Executive Summary

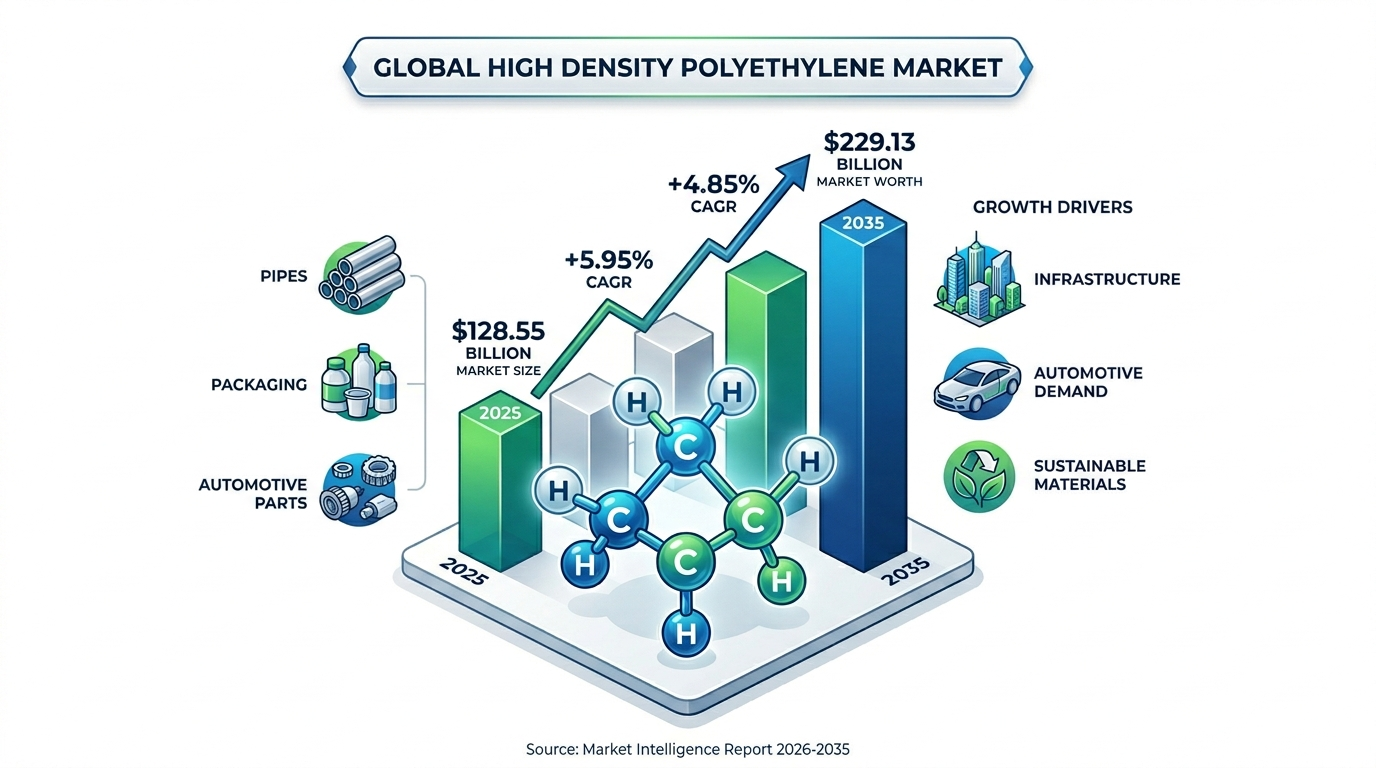

The global High Density Polyethylene (HDPE) market is undergoing a structural transition driven by macro-economic infrastructure investments, evolving packaging demands, and regulatory mandates on material circularity. Valued at USD 128.55 billion in 2025, the global market value is projected to scale to USD 229.13 billion by 2035. This trajectory represents a compound annual growth rate (CAGR) of 5.95% from 2026 to 2035. Linear interpolation of this data places the projected market value at approximately USD 178.78 billion by 2032.

In terms of physical volume, demand is expected to expand from 61.25 million tons in 2025 to 98.35 million tons by 2035, yielding a volume-based CAGR of 4.85%. This slight divergence between value and volume compound annual growth rates highlights a shifting market mix toward high-performance, bimodal, and certified recycled resin grades (rHDPE), which command a clear pricing premium over standard commodity resins.

Market Overview

What is the High Density Polyethylene market?

The High Density Polyethylene market comprises the global manufacturing, distribution, and commercial conversion of thermoplastic dense ethylene polymers characterized by a density range of $0.941\text{ to }0.967\text{ g/cm}^3$. Known for its minimal branching structure, HDPE exhibits superior tensile strength, high chemical resistance, and excellent environmental stress-crack resistance (ESCR).

The market operates as a vital pillar within the broader petrochemical sector, bridging raw material refining (cracking of naphtha and natural gas liquids) with essential downstream industrial verticals. Resin producers supply materials across diverse processing technologies, primary among them being extrusion blow molding, injection molding, sheet and film extrusion, and pipe extrusion.

Market Dynamics & Key Drivers

What are the key factors driving the market?

Substantial infrastructure investments in emerging economies serve as the primary catalyst for the global expansion of the HDPE market. Rapid urbanization and state-backed utility modernization initiatives require the replacement of legacy metal and concrete water networks with corrosion-resistant, flexible HDPE pipe systems capable of a 100-year operational lifespan.

Concurrently, the automotive industry’s pursuit of vehicle lightweighting to optimize fuel efficiency and support electric vehicle (EV) battery ranges has boosted demand for complex, blow-molded HDPE fuel tanks, structural components, and fluid reservoirs. Furthermore, the global consumer goods sector is shifting heavily toward lightweight, durable materials, ensuring steady demand for structural packaging across both food-grade and industrial applications.

Key Market Trends

What are the primary market trends?

The most significant trend reshaping the industry is the commercial scale-up of advanced recycling technologies, specifically chemical recycling (pyrolysis), alongside mechanical processing to produce high-purity rHDPE. Major polymer producers are forming joint ventures with municipal waste sorting entities to secure clean post-consumer resin streams, matching a structural push by global brands to hit recycled content targets.

Technologically, manufacturing setups are moving away from traditional unimodal resins toward bimodal resin architectures. Bimodal HDPE lines allow processing plants to create thin-walled parts that retain high mechanical toughness and crack resistance, offering a significant economic advantage through material lightweighting.

Market Benefits & Product Importance

Why is this market important, and what are the benefits of using HDPE?

HDPE is a vital material in industrial design due to its balance of structural strength, low weight, chemical resistance, and long-term cost savings. Unlike traditional metals, it is entirely immune to electrochemical corrosion and biological fouling, eliminating the need for cathodic protection or anti-corrosive chemical coatings.

Its low density cuts logistics costs and reduces greenhouse gas emissions during transport compared to glass or metal packaging. Additionally, its high thermal stability and ease of thermoplastic processing make it highly recyclable. This allows it to easily re-enter the industrial value chain, supporting circular economy initiatives.

Recent Government Initiatives

What recent government initiatives are impacting the market?

Regulatory directives worldwide are changing how virgin and recycled HDPE are used. In Europe, the Packaging and Packaging Waste Regulation (PPWR) mandates strict post-consumer recycled targets for consumer plastic packaging by 2030, putting pressure on suppliers to stabilize the supply chain for food-contact rHDPE.

In the United States, infrastructure funding through the Infrastructure Investment and Jobs Act (IIJA) has allocated substantial capital directly to drinking water and wastewater infrastructure renewals, boosting domestic procurement of certified HDPE pressure pipes. Meanwhile, across the Asia-Pacific region, strict bans on specific non-recyclable single-use plastics are forcing a shift toward highly recyclable, rigid HDPE formats.

Market Segmentation Analysis

Which segment accounted for the largest market share?

The packaging segment dominated the market share in 2025, accounting for over 35% of global volume demand. This leading position is driven by high consumption rates in household care, cosmetic containers, food-grade milk and juice jugs, and industrial drums. Within processing methods, blow molding leads the market, driven by its efficiency in producing high-volume, hollow components.

From a regional perspective, the Asia-Pacific region holds the largest market share, commanding roughly 46% of global demand. This dominance is supported by the heavy concentration of chemical processing infrastructure and manufacturing capacity in China, alongside rapid urbanization and infrastructure investments across India and Southeast Asia.

Strategic Data Reference

The following table provides a structured breakdown of the forecast metrics, highlighting the distinct performance pathways between overall value expansion and true physical consumption volumes.

Leave a Reply