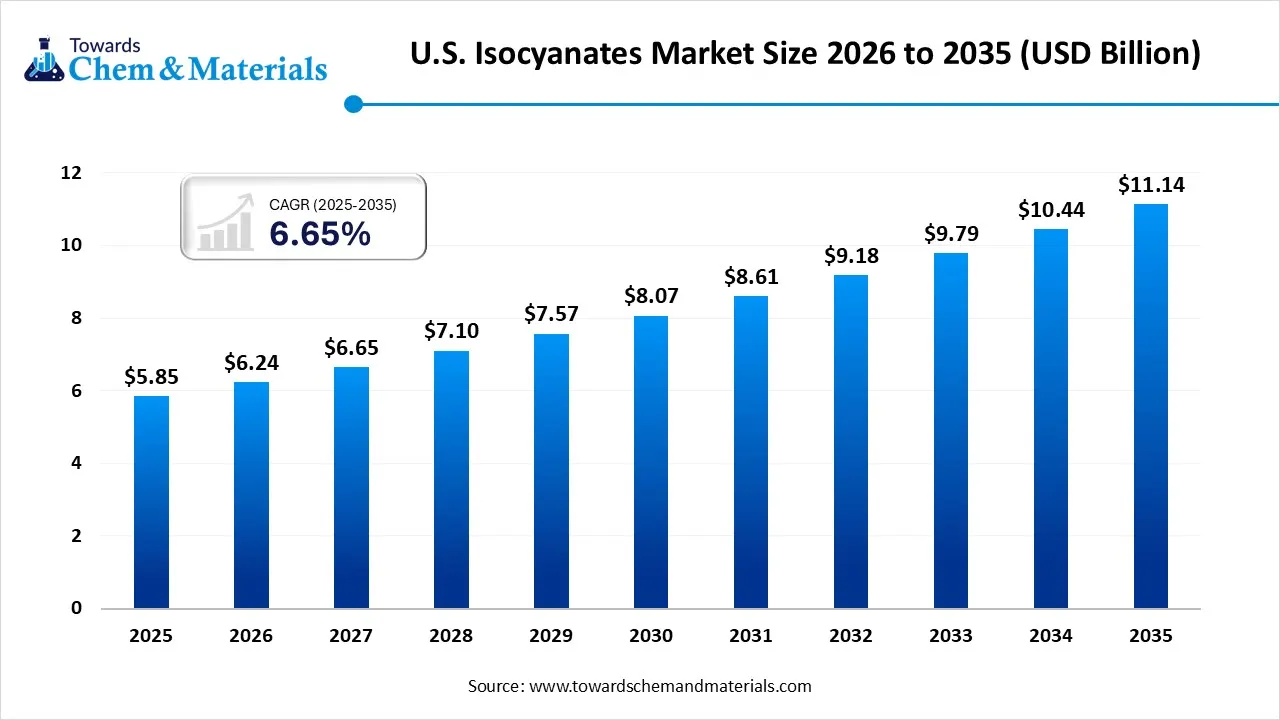

The U.S. isocyanates market continues to demonstrate steady expansion, supported by rising demand across construction, automotive, furniture, and industrial sectors. In 2025, the market was valued at USD 5.85 billion and is projected to grow from USD 6.24 billion in 2026 to USD 11.14 billion by 2035, registering a CAGR of 6.65% during 2026–2035.

The market encompasses the manufacturing, distribution, and commercialization of highly reactive NCO chemical compounds, primarily aliphatic diisocyanates, methylene diphenyl diisocyanate (MDI), and toluene diisocyanate (TDI). These chemicals serve as essential building blocks in polyurethane production, enabling the creation of rigid foams, flexible foams, elastomers, coatings, adhesives, and sealants. The industry is characterized by long-term, high-value contracts and significant investment in supply chain security.

Download a sample of this report @ https://www.towardschemandmaterials.com/download-sample/6217

Key Growth Drivers

Rising Demand for Energy-Efficient Insulation

One of the primary drivers of market growth is the increasing need for energy-efficient building insulation, particularly MDI-based rigid polyurethane foams. With infrastructure renovations accelerating and sustainability becoming central to building codes, high-performance insulation materials are in greater demand.

Additionally, the shift toward bio-based and low-emission alternatives is supporting long-term market growth, as manufacturers invest in environmentally responsible production systems.

Automotive Lightweighting and Electrification

The automotive industry plays a pivotal role in shaping market expansion. Isocyanates are critical in producing lightweight polyurethane components that enhance fuel efficiency and structural performance.

The transition to electric vehicles (EVs) further strengthens this demand. Lightweight polyurethane materials improve battery range and vehicle efficiency, accelerating the adoption of MDI- and TDI-based PU systems.

Market Highlights

By Type

-

The MDI segment dominated the market in 2025, accounting for 40.00% of total revenue share.

-

Growth is largely driven by its extensive use in automotive and construction applications, especially rigid insulation foams.

By Application

-

The flexible foam segment led the market with a 38.00% revenue share in 2025.

-

Increasing demand for lightweight seating, cushioning, and interior components in vehicles and furniture continues to fuel segment growth.

To own our research study instantly, Click here @ https://www.towardschemandmaterials.com/checkout/6217

How Cutting-Edge Technologies Are Transforming the Market

Technological advancements are reshaping the U.S. isocyanates landscape by improving sustainability, safety, and operational efficiency.

Major global producers such as BASF SE, Covestro, and Wanhua Chemical are investing heavily in:

-

Low-carbon manufacturing processes

-

Renewable energy integration

-

Bio-based feedstocks derived from plant oils and biomass

-

Digital automation for improved yield and plant safety

A significant innovation includes the development of phosgene-free production routes, such as oxidative carbonylation and CO₂-based synthesis methods. These technologies reduce environmental risks while enhancing production safety compared to traditional phosgene-based processes.

Trade Analysis: U.S. Isocyanates Import & Export Statistics

The United States remains a key exporter of isocyanates.

In 2024:

-

Exports totaled 165,602,000 kg

-

Total export value reached USD 494,236,990

Top Export Destinations:

-

Brazil – USD 97,355.06K (36,534,900 kg)

-

Mexico – USD 89,169.56K (40,406,200 kg)

-

Canada – USD 77,329.10K (31,582,000 kg)

-

Other Asia (nes) – USD 51,625.16K (3,708,150 kg)

-

Belgium – USD 42,203.64K (14,198,100 kg)

These trade flows highlight the strong regional integration of the U.S. chemical supply chain across North America and expanding access to global markets.

Market Trends Shaping Future Growth

1. Infrastructure Modernization

Infrastructure renovation projects across the United States are driving sustained demand for insulation and construction-grade polyurethane systems.

2. Production Efficiency & Digitalization

Rapid advancements in manufacturing technologies, including automation and process optimization, are improving yield, safety, and product consistency.

3. Sustainable Chemistry

The market is witnessing a structural shift toward low-VOC, non-phosgenated, and bio-based isocyanate alternatives to meet evolving environmental regulations and ESG goals.

Country Insights: United States

The U.S. isocyanates market represents a mature yet steadily growing segment of the broader chemical industry. Growth is strongly supported by:

-

Increasing vehicle production

-

Rising demand for durable and lightweight materials

-

Strong construction and insulation demand

-

Investments in advanced manufacturing technologies

The adoption of non-phosgenation processes and digital plant automation is further enhancing operational efficiency, plant safety, and product reliability across domestic production facilities.

You can place an order or ask any questions, please feel free to contact us at sales@towardschemandmaterials.com

Recent Developments

The competitive landscape continues to evolve with strategic acquisitions and product innovations:

-

In August 2025, Covestro signed an agreement with Vencorex Holding SAS to acquire two standalone production sites for HDI derivatives. This move strengthens Covestro’s aliphatics production capacity and broadens its presence in the U.S. and Asia-Pacific markets.

-

In December 2025, Pflaumer Brothers launched TERACURE® HP 47, a next-generation aliphatic crosslinking agent designed for high-performance two-component (2K) waterborne polyurethane systems. The product targets aerospace, automotive, flooring, construction, and industrial coatings sectors.

Competitive Landscape: Major Companies

The U.S. isocyanates market features a mix of global chemical giants and specialized manufacturers:

-

Asahi Kasei – Specializes in aliphatic diisocyanates (HDI), serving high-performance coating markets.

-

Aekyung Chemical – Emerging player in specialty isocyanates and polyisocyanate hardeners.

-

Covestro – Leading North American supplier of MDI and TDI.

-

Dow Inc. – Major integrated chemical producer with strong polyurethane capabilities.

-

BASF SE – Global leader in diversified chemical production.

-

Anhui Royal Chemical Co., Ltd.

-

Hefei TNJ Chemical Industry Co., Ltd.

-

Evonik Industries AG

-

KUMIAI CHEMICAL INDUSTRY CO., LTD.

-

LANXESS

-

Mitsui Chemicals Inc.

-

SABIC

-

SAPICI S.p.A.

-

Vencorex

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Explore the comprehensive statistics and insights on healthcare industry data and its associated segmentation: Get a Subscription

Leave a Reply