The global Sustainable Aviation Fuel (SAF) market is at the cusp of a transformative era, driven by the aviation industry’s urgent and non-negotiable commitment to decarbonization. The latest market analysis reveals a sector poised for explosive, near-unprecedented growth, making it one of the most dynamic segments within the global energy transition landscape.

This in-depth article will provide a comprehensive market overview, explore the powerful dynamics driving this growth, offer key insights into market segmentation, and profile the top companies leading the charge towards a net-zero sky.

Download Sample : https://www.towardschemandmaterials.com/download-sample/6066

Market Overview: A Decade of Hyper-Growth

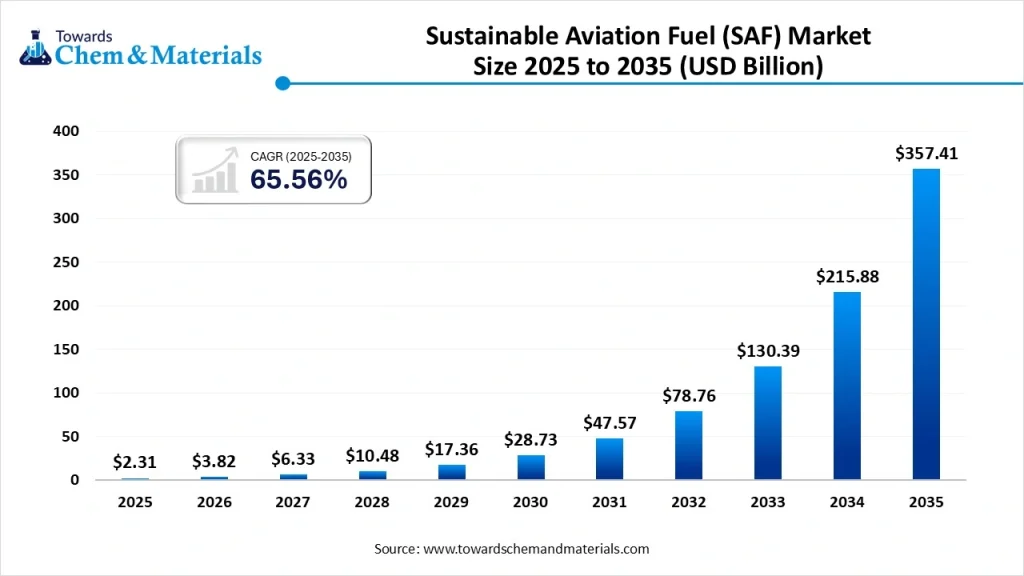

The data paints a clear picture of a market accelerating from niche adoption to mainstream necessity. The global Sustainable Aviation Fuel (SAF) market size is currently calculated at USD 2.31 billion in 2025. This figure is not merely projected to grow; it is forecast to undergo a period of hyper-growth, expanding at a remarkable Compound Annual Growth Rate (CAGR) of 65.56% over the forecast period from 2026 to 2035.

By the end of this forecast window, the market is projected to reach an astounding value of USD 357.41 billion by 2035. This monumental expansion is a direct reflection of aggressive global mandates, increasing corporate sustainability targets, and technological maturation in SAF production.

In 2025, the market dominance by region was clearly established, with North America leading the way, accounting for the largest revenue share of 47.11%. This dominance is heavily fueled by significant government initiatives and supportive regulatory frameworks, such as the US Inflation Reduction Act (IRA), which provides crucial tax credits and incentives for SAF production.

Market Dynamics: Drivers of Decarbonization

The exponential growth of the SAF market is not accidental; it is being propelled by a powerful convergence of regulatory, corporate, and technological forces. Understanding these market dynamics is key to appreciating the sector’s trajectory.

Market Drivers

- Strict Global Regulatory Mandates: The most significant driver is the enforcement of ambitious blending mandates by major economic blocs. The European Union’s ReFuelEU Aviation initiative and similar policies in the US and other regions legally require airlines to incorporate a growing percentage of SAF into their total fuel consumption. These mandates create guaranteed, long-term demand for the product.

- Net-Zero Commitments from Airlines and Corporates: Major international airlines have made public commitments, such as the industry-wide target to achieve net-zero carbon emissions by 2050. Since electrification is not currently viable for long-haul commercial flights, SAF is the primary, certified “drop-in” solution to achieve these goals. This creates a voluntary but powerful demand pull from the commercial aviation segment. Furthermore, large corporations are increasingly demanding SAF for business travel, driving growth in the private aviation application segment.

- Technological Maturity and Certification: Key production pathways like Hydroprocessed Esters and Fatty Acids (HEFA) are fully certified and being rapidly scaled up. Continuous innovation in other pathways, such as Fischer-Tropsch (FT) synthesis and Alcohol-to-Jet (AtJ), is expanding the range of feedstocks that can be used, increasing potential supply.

Market Challenges

- High Production Cost: SAF currently costs significantly more — often two to five times more — than conventional jet fuel. While subsidies aim to bridge this gap, cost remains a major barrier to widespread, unmandated adoption.

- Feedstock Availability and Competition: The most commercially viable feedstocks today, such as Used Cooking Oil (UCO) and animal fats, are limited in supply and face increasing competition from the road transport sector (biodiesel). Sourcing sustainable, non-food-competing feedstocks is a critical challenge for scaling.

- Infrastructure and Logistics: Scaling production requires massive capital investment in new biorefineries and dedicated logistics infrastructure for distribution to airports worldwide.

For more information, visit the Towards Chemical and Materials website or email the team at sales@towardschemandmaterials.com| +1 804 441 9344

More Insights in Towards Chemical and Materials:

· Sustainable Materials Market: The global sustainable materials market size is estimated at USD 375.38 billion in 2025 and is predicted to increase from USD 422.08 billion in 2026 to approximately USD 1,078.35 billion by 2034, expanding at a CAGR of 12.44% from 2025 to 2034.

· Asia Pacific Sustainable Chemicals Market : According to the new market research report the Asia Pacific sustainable chemicals market size is calculated at USD 16.67 billion in 2025 and is expected to reach USD 59.74 billion by 2034, growing at a CAGR of 15.24% from 2025 to 2034.

· Sustainable Plastics Market : The global sustainable plastics market size was reached at USD 410.73 billion in 2024 and is expected to be worth around USD 1,448.23 billion by 2034, growing at a compound annual growth rate (CAGR) of 13.43% over the forecast period 2025 to 2034. Asia Pacific dominated the sustainable plastics market with a market share of 45% in 2024.

· Sustainable Adhesive Market : The global sustainable adhesive market size is calculated at USD 4.19 billion in 2025 and is forecasted to reach around USD 7.17 billion by 2034, accelerating at a CAGR of 6.15% from 2025 to 2034.

· Lubricants Market : Based on comprehensive market projections, the global lubricants market was valued at USD 144.98 Billion by the end of 2024 and is expected to increase to USD 211.53 Billion by 2034. This is a significant 3.85% increase from 2025 to 2034. In 2024, Asia Pacific led the market, achieving over 45.85% share with a revenue of USD 66.47 Billion.

Market Insight: Key Segmentation Trends

The market data from 2025 provides valuable insight into which technologies, feedstocks, and applications are dominating the initial phase of the SAF boom, and which are positioned for future growth.

By Feedstock Type

- Dominant Segment: Vegetable Oils (36.11% in 2025): The market is initially led by vegetable oils (though sustainable sourcing is a key debate), which accounted for the largest revenue share due to existing supply chains and established processing technologies.

- Fastest-Growing Segment: Waste Oils and Fats (Projected 25% Share): The future growth trajectory is clearly shifting towards waste streams. The waste oils and fats segment is expected to capture a 25% industry share during the forecast period, as they offer the highest carbon reduction potential and avoid the food-vs-fuel debate.

By Processing Technology

- Dominant Segment: Hydroprocessed Esters and Fatty Acids (HEFA) (41.23% in 2025): The HEFA pathway, which processes oils and fats, is currently the most mature and dominant technology, holding a 41.23% revenue share in 2025.

- Fastest-Growing Segment: Fischer-Tropsch (FT) Synthesis (Projected 25% Share): The Fischer-Tropsch (FT) synthesis pathway, which can convert synthesis gas from biomass, municipal waste, and power-to-liquid (PtL) sources, is expected to see dramatic growth, projecting a 25% industry share as producers look to diversify feedstock input beyond simple oils.

By Application and Distribution

- Application Dominance: Commercial Aviation (71.09% in 2025): The commercial airline sector, being the primary consumer of jet fuel and the target of most mandates, held the overwhelming majority of the market share at 71.09%.

- Future Application Growth: Private and Business Aviation (Projected 10% Share): The private and business aviation segment is expected to capture a 10% industry share, driven by high net-worth individuals and companies willing to pay a premium for immediate emissions reduction.

- Distribution Dominance: Direct Sales to Airlines (60.56% in 2025): The initial market strategy favored direct sales to airlines, which dominated with a 60.56% revenue share.

- Future Distribution Growth: Fuels Blending/Suppliers (Projected 25% Share): The fuels blending/suppliers segment is expected to grow to a 25% industry share, indicating a move towards normalizing SAF logistics within existing fuel infrastructure.

Frequently Asked Questions

What is Sustainable Aviation Fuel (SAF)

Sustainable Aviation Fuel, or SAF, is a jet fuel alternative derived from sustainable resources instead of fossil fuels. It is a certified “drop-in” fuel that can be blended with conventional jet fuel without requiring any modifications to aircraft engines, airport infrastructure, or fuel delivery systems. It can reduce lifecycle carbon emissions by up to 80 percent compared to conventional jet fuel.

Why is the Sustainable Aviation Fuel market growing so rapidly

The market is experiencing exponential growth primarily due to three factors. First, strict global regulatory mandates, such as the European Union’s ReFuelEU Aviation, require airlines to use increasing SAF percentages. Second, major airlines and large corporations have made ambitious net-zero commitments, creating a strong voluntary demand pull. Third, there is increasing technological maturity and investment in efficient production pathways like Hydroprocessed Esters and Fatty Acids (HEFA).

What are the main types of feedstock used to produce SAF

The production of SAF utilizes diverse feedstock types. Currently, the dominant feedstock segment is vegetable oils (though sustainability is a key factor), but the most significant growth is projected in the waste oils and fats segment, which includes Used Cooking Oil (UCO) and animal fats. Future feedstocks include agricultural residues, forestry waste, municipal solid waste, and even captured carbon dioxide (Power-to-Liquid).

Which production technology currently dominates the SAF market

The Hydroprocessed Esters and Fatty Acids (HEFA) processing technology currently dominates the market, holding the largest revenue share. This is because HEFA is the most mature and commercially proven pathway for converting fats and oils into certified jet fuel. However, technologies like Fischer-Tropsch (FT) synthesis, which can use a wider range of biomass and waste, are projected to show the highest growth in the coming decade.

Which region holds the largest market share for SAF

In 2025, North America dominated the Sustainable Aviation Fuel (SAF) market, accounting for the largest revenue share of over 47 percent. This dominance is driven by proactive government support, particularly the incentives and tax credits provided through the US Inflation Reduction Act, which has strongly encouraged both production and off-take agreements within the region.

Immediate Delivery Available | Buy This Premium Research Report@ https://www.towardschemandmaterials.com/checkout/6066

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Leave a Reply