Market Overview

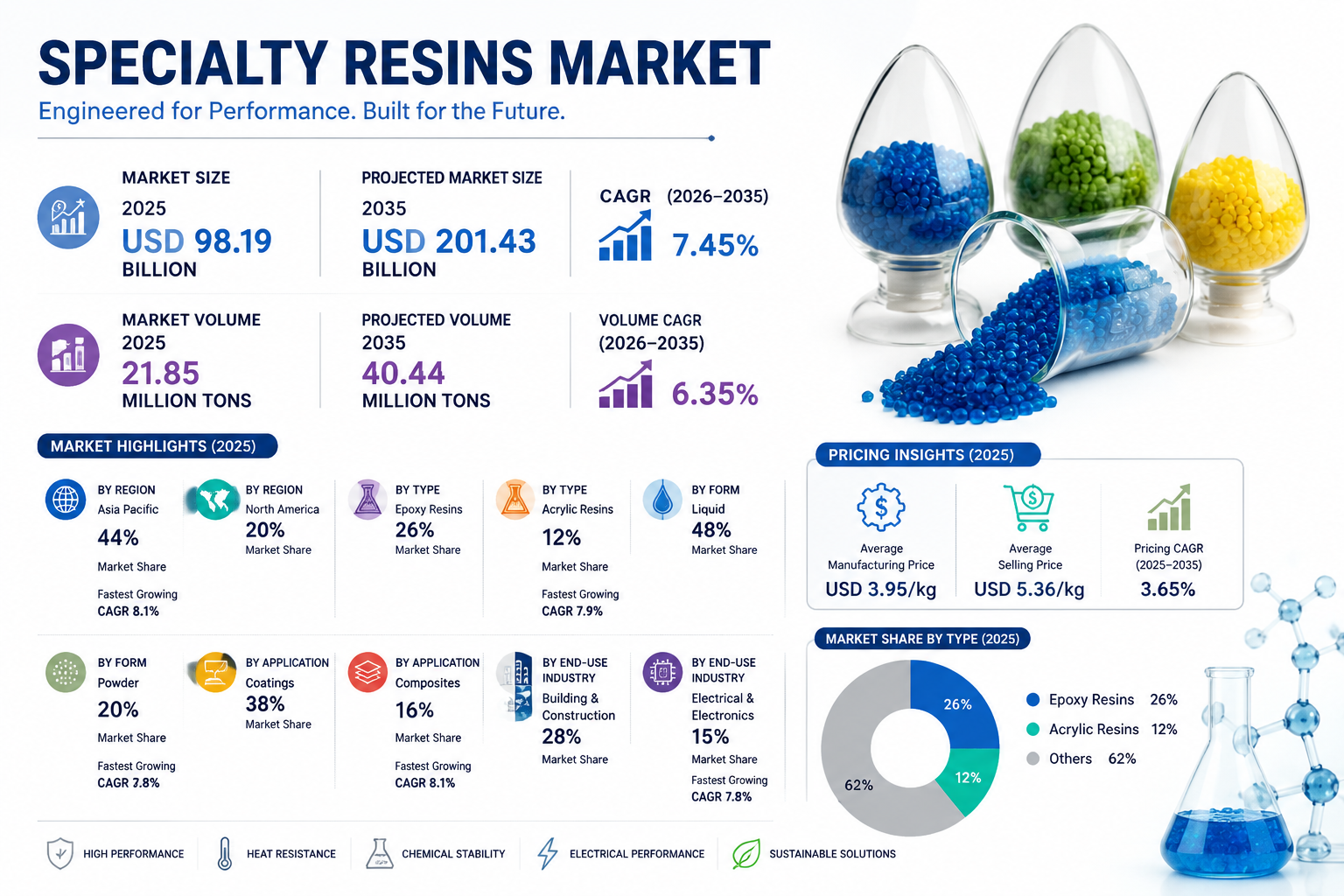

The Global Specialty Resins Market has emerged as one of the most dynamic segments in advanced materials, driven by rising demand for tailored, high‑performance polymer solutions across multiple end‑use industries. In 2025, the market was valued at USD 98.19 billion and is projected to reach USD 201.43 billion by 2035, reflecting a Compound Annual Growth Rate (CAGR) of 7.45 % from 2026 to 2035. In volume terms, the industry is expected to grow from 21.85 million tons in 2025 to 40.44 million tons by 2035, registering a 6.35 % CAGR over the same period.

Specialty resins are engineered polymers developed for specific performance characteristics — including heat resistance, chemical stability, electrical insulation, and mechanical strength — making them invaluable in demanding applications. They are widely used in adhesives, coatings, composites, electronics, and advanced composites. Continued technological innovation and increasing requirements for sustainability and performance are key drivers for growth.

| Year | Market Value (USD Billion) | Volume (Million Tons) |

|---|---|---|

| 2025 | 98.19 | 21.85 |

| 2030 | 140.00 (estimate) | 30.00 |

| 2035 | 201.43 | 40.44 |

Market Dynamics

Growth Drivers

• Shift Toward Specialty Applications: Industries such as automotive, electronics, construction, and aerospace increasingly require materials with precise performance criteria, fueling demand for customized resin solutions.

• Technological Innovation: Continuous R&D in polymer chemistry enables development of resins with enhanced thermal, mechanical, and barrier properties.

• Sustainability Focus: Manufacturers are investing in bio‑based and recyclable resin technologies to meet environmental regulations and corporate sustainability objectives.

Challenges

• Raw Material Price Volatility: Fluctuating petrochemical feedstock prices impact production costs and pricing stability.

• Regulatory Compliance: Stricter environmental and safety regulations require significant investments in cleaner technologies and reformulation.

• Competition from Alternative Materials: Emerging material families (e.g., bio‑polymers) present competitive pressures in certain applications.

Opportunities

• Growth in emerging economies, particularly Asia Pacific, with strong industrial expansion and infrastructure development.

• Increasing adoption of specialty resins in high‑growth applications such as electric vehicles, smart electronics, and renewable energy composites.

Market Insights

Regional Insights

• Asia Pacific dominated the market in 2025 with a 44 % share, attributed to rapid industrial growth, infrastructure development, and strong manufacturing bases in China, India, Japan, and Southeast Asia.

• North America held approximately 20 % market share in 2025, supported by advanced technology adoption and steady demand in automotive and aerospace sectors.

• Europe continues to show stable growth due to sustainability initiatives and advanced polymers adoption.

Pricing Outlook

• The average manufacturing price in 2025 was USD 3.95/kg, with the average selling price around USD 5.36/kg, indicating strong value capture through specialty formulations.

• The pricing CAGR from 2025 to 2035 is projected at 3.65 % — a reflection of ongoing improvements in high‑value product offerings.

Market Segments

By Resin Type

• Epoxy Resins: Largest segment with ~26 % share in 2025; widely used for coatings, adhesives, and composites.

• Acrylic Resins: ~12 % share in 2025; fastest‑growing with ~7.9 % CAGR due to demand in coatings and high‑performance adhesives.

• Other types include polyurethane, phenolic, silicone, and specialty thermoplastic resin families.

| Resin Type | 2025 Share | CAGR (2026‑2035) |

|---|---|---|

| Epoxy | 26% | 6.5% |

| Acrylic | 12% | 7.9% |

| Others | 62% | 6.0% |

By Form

• Liquid Resins: Dominated the market with ~48 % share in 2025.

• Powder Resins: Held ~20 % share, with projected high growth (~7.8 % CAGR) driven by powder coatings and industrial applications.

By Application

• Coatings: Largest segment (~38 % share in 2025), used extensively in automotive, construction, and industrial finishes.

• Composites: ~16 % share in 2025; fastest growth (~8.1 % CAGR) due to use in lightweight, high‑strength components.

By End‑Use Industry

• Building and Construction: Held the largest share (~28 %) in 2025, driven by increased demand for durable, weather‑resistant materials.

• Electrical and Electronics: ~15 % share in 2025; fastest growth (~7.8 % CAGR) due to increased electronics production and performance requirements.

Top Companies in the Specialty Resins Market

Below are some of the leading global companies shaping the specialty resins landscape, including company overview, key product offerings, and market capitalization (as of May 2026):

BASF SE

About: BASF SE is the world’s largest chemical producer headquartered in Germany, offering a broad portfolio of specialty resins and performance materials for multiple industries.

Products: Epoxy, acrylic, polyurethane, and engineered resin systems for coatings, adhesives, and composites.

Market Cap: ~USD 46.5 billion.

Dow Inc.

About: Dow Inc. is a leading American multinational chemical company focused on performance materials and specialty chemicals.

Products: Epoxy and acrylic resins, specialized polyurethanes, and engineered polymers for construction, automotive, and packaging industries.

Market Cap: Publicly traded; large diversified chemical market cap (precise figure subject to daily change).

Evonik Industries AG

About: German specialty chemical company with strong expertise in functional polymers, additives, and specialty resins.

Products: Performance resin systems for coatings, adhesives, composites, and high‑technology applications.

Market Cap: Publicly traded; strong financials with €14.1 billion revenue base in 2025.

Covestro AG

About: Covestro is a German materials manufacturer specializing in advanced polymers and resin precursors.

Products: Polyurethane and polycarbonate resins, coatings additives, and engineered polymer materials.

Market Cap: ~USD 14.31 billion.

Huntsman Corporation

About: Huntsman provides specialty chemical solutions, including advanced thermosets and custom resin technologies, globally.

Products: Epoxy, phenolic, and other specialty resins for adhesives, coatings, and composites.

Recent Developments in Specialty Resins

• In 2025, major chemical companies expanded partnerships and product portfolios to address emerging applications in automotive and electronics sectors. Recent initiatives focus on sustainable resin formulations, driven by regulatory and customer demand.

• Companies are emphasizing capacity expansions, including advanced epoxy production units in Asia Pacific and Europe, to meet projected demand growth.

• Strategic divestments and restructuring for performance focus — including BASF’s portfolio optimization — signal industry shifts toward core specialty materials segments.

Industry Trends

• Bio‑Based and Recycled Resins: Growing investment in sustainable resin alternatives to traditional petrochemical‑derived materials.

• High‑Performance Composites Adoption: Increasing use in aerospace, automotive, and renewable energy applications.

• Shift to Lightweight Materials: Driven by automotive weight reduction and fuel efficiency mandates.

Frequently Asked Questions

- What defines specialty resins in the chemical industry market?

Specialty resins are high‑performance polymers engineered for specific functional properties such as heat resistance, chemical stability, electrical insulation, and mechanical strength — tailored for advanced applications across industries. - Which regions dominate the global specialty resins market?

Asia Pacific currently leads with the highest market share and fastest growth rate, followed by North America and Europe, driven by industrial expansion and demand for advanced materials. - What are the key growth drivers for specialty resins?

Key drivers include increased demand for high‑performance materials in automotive, electronics, coatings, sustainable material trends, and demand for customized resin solutions. - How does sustainability impact specialty resin development?

Sustainability drives R&D toward bio‑based resins, recyclable systems, and low‑emission formulations responding to regulatory pressure and customer preferences. - Which segments offer the fastest growth opportunities?

Fastest growth is expected in acrylic resins, powder forms, composites, and specialty applications such as electrical and electronics industries due to performance requirements.

Leave a Reply