The U.S. mining sector is currently navigating a period of intensive modernization, where the efficiency of mineral extraction is no longer just a technical goal but a geopolitical necessity. As domestic ore grades decline and the demand for critical minerals—essential for the energy transition—surges, the role of froth flotation chemicals has become paramount. This report examines the evolution of the U.S. market, focusing on how chemical innovation is enabling the recovery of high-value minerals from increasingly complex geological deposits.

Executive Summary

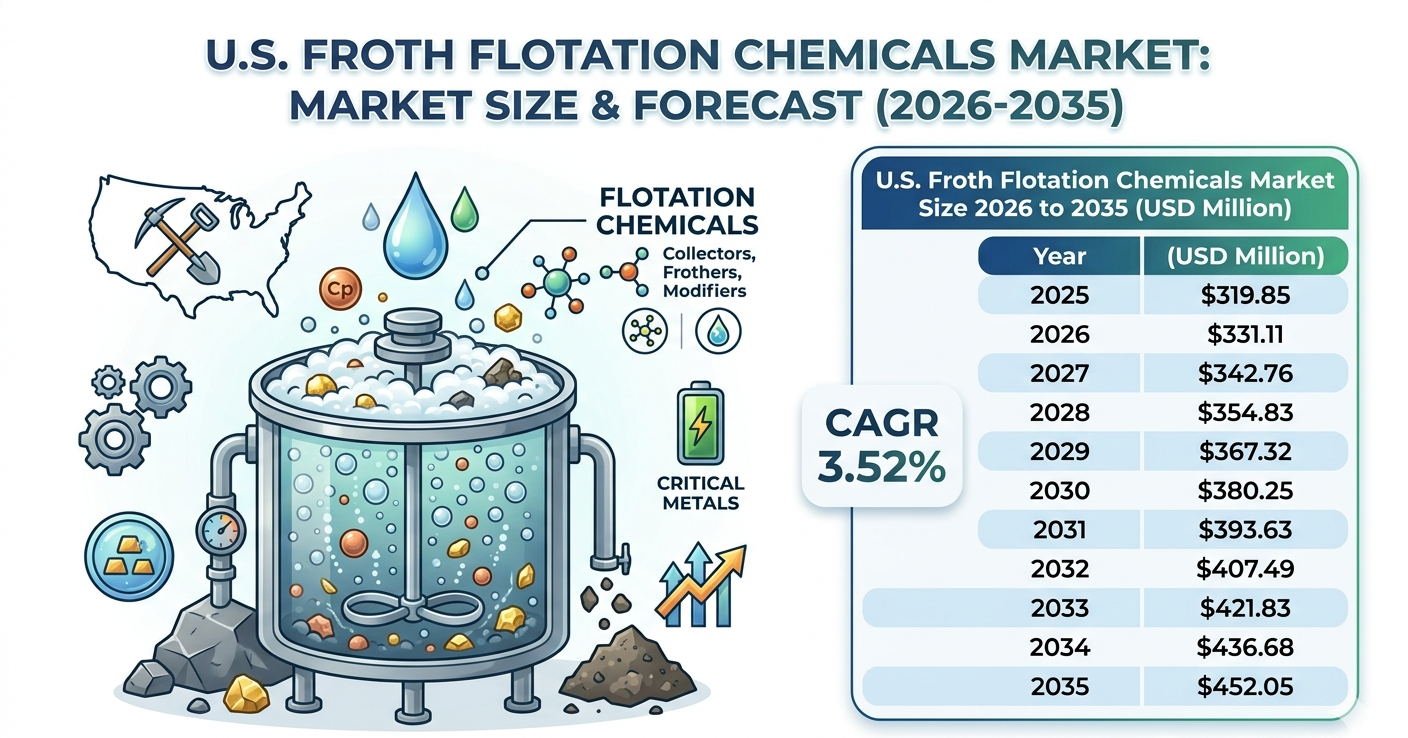

The U.S. froth flotation chemicals market is projected to witness a steady expansion, primarily fueled by the domestic push for mineral independence and advanced ore beneficiation techniques. Valued at USD 319.85 million in 2025, the market is estimated to reach USD 331.11 million in 2026. By 2035, the market is projected to grow to USD 452.05 million, progressing at a CAGR of 3.52% from 2026 to 2035. While the growth rate reflects a mature market, the value is increasingly shifting toward high-performance, site-specific specialty chemicals that offer superior recovery rates under challenging conditions.

Market Overview: Why Is This Market Important?

Froth flotation chemicals are the critical “selective agents” that allow the mining industry to separate valuable minerals from gangue (waste rock). In an era where “easy” ore deposits have largely been depleted, the U.S. mining industry relies on these chemicals to maintain the economic viability of domestic mines. Their importance is heightened by the U.S. strategy to secure domestic supply chains for copper, molybdenum, and gold, as well as critical battery metals. Without sophisticated collectors, frothers, and modifiers, the processing of low-grade ores would be energy-prohibitive and environmentally unsustainable.

Market Dynamics: What Are the Key Factors Driving the Market?

The primary driver for the U.S. market is the rising demand for copper and rare earth elements necessitated by the electrification of the economy. Copper mining, in particular, is a heavy consumer of flotation chemicals, and with several major U.S. projects seeking to expand capacity, the demand for specialized collectors is intensifying. Additionally, the industry is seeing a significant shift toward “Green Mining.” Environmental regulations regarding tailings management and water discharge are forcing operators to move away from traditional xanthates toward more biodegradable and less toxic alternatives.

Another critical factor is the integration of digitalization and automation in mineral processing. Modern flotation circuits now use real-time sensors to adjust chemical dosages instantly. This “smart dosing” requires chemicals with high consistency and predictable performance profiles. Furthermore, the trend of processing “complex ores”—where multiple minerals are interlocked at a microscopic scale—is driving the development of bespoke chemical “cocktails” tailored to specific mine sites, creating a more high-margin, service-oriented market for chemical suppliers.

Key Segments & Trends: Which Segment Accounted for the Largest Share?

The market is segmented by chemical type into Collectors, Frothers, Modifiers, and Depressants. Collectors currently hold the largest market share, as they are the primary agents responsible for making the target mineral hydrophobic. However, the Modifiers segment is seeing rapid growth due to the need to adjust pH levels and deactivate unwanted minerals in complex ore bodies. By application, the Base Metals segment (Copper, Lead, Zinc) continues to dominate U.S. demand, followed closely by precious metals recovery.

A significant technological shift is the move toward synergistic collector blends. Rather than relying on a single chemical, operators are increasingly using blends that combine the high power of traditional collectors with the high selectivity of newer, synthetic molecules. Regional growth is largely concentrated in the Southwestern U.S. (Arizona, Nevada, and Utah), which serves as the heart of the nation’s copper and gold production. Emerging trends also indicate a rising interest in flotation chemicals for the recycling of electronic waste, where flotation is used to recover precious metals from crushed circuit boards.

Market Recent Government Initiatives: What Is Shaping the Regulatory Landscape?

The U.S. government has taken a proactive stance in securing the mineral supply chain, which directly impacts the flotation chemicals sector. The “American Critical Minerals Strategy” and the Inflation Reduction Act (IRA) provide significant incentives for domestic mineral production. These initiatives are designed to reduce reliance on foreign entities for materials like lithium and cobalt. Furthermore, the U.S. Department of Energy (DOE) has allocated substantial funding for R&D into more efficient mineral extraction technologies, including “next-generation” flotation reagents that reduce water consumption.

Environmental oversight from the EPA and the Bureau of Land Management (BLM) is also steering the market. Recent guidelines emphasize the reduction of hazardous waste in mine tailings. This has created a “regulatory push” for chemical manufacturers to phase out certain legacy chemicals in favor of surfactants that are more easily neutralized in tailings ponds. These initiatives are essentially transforming the flotation chemical market from a commodity-driven sector into a compliance-and-innovation-driven industry.

Data Presentation: Market Size and Projected Growth

The following data highlights the consistent value appreciation of the U.S. market.

[Insert Data Table 1: U.S. Froth Flotation Chemicals Market Size (2025–2035) in USD Million]

-

2025: $319.85 M

-

2028: $354.83 M

-

2032: $407.49 M

-

2035: $452.05 M

Recent developments in the product space include the introduction of low-sulfur frothers that minimize odor and toxicity issues in underground mining operations, and polymeric depressants that offer higher precision in separating talc and carbonaceous matter from valuable ores.

Competitive Landscape: Top Companies and Strategic Movements

The U.S. competitive environment is shifting from a purely product-based competition to a “service-plus-chemistry” model, where top firms provide on-site technical support to optimize recovery.

1. BASF SE

-

About: A global leader in chemical manufacturing with a specialized division for mineral processing.

-

Products: Lupromin™ collectors and specialized frothers.

-

Market Cap: Approximately USD 43 Billion.

-

Strategic Move: BASF has been focusing on its “Sustainable Solution Steering” method to provide flotation reagents that minimize environmental footprints while maximizing recovery in U.S. copper mines.

2. Clariant AG

-

About: A Swiss specialty chemical giant with a strong “Mining Solutions” hub in North America.

-

Products: FLOTIGAM® collectors and FLOTANOL® frothers.

-

Market Cap: Approximately USD 4.8 Billion.

-

Strategic Move: Clariant recently expanded its R&D capabilities in the U.S. to focus specifically on tailor-made reagents for the recovering of battery-grade minerals.

3. Arkema (ArrMaz)

-

About: Arkema acquired ArrMaz to strengthen its position in specialty surfactants for the mining and infrastructure markets.

-

Products: Custo™ line of collectors and frothers.

-

Market Cap: Approximately USD 7.5 Billion (Arkema).

-

Strategic Move: Leveraging its deep expertise in phosphate mining to expand into the U.S. industrial minerals and base metals flotation markets.

4. Solvay S.A.

-

About: A major player in high-performance specialty chemicals with a legacy in mining reagents.

-

Products: AEROPHINE® and AERO® promoters.

-

Market Cap: Approximately USD 3.8 Billion (Solvay).

-

Strategic Move: Concentrating on its “AERO” series to provide high-selectivity solutions for complex polymetallic ores in the Western U.S.

Conclusion: What Is the Future of the Market?

The future of the U.S. froth flotation chemicals market lies in the intersection of molecular biology and chemical engineering. We anticipate the rise of “bio-flotation” agents—microbial-derived surfactants that offer near-perfect selectivity and zero environmental toxicity. As the U.S. continues to revitalize its domestic mining infrastructure, the demand for chemicals that can operate in “closed-loop” water systems will become the new industry standard. For chemical manufacturers, the path forward is clear: success will be defined by the ability to provide site-specific, sustainable, and digitally-integrated chemical solutions that turn low-grade waste into high-value resources.

Inquiries: sales@towardschemandmaterials.com | Stay ahead of the curve with our specialized mineral processing research.

Contact Us https://www.towardschemandmaterials.com/contact-us

About Us

Towards Chem and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Web: https://www.towardschemandmaterials.com/

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/?viewAsMember=true

Leave a Reply