ton | $2,790 | — | — | 3.95% |

Regional Analysis: Geographic Consolidation

How Did Asia-Pacific Dominate the Liquid Polybutadiene Market?

The Asia-Pacific region represents the core locomotive of the global liquid polybutadiene market, securing a commanding 34% market share in 2025. Valued at USD 0.87 billion in 2025, the regional market is projected to reach USD 1.69 billion by 2035, progressing at the fastest international rate with a 7.80% CAGR.

This dominant regional profile is driven by rapid urbanization and extensive tire manufacturing infrastructure across China and India. China leads the regional consumption curve, driven by intensive local investments in advanced electronics, high-performance rubber compounds, and localized production networks designed to minimize automotive component import dependencies.

North American Market Trends

North America maintained a highly stable 25% market share in 2025, exhibiting a projected growth CAGR of 6.20%. The region’s market architecture is heavily defined by a robust defense manufacturing footprint in the United States, alongside strict regulatory mandates from environmental protection agencies that accelerate the commercial transition toward eco-friendly, low-VOC formulation ingredients.

Market Recent Government Initiatives & Regulatory Landscape

Industrial polymer synthesis operations are continuously shaped by regional safety and carbon neutrality targets:

-

Europe (European Union): The ongoing enforcement of the REACH framework places strict regulatory thresholds on residual monomers and VOC tracking. Future European Commission mandates are anticipated to favor bio-based alternatives and fully recyclable synthetic configurations to align with cross-border carbon neutrality targets.

-

North America (United States & Canada): Regulatory bodies enforce strict hazardous workplace protocols regarding volatile chemical handling, while simultaneously mandating high-stakes performance and safety certifications for materials deployed across defense and aerospace environments.

-

Asia-Pacific: Regional ministries are actively backing public-private R&D frameworks for electric vehicle components and lightweight composites. This provides direct regulatory support and fast-tracked approvals for cleaner material formulations and innovative catalyst setups.

Competitive Landscape & Top Companies

The global liquid polybutadiene market features specialized chemical innovators investing heavily in functionalized grade expansions and green polymer synthesis assets.

1. TotalEnergies (Cray Valley)

-

About: Operating as a specialized subsidiary of TotalEnergies, Cray Valley is a premier global manufacturer of specialty functional additives and low-molecular-weight liquid polybutadiene resins.

-

Products: Ricon® liquid polybutadiene resins, Krasol® hydroxyl-terminated liquid rubbers, and Ricobond® functionalized coupling agents used to optimize rubber-to-filler interactions.

-

Market Capitalization: Approximately USD 162.40 Billion (TotalEnergies parent market valuation as of May 2026).

2. Kuraray Co., Ltd.

-

About: Headquartered in Tokyo, Japan, Kuraray is a world-leading chemical innovator renowned for its advanced synthetic fiber engineering and high-performance functionalized liquid rubber portfolios.

-

Products: High-purity Liquid Polybutadiene (LBR), Liquid Isoprene Rubber (LIR), and innovative bio-based Liquid Farnesene Rubber (LFR) configurations designed for high-performance tire compounds.

-

Market Capitalization: Approximately JPY 544.20 Billion (~USD 3.51 Billion) (as of May 2026).

3. Nippon Soda Co., Ltd.

-

About: Based in Tokyo, Japan, Nippon Soda is a diversified chemical manufacturer specializing in agrochemicals, advanced plastics processing aids, and high-purity functional polymers.

-

Products: NISSO-PB® series liquid polybutadiene (including highly reactive dicarboxylic acid-terminated and hydroxyl-terminated specialized grades).

-

Market Capitalization: Approximately JPY 168.10 Billion (~USD 1.08 Billion) (as of May 2026).

What Is the Status of Recent Strategic Product Developments?

-

February 2026: Evonik Industries announced a major strategic expansion of its hydroxyl-terminated polybutadienes (HTPB) global production capabilities. The initiative includes a major production capacity increase at its centralized chemical facility in Marl, Germany, projected to achieve full commercial operation by Q2 2027, alongside concurrent engineering blueprints for a brand-new HTPB manufacturing site located in Asia to serve high-growth defense and adhesive markets.

Future Horizon: The Strategic Outlook

The future of the global liquid polybutadiene market will be defined by a careful balance between maximizing dynamic material properties and meeting strict global sustainability standards. While conventional solid synthetic rubber modifications remain a massive volume base, high-margin commercial rewards will favor chemical entities that successfully master precision functionalization.

Over the coming decade, the market will increasingly transition toward bio-derived monomer inputs and advanced continuous polymerization techniques. Companies that focus on developing low-VOC resins, high-purity aerospace HTPB lines, and high-efficiency tire additives will successfully protect their manufacturing margins from fossil feedstock fluctuations, securing a resilient position in the global chemical and materials supply chain.

Segment Breakdown by Market Share (Base Year 2025)

| Segment Type | Category Focus | 2025 Revenue Share (%) | Key Segment Driver |

| Molecular Weight | Medium Molecular Weight | 46% | Balanced viscosity-to-strength ratios across multiple sectors. |

| Low Molecular Weight | 34% | Surging demand in liquid sealants and industrial coatings. | |

| High Molecular Weight | 20% | Mechanical strength benefits in high-performance rubber. | |

| Product Type | Hydroxyl-Terminated (HTPB) | 51% | Extensive utilization across aerospace propulsion binders. |

| Non-Functionalized | 18% | Cost-effective solutions for mass industrial rubber modification. | |

| Carboxyl-Terminated (CTPB) | 17% | Elevated chemical reactivity for advanced coatings. | |

| Application | Adhesives & Sealants | 29% | Expanding global infrastructure and building activities. |

| Rubber Modification | 21% | Rising global automotive tier-one tire manufacturing volumes. | |

| Aerospace & Defense | 20% | Rising consumption of advanced solid propellant formats. |

Regional Volume and Revenue Distribution (2025)

| Geographic Region | 2025 Revenue Share (%) | Projected Regional Growth Profile |

| Asia-Pacific | 34% | Dominant region; expanding at the fastest 7.80% CAGR. |

| North America | 25% | Strong aerospace presence; focus on low-VOC compliant components. |

| Europe | 22% | High concentration of automotive OEMs; transitioning under REACH. |

| Latin America | 10% | Steady expansion of localized industrial manufacturing assets. |

| Middle East & Africa | 9% | Growing industrial infrastructure and energy applications. |

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Email: [email protected]

Leave a Reply