The Asia Pacific specialty chemicals landscape is undergoing a structural realignment, shifting from a high-volume manufacturing hub to a high-value innovation center. As global supply chains diversify and domestic demand for high-performance materials surges in sectors like electronics, electric vehicles (EVs), and advanced healthcare, the regional market is poised for a decade of sophisticated growth.

Executive Summary

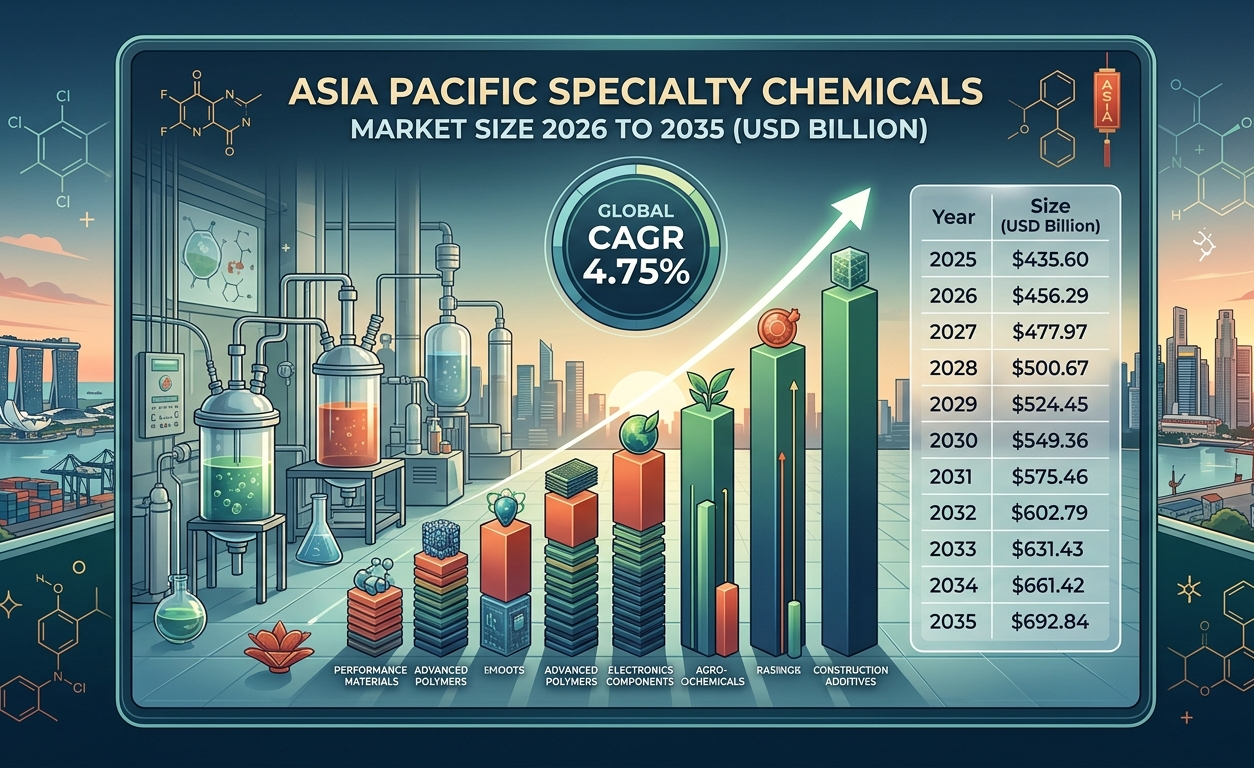

The Asia Pacific specialty chemicals market is entering a pivotal expansion phase. Valued at USD 435.60 billion in 2025, the sector is estimated to grow to USD 456.29 billion in 2026. By 2035, the market is projected to reach USD 692.84 billion, accelerating at a consistent CAGR of 4.75% from 2026 to 2035. This growth is underpinned by rapid industrialization in emerging economies and a significant shift toward sustainable, “green” chemical solutions.

Market Overview: Why Is This Market Historically Significant?

Specialty chemicals, often referred to as performance chemicals, are valued for what they do rather than their molecular composition. In the Asia Pacific region, this sector acts as the lifeblood of industrial modernization. Unlike commodity chemicals, specialty products—such as electronic chemicals, agrochemicals, and construction polymers—are low-volume but high-margin, requiring intense R&D and deep technical integration with end-user applications.

The importance of this market lies in its role as an “enabler.” For instance, the transition to 5G technology and the miniaturization of semiconductors in South Korea and Taiwan would be impossible without high-purity electronic gases and photoresists. Similarly, India’s push for food security relies heavily on advanced crop protection chemicals. This region has transitioned from a mere consumer to a dominant producer, with China now commanding a significant portion of global output, forcing a shift in global competitive dynamics and trade flows.

Market Dynamics: What Are the Key Factors Driving the Market?

The primary engine of the APAC specialty chemicals market is the relentless expansion of the middle class and the subsequent demand for sophisticated end-products. The automotive industry’s pivot toward electrification is creating a massive vacuum for specialty polymers and battery chemicals. Furthermore, the “China Plus One” strategy is encouraging significant investment in Southeast Asia and India, diversifying the manufacturing base and creating new clusters of specialty chemical production.

Digitalization is another critical driver. The integration of AI and machine learning in chemical formulation is shortening the “lab-to-market” cycle, allowing companies to respond more rapidly to niche consumer demands. We are also seeing a “premiumization” trend in the personal care and home care sectors across Southeast Asia, where consumers are increasingly opting for active ingredients over basic formulations. This shift mandates a higher concentration of specialty additives, surfactants, and fragrance chemicals, ensuring a steady demand pipeline despite global economic fluctuations.

What Are the Key Market Trends?

The most dominant trend is the “Green Decarbonization” of the chemical value chain. Regulatory pressures and ESG mandates are forcing manufacturers to adopt bio-based feedstocks and circular economy models. We are seeing a surge in bio-plastics and biodegradable surfactants, particularly in Japan and Australia. Additionally, the localized production of high-performance electronic chemicals is a strategic priority for regional governments looking to secure their tech supply chains.

Segment Analysis: Which Segment Accounted for the Largest Market Share?

The Agrochemicals and Electronic Chemicals segments currently dominate the regional landscape. Agrochemicals lead in terms of volume, driven by the massive agricultural sectors of India, China, and Vietnam. However, Electronic Chemicals is the fastest-growing sub-segment by value. With the Asia Pacific region hosting the world’s largest semiconductor foundries, the demand for high-purity specialty gases, wet chemicals, and CMP slurries is insatiable.

Construction chemicals also represent a significant share, fueled by massive infrastructure projects like Indonesia’s new capital city and India’s Gati Shakti initiative. These projects require advanced admixtures, sealants, and water-proofing compounds that can withstand diverse and extreme climatic conditions. The trend toward smart cities and green buildings is further pushing the demand for high-performance specialty coatings and insulation materials, marking a shift toward longevity and energy efficiency in urban planning.

What Is the Market’s Future?

The future of the APAC specialty chemicals market will be defined by “Molecular Tailoring.” Instead of selling products, companies will increasingly sell “solutions”—collaborating directly with OEMs to develop materials that meet hyper-specific performance criteria. We anticipate a surge in the adoption of Flow Chemistry and modular manufacturing, which allows for safer, more efficient production of hazardous specialty intermediates.

Furthermore, as the region moves toward its net-zero goals, the specialty chemicals sector will become the provider of the “hardware” for the energy transition. This includes advanced membranes for hydrogen fuel cells, specialized coatings for wind turbine blades, and high-efficiency thermal interface materials for EV batteries. The convergence of biotechnology and traditional chemistry will also lead to the rise of bio-manufactured specialty ingredients, potentially disrupting traditional petroleum-based incumbents.

What Are the Market’s Recent Government Initiatives?

Governments across the APAC region are aggressively incentivizing domestic specialty chemical production to reduce import dependency and foster innovation.

-

India: The Production Linked Incentive (PLI) scheme for pharmaceuticals and advanced chemistry cell (ACC) batteries is indirectly boosting the demand for specialty chemical intermediates.

-

China: The “14th Five-Year Plan” focuses on upgrading the chemical industry through high-end new materials and fine chemicals, moving away from low-end bulk production.

-

South Korea: Significant government funding is being directed toward the “K-Sensor” and “K-Semiconductor” strategies, which prioritize the domestic development of 100 core materials, many of which are specialty chemicals.

Competitive Landscape: Top Companies and Strategic Moves

The competitive environment is a mix of global diversified giants and agile regional players who are rapidly scaling their technical capabilities.

1. BASF SE

-

About: The world’s largest chemical producer, with a massive footprint in China and Southeast Asia.

-

Products: Functional materials, performance chemicals, and agricultural solutions.

-

Market Cap: Approximately USD 42 billion.

-

Strategic Move: Recently inaugurated the first plants at its new Verbund site in Zhanjiang, China, focusing on engineering plastics and thermoplastic polyurethanes.

2. Mitsubishi Chemical Group

-

About: A Japanese leader specializing in performance products and industrial materials.

-

Products: Optical films, carbon fibers, and performance polymers.

-

Market Cap: Approximately USD 8.5 billion.

-

Strategic Move: Restructuring its portfolio to focus heavily on specialty materials for the electronics and healthcare sectors.

3. Sumitomo Chemical Co., Ltd.

-

About: A major Japanese player with a strong focus on high-tech materials and life sciences.

-

Products: Photoresists for semiconductors, OLED materials, and crop protection.

-

Market Cap: Approximately USD 4 billion.

-

Strategic Move: Expanding its semiconductor material production capacity in Taiwan and South Korea to meet the surging demand for AI chips.

Recent Developments by Major Companies

Innovation in this sector is currently focused on sustainability and supply chain resilience. For example, SABIC has recently expanded its “TRUCIRCLE” portfolio in Asia, offering certified circular polymers to regional packaging leaders. DIC Corporation has been aggressively acquiring regional specialty coating companies to consolidate its leadership in the inks and adhesives market. We are also seeing a rise in joint ventures, such as the recent collaborations between local Indian firms and Japanese specialty houses to bring advanced fluorochemical technology to the Indian market.

Conclusion: A Forward-Looking Perspective

The Asia Pacific specialty chemicals market is no longer a follower in the global industry; it is now a trendsetter. The next decade will see a transition from “Made in Asia” to “Innovated in Asia.” For investors and stakeholders, the opportunity lies in the intersection of sustainability and digitalization. Companies that can solve the region’s unique challenges—such as water scarcity, food security, and the need for ultra-fast electronics—through specialized chemical engineering will define the market’s leadership through 2035.

Inquiries: [email protected] | Explore our full intelligence reports for deeper regional breakdowns.

Contact Us https://www.towardschemandmaterials.com/contact-us

About Us

Towards Chem and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Web: https://www.towardschemandmaterials.com/

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/?viewAsMember=true

Leave a Reply