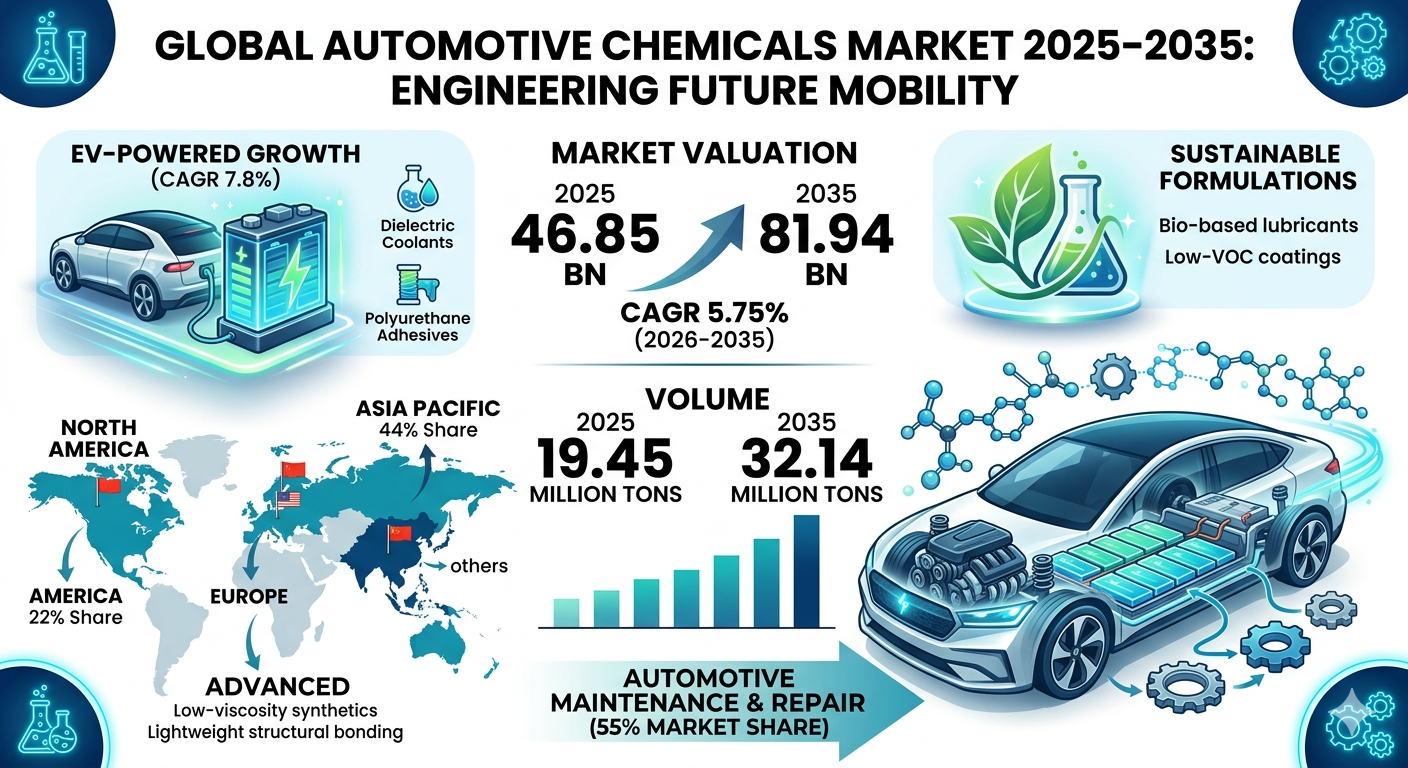

The shifting paradigm of global mobility necessitates an ultra-precise evaluation of chemical interventions that guarantee vehicle reliability, lightweighting, and electrification infrastructure. The global automotive chemicals market size was estimated at USD 46.85 billion in 2025 and is projected to reach USD 81.94 billion by 2035. Over the forecast period from 2026 to 2035, this market is poised to grow at a Compound Annual Growth Rate (CAGR) of 5.75%.

In terms of material volume, the industry is anticipated to scale from 19.45 million tons in 2025 to 32.14 million tons by 2035, exhibiting a volumetric CAGR of 5.15%. The underlying expansion is heavily sustained by the dual pressures of stringent environmental regulations and structural design overhauls geared toward high-performance e-mobility and advanced lightweighting.

Market Overview & Architectural Significance

Why Is Market Importance Critical to the Automotive Ecosystem?

Automotive chemicals serve as the molecular baseline for modern vehicular structural integrity, powertrain thermal management, and long-term lifecycle optimization. From synthetic esters that prevent boundary friction in extreme kinetic environments to structural adhesives that redistribute stress across multi-material lightweight car frames, these chemical formulations dictate the physical boundaries of modern automotive engineering. They are no longer treated as passive consumables but as integrated components essential for satisfying stringent corporate average fuel economy (CAFE) metrics and battery insulation standards.

What Is Market Growth Driven By in the Current Decade?

The market growth is structurally supported by a multi-tiered expansion across traditional internal combustion engine (ICE) maintenance and highly specialized electric vehicle (EV) architectures. As the average age of global vehicle fleets increases, the dependency on high-performance aftermarket maintenance chemicals escalates to optimize combustion efficiency and control exhaust degradation. Concurrently, the global transition to high-voltage electric mobility creates an entirely new ecosystem of demands for complex dielectric fluids, polyurethane battery adhesives, and water-borne coatings.

Technical Framework and In-Depth Market Dynamics

What Are the Key Factors Driving The Market?

-

Accelerated Urbanization and Fleet Utilization: Expanding urban populations in emerging economies elevate the operational reliance on passenger and commercial transport. Higher urban thermal effects and gridlock stop-and-go driving mandate advanced, biodegradable fluid formulations that prevent accelerated oxidation and soot deposits.

-

Electrification and E-Mobility Architecture: The rapid deployment of Electric Vehicles (EVs) creates massive structural demands for specialized cooling media. Single-circuit thermal fluids and high-purity battery binders are vital to prevent thermal runaway while supporting rapid-charging capacities.

-

Lightweight Performance Engineering: Traditional mechanical fasteners are increasingly replaced by high-strength structural adhesives to join dissimilar materials like carbon fiber, aluminum, and high-strength steel, maximizing weight reduction without degrading vehicle crashworthiness.

What Are the Primary Restraints Limiting Expansion?

-

High Operational and Feedstock Costs: Transitioning to green chemistry, bio-derived synthetic base oils, and low-VOC formulations demands specialized manufacturing inputs. The elevated cost of sourcing non-petroleum chemical precursors limits the gross margins for medium-scale manufacturers trying to achieve rapid economies of scale.

What Is the Core Future Opportunity in the Sector?

-

Advanced Battery Materials & Circular Economy Investments: Tremendous capital is flowing into engineering specialized fire-retardant intumescent materials, dielectric cooling fluids, and silicon-anode stabilizers. Furthermore, the evolution of hydrometallurgical recycling agents designed to extract and recover high-purity battery electrolytes creates an entirely new circular sub-market aligned with stringent ESG directives.

Key Market Trends & Advanced Technological Shifts

What Is the Impact of AI and Digital Twins in Automotive Chemistry?

Computational Fluid Dynamics (CFD) and AI-driven high-throughput screening have revolutionized molecular formulation. Researchers now utilize machine learning algorithms to map and predict the chemical degradation rate, oxidation resistance, and thermal profiles of smart polymers and synthetic lubricants under high shear stress.

Additionally, automated laboratory robotics are deployed to refine electrolytic purity levels in EV cooling materials, removing manual trial-and-error limitations. AI models are also widely integrated into green synthesis pathways, minimizing catalytic energy consumption and toxic byproducts during industrial manufacturing runs.

What Is the Key Strategy Behind the Shift Toward Sustainability?

The industry is experiencing a profound transition toward green chemistry. Original Equipment Manufacturers (OEMs) and aftermarket players are co-developing low-VOC (volatile organic compound) coatings, bio-based lubricants, and eco-friendly aqueous binders. These formulations eliminate hazardous heavy metals and persistent PFAS chemicals, ensuring compliance with strict environmental global frameworks.

Segmental Architecture & Dominant Market Shares

Which Segment Accounted for the Largest Market Share by Product Type?

The Lubricants segment dominated the industry, capturing 38% of the global market share in 2025. This extensive dominance is sustained by the critical requirement for friction reduction, mechanical integrity, and heat dissipation across engine oils, brake fluids, and gear systems. The segment is currently evolving toward ultra-low viscosity synthetic e-fluids that possess high copper compatibility and reduced internal drag coefficients.

-

Adhesives & Sealants (10% Share in 2025): Projected to expand at the fastest product CAGR of 6.2%. This growth is directly accelerated by vehicle lightweighting and structural bonding in battery cell arrays where insulation and noise, vibration, and harshness (NVH) damping are mandatory.

-

Fuels & Fuel Additives (16% Share in 2025): Serving as a critical medium for maintaining fuel injector hygiene and supporting advanced bio-ethanol or renewable diesel blends.

Vehicle Type and Application Segments

-

Passenger Vehicles (52% Dominant Share in 2025): Driven by massive consumer car ownership and structured preventative maintenance cycles that utilize high-mileage lubricants and cabin-safe interior protectants.

-

Electric Vehicles (20% Share in 2025): Positioned as the fastest-growing vehicle cohort with a 7.8% CAGR, creating non-negotiable requirements for structural EMI shielding, potting compounds, and dielectric thermal interface systems.

-

Engine Application (34% Dominant Share in 2025): Driven by internal combustion downsizings, turbocharging architectures, and the subsequent need for high oxidation-resistant synthetic lubricants.

Supply Chain and Distribution Overview

The Aftermarket segment commanded 58% of the distribution channel share in 2025, growing at an expected 6.1% CAGR. This dominance is fueled by independent service centers and e-commerce networks delivering high-margin fuel system cleaners, protective coatings, and recurring maintenance flushes. The remaining 42% is held by the OEM assembly pipeline.

From a formulation perspective, Organic Chemicals dominated with a 62% share in 2025, utilizing carbon-based polyalphaolefins and synthetic esters. Meanwhile, Inorganic Chemicals (38% share) are rising rapidly at a 5.8% CAGR due to the integration of lithium-salt electrolytes and ceramic protective films.

| Attribute | 2025 (Base Year) | 2026 (Forecast Start) | 2035 (Target Forecast) | Sector CAGR (2026–2035) |

| Market Value (USD) | $46.85 Billion | $49.54 Billion | $81.94 Billion | 5.75% |

| Market Volume (Tons) | 19.45 Million | 20.45 Million | 32.14 Million | 5.15% |

| Avg. Mfg Price / Ton | $1,930 | — | — | Pricing CAGR: |

| Avg. Selling Price / Ton | $2,550 | — | — | 3.11% |

Regional Analysis: Geographic Consolidation

How Did Asia-Pacific Dominate the Automotive Chemicals Market?

The Asia-Pacific region stood as the definitive global anchor, holding a massive 44% market share in 2025 with a valuation estimated at USD 20.61 billion, and is projected to expand to USD 36.46 billion by 2035. It is also the fastest-expanding region, registering an impressive 6.5% CAGR. The region serves as the epicentre for global vehicle assembly, driven heavily by China’s dominant e-mobility supply chain, massive production capacities for lithium-ion battery binders, and large-scale domestic transition toward water-borne OEM paints.

North American Growth Trends

North America captured 22% of the market share in 2025, moving forward at a steady 5.20% CAGR. The market is strongly characterized by a highly mature aftermarket infrastructure and a rising average vehicle fleet age, which requires premium synthetic formulations, fuel additives, and specialized high-mileage engine care products.

Regulatory Framework: Global Policy Matrix

Regulatory alignment dictates the chemical composition boundaries across major manufacturing geographies:

-

Global Level (GHS, ISO, OECD): Enforces global standardization of safety data sheets (SDS) and establishes toxicity ceilings for bulk polymers and industrial chemical additives.

-

North America (EPA, CARB, TSCA): Mandates strict VOC limits on brake systems, non-chlorinated solvent usage, and structural fluids optimizing CAFE mileage metrics.

-

Asia-Pacific (GB Standard, METI, Bharat Stage): Enforces dielectric safety thresholds for EV cooling materials, mandates New Energy Vehicle (NEV) battery recycling, and accelerates the transition to green water-borne coatings.

-

Europe (REACH, CLP, Euro 7): Drives the complete elimination of PFAS (“forever chemicals”) in industrial lubricants, prioritizing ultra-low toxicity coolants and absolute chemical purity.

Competitive Landscape & Top Companies

The strategic environment features intense consolidation among chemical conglomerates focusing on high-margin EV fluids and bio-derived polymer portfolios. Below is an architectural overview of three leading market participants:

1. BASF SE

-

About: Headquartered in Ludwigshafen, Germany, BASF is one of the world’s largest chemical corporations, focusing deeply on sustainable surface technologies, performance materials, and custom automotive coatings.

-

Products: Glysantin® coolants, water-borne refinish coatings, structural polyurethane adhesives, fuel additives, and customized engineering plastics.

-

Market Capitalization: Approximately EUR 46.37 Billion (as of May 2026).

2. ExxonMobil Corporation

-

About: An American multinational oil and gas corporation, ExxonMobil is a dominant upstream and downstream producer of high-purity synthetic base stocks, hydrocarbon solvents, and advanced polyalphaolefins (PAOs) for the lubricant market.

-

Products: Mobil 1™ synthetic lubricants, SpectraSyn™ PAO base stocks, specialized automotive resins, and advanced functional fluids for electric drivetrains.

-

Market Capitalization: Approximately USD 642.14 Billion (as of May 2026).

3. Dow Inc.

-

About: A global leader in materials science, Dow delivers highly advanced silicone, acrylic, and polyurethane solutions tailored for structural bonding, crash durability, and electronic component insulation within the automotive sector.

-

Products: DOWSIL™ silicone sealants, Betaseal™ structural adhesives, Voranol™ polyurethane systems for acoustic insulation, and thermal management gels.

-

Market Capitalization: Approximately USD 25.96 Billion (as of May 2026).

What Is the Status of Recent Strategic Market Developments?

-

January 2026: ProLogium entered into a strategic collaboration with Darfon Energy Tech at CES 2026. The alliance focuses on rolling out solid-state battery solutions engineered for light electric vehicles and e-bikes to optimize charging speeds and overall thermal efficiency.

-

December 2025: NEXTCHEM, a key subsidiary of MAIRE, executed a definitive agreement to acquire the Ballestra Group. This strategic maneuver integrates Ballestra’s expertise in advanced fluorine-based materials for lithium-ion batteries, scaling NEXTCHEM’s global presence within specialty battery chemicals and supporting global energy transition mandates.

Future Horizon: The Strategic Outlook

The future of the automotive chemicals market will be defined by an irreversible convergence of material circularity, high-voltage vehicle electrical safety, and AI-accelerated molecular discovery. As internal combustion applications gradually plateau, the financial center of gravity will shift decisively toward smart functional fluids and composite-bonding adhesives.

Chemical organizations that prioritize high thermal stability, non-toxic formulations, and localized onshoring of critical battery chemistries will capture long-term supply agreements with global automakers. The upcoming decade will reward chemical precision over volume, cementing these specialized formulations as foundational elements of autonomous, electric, and sustainable transport networks.

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Email: [email protected]

Leave a Reply