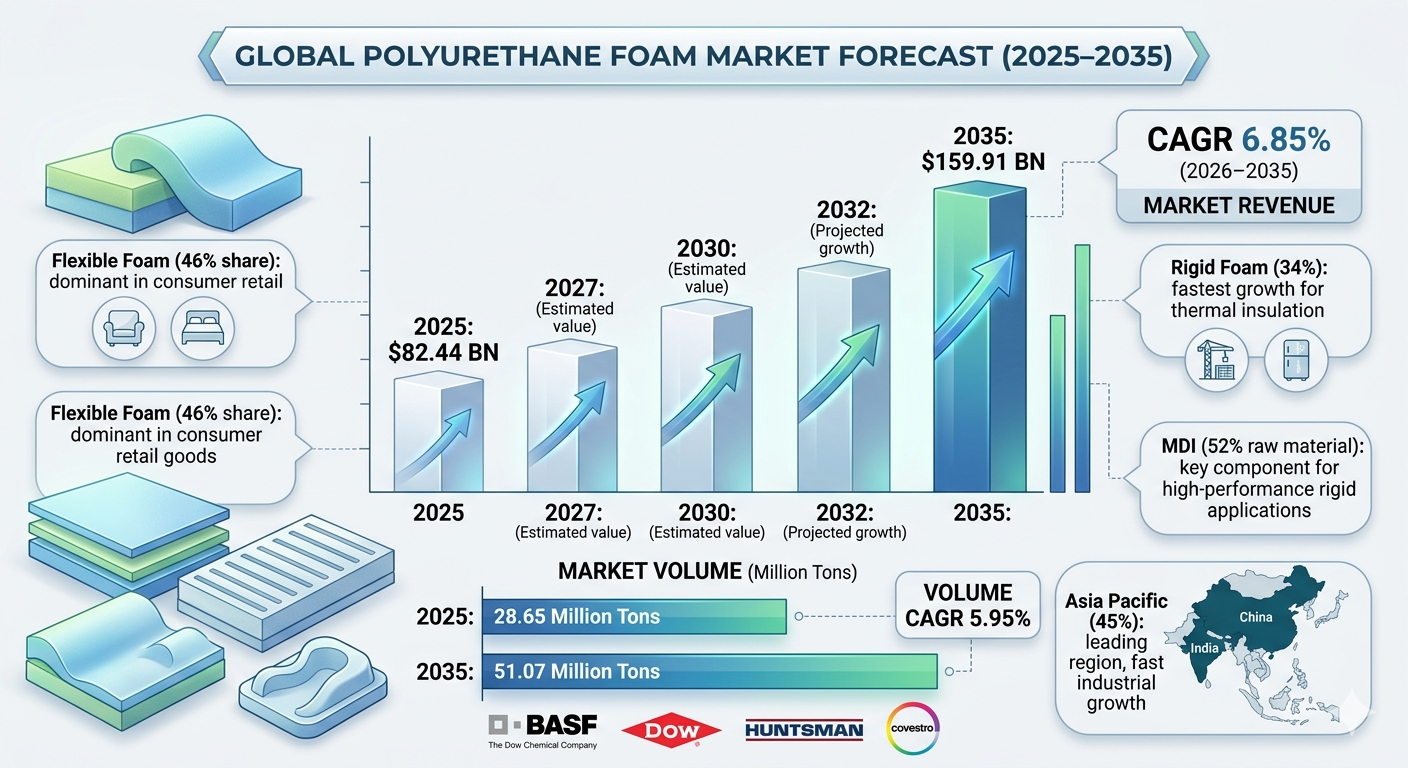

The rapid evolution of modern infrastructure and automotive architectures remains deeply reliant on high-performance chemical engineering inputs. The global polyurethane foam market size was valued at USD 82.44 billion in 2025 and is projected to reach USD 159.91 billion by 2035. Over the intensive forecast horizon stretching from 2026 to 2035, this specialized chemical and materials sector is poised to expand at a steady Compound Annual Growth Rate (CAGR) of 6.85%.

In terms of volumetric scale, the industry is estimated to advance from 28.65 million tons in 2025 to 51.07 million tons by 2035, moving at a physical CAGR of 5.95%. This structural growth is primarily accelerated by a global surge in lightweight material engineering, precision protective packaging, and strict thermal insulation regulations.

Market Overview & Technical Framework

Why Is Polyurethane Foam Critical to Modern Industry?

Polyurethane foam serves as an indispensable material in industrial design, praised for its lightweight composition, structural durability, and unique cellular ability to trap air efficiently. Synthesized through an exothermic reaction mixing liquid polyols and diisocyanates with specific catalysts, this material expands rapidly into specialized low-, medium-, or high-density open-cell or closed-cell structures.

Its foundational insulation properties make it an essential element for maximizing energy efficiency in residential appliances, while its variable density allows it to provide premium ergonomics in commercial upholstery and protective safety in industrial packaging networks.

What Is Driving Long-Term Market Growth?

Market expansion is materializing through a coordinated demand wave from both urban infrastructure developers and transportation manufacturers. The structural push for energy-saving, low-carbon building envelopes requires extensive use of spray and rigid insulation foams to form continuous thermal barriers against heat flow.

Concurrently, global automotive manufacturers are heavily investing in structural weight-reduction strategies to expand vehicle battery range and fuel efficiency, positioning polyurethane foam as a key engineering substrate for next-generation interior seating and structural components.

Market Dynamics & Analytical Insights

What Are the Primary Factors Driving The Market?

-

Aggressive Expansion of Energy-Efficient Buildings: Rising adoption of green building codes globally accelerates the installation of rigid boardstock and spray foam insulation to prevent structural thermal bridging.

-

Automotive Lightweighting & Fleet Electrification: The urgent engineering requirement to scale back vehicular curb weight in electric vehicle (EV) fleets drives high-volume consumption of molded flexible components.

-

Consumer Demand for Premium Comfort: Rising urbanization and disposable incomes globally trigger continuous retail replacement cycles for high-density mattress substrates and advanced ergonomic office furnishings.

What Are the Key Restraints Limiting Market Expansion?

-

Volatile Chemical Feedstock Costs and Strict Ecological Oversight: Legacy polyurethane manufacturing relies fully on specific isocyanates (MDI/TDI) that release volatile organic compounds (VOCs) and hazardous air pollutants during primary processing. This exposes manufacturers to highly restrictive regulatory compliance frameworks (like OSHA and REACH) and elevates overall factory conversion costs. Furthermore, the lack of widespread chemical recycling options for cross-linked polyurethane thermosets leaves the sector exposed to long-term landfill and waste management challenges.

What Is the Core Future Opportunity in the Sector?

-

Bio-Based Material Innovation and Smart Infrastructure Assets: Integrating bio-derived polyols (harvested from natural vegetable oils) into standard chemical processing loops allows brands to command a green price premium. Additionally, the rollout of smart cities and the expansion of medical-grade supportive cushioning present untapped, high-margin commercial pipelines.

Segmental Architecture & Dominant Market Shares

Which Product Type Segment Accounted for the Largest Market Share?

The Flexible Foam segment led the global market, accounting for 46% of the revenue share in 2025, due to its widespread integration into high-volume consumer goods like cushions, commercial seating, and bedding solutions.

-

Rigid Foam (34% Share in 2025): Projecting the fastest sub-sector growth with a 7.2% CAGR, driven by its superior thermal resistance and extensive deployment across structural building panels and commercial refrigeration insulation.

-

Spray Polyurethane Foam (20% Share in 2025): Expanding steadily due to its excellent fluid-applied sealing capabilities that effectively fill architectural gaps to eliminate air leakage.

Raw Material, End-Use, and Application Breakdown

-

MDI Base Supremacy (52% Share in 2025): Captures the majority market share and is expected to grow at the fastest 7.1% CAGR, owing to its foundational role in rigid foam formulations and its safer industrial handling profile over alternatives.

-

Residential & Furnishings Dominance (48% and 32% Shares): Driven by high-volume requirements for daily domestic furniture, household appliances, and residential structural insulation.

-

Low-Density Configurations (38% Share): Maintains its top volume position due to its excellent balance of softness and cost-efficiency in mass-market consumer applications.

Polyurethane Foam Market Value, Volume, and Pricing Forecast

| Attribute | 2025 (Base Year) | 2026 (Forecast Start) | 2035 (Target Forecast) | Segment CAGR (2026–2035) |

| Market Value (USD) | $82.44 Billion | $88.09 Billion | $159.91 Billion | 6.85% |

| Market Volume (Tons) | 28.65 Million | 30.35 Million | 51.07 Million | 5.95% |

| Avg. Mfg Price / Ton | $2,160 | — | — | Pricing CAGR: |

| Avg. Selling Price / Ton | $2,790 | — | — | 3.25% |

Regional Analysis: Geographic Consolidation

How Will Asia-Pacific Dominate the Polyurethane Foam Market?

The Asia-Pacific region represents the primary engine of the industry, commanding a dominant 45% market share in 2025. Valued at USD 37.10 billion in 2025, the regional market is projected to reach USD 72.76 billion by 2035, growing at a rapid 7.6% regional CAGR.

This massive expansion is propelled by China’s colossal manufacturing base and massive domestic construction pipeline, paired with rising disposable incomes across India and Southeast Asia that boost automotive and appliance sales. Low conversion costs and supportive industrial expansion frameworks make it a preferred hub for multinational chemical capacity additions.

North American Growth Metrics

North America secured a notable 22% market share in 2025, focusing heavily on product sustainability and smart infrastructure investments. Market development across the United States is anchored by high-end research into bio-based polyols and strict building codes that mandate high-efficiency building insulation.

Market Recent Government Initiatives & Regulatory Landscape

Industrial manufacturing assets must continuously realign their chemical production loops to comply with changing environmental frameworks:

-

United States (EPA): Rolled out the Water Reuse Action Plan (WRAP) 2.0 in April 2026, which impacts production logic by scaling up industrial wastewater recycling across high-intensity mineral extraction and chemical synthesis sites.

-

European Union (European Commission): Enforces Regulation (EU) 2020/741 (effective June 2023), establishing strict water quality benchmarks to advance the circular economy across industrial chemical processing zones.

-

China (MEE): Enforced the national-level Regulations on Water Conservation in May 2024, setting a strict target of 25% wastewater reuse in water-scarce industrial zones and forcing chemical processing centers to upgrade to water-saving technologies.

Competitive Landscape & Key Companies

The global marketplace is highly consolidated, with leading chemical giants prioritizing bio-based alternatives and precision digital manufacturing systems to cater to highly customized industrial requirements.

1. BASF SE

-

About: A prominent German chemical conglomerate and a global leader in industrial chemical manufacturing, operating production assets across more than 80 countries.

-

Products: Elastollan® systems, critical polyols, specialized isocyanates, and WALLTITE insulation lines.

-

Market Capitalization: Approximately EUR 47.31 Billion (~USD 54.29 Billion) (as of May 2026).

2. The Dow Chemical Company

-

About: A major American subsidiary of Dow Inc., operating as a leading global manufacturer of advanced plastics, coatings, and specialized synthetic chemical intermediates.

-

Products: Tailored VORANOL™ polyols, specialized ISONATE™ pure isocyanates, and high-performance silicone surfactants.

-

Market Capitalization: Approximately USD 25.96 Billion (as of May 2026).

3. Huntsman Corporation

-

About: A publicly traded American manufacturer specializing in differentiated chemical processing, recognized as a global leader in MDI-based polyurethane architectures.

-

Products: SUPRASEC® MDI isocyanates, JEFFOL® specialty polyols, and advanced thermal insulation foams.

-

Market Capitalization: Approximately USD 2.54 Billion (as of May 2026).

What Is the Status of Recent Strategic Product Developments?

-

December 2025: BASF officially introduced WALLTITE RSB, its newest product line of closed-cell spray polyurethane foam insulation. This advanced system is designed to improve structural sustainability profiles and meet the rising global demand for certified eco-friendly construction components.

Future Horizon: The Strategic Outlook

The next decade of the polyurethane foam market will be defined by a shift from legacy bulk manufacturing to smart, circular, and precision-engineered material lines. While flexible foam will maintain its high volume dominance in consumer retail goods, long-term market premiums will be captured by entities that successfully commercialize fully recyclable thermoset systems and bio-based alternatives.

As global regulatory bodies enforce stricter limits on chemical emissions and waste management, the industry will reward technical efficiency over raw volume. Companies that invest in low-VOC formulas, automated digital density controls, and high-performance rigid insulation systems will successfully insulate their supply chains from fossil feedstock volatility, securing a resilient position in the global manufacturing ecosystem.

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Email: [email protected]

Leave a Reply