The global agricultural industry is undergoing a revolutionary transformation, moving from traditional, indiscriminate crop feeding to precision nourishment. At the forefront of this evolution is the Smart Fertilizers Market, a high-growth sector dedicated to delivering nutrients precisely when and where a crop needs them. This advanced category of crop nutrition is on a significant upward trajectory, fueled by the imperative to increase global food production while adhering to increasingly stringent sustainability standards.

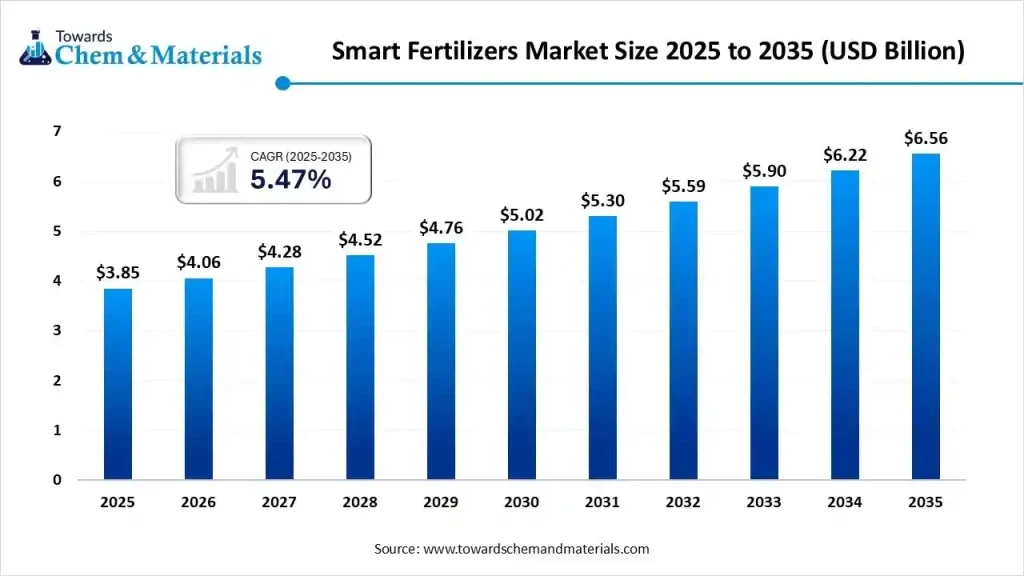

The global smart fertilizers market size was valued at USD 3.85 billion in 2025. Industry projections show this market value will grow substantially, increasing from USD 4.06 billion in 2026 and heading toward USD 6.56 billion by 2035. This represents a solid Compound Annual Growth Rate (CAGR) of 5.47% over the forecast period from 2026 to 2035. The Asia Pacific region is the market’s primary revenue driver, capturing a commanding share of over 40.75% in 2025, a reflection of the region’s massive agricultural output and its swift adoption of modern, technology-enabled farming techniques.

Get All the Details in Our Solutions –Download Sample: https://www.towardschemandmaterials.com/download-sample/6071

Key Takeaways for 2025 Market Dominance

The market’s performance in 2025 is clearly segmented, highlighting where technology adoption and commercial value are concentrated:

- Regional Leadership: The Asia Pacific region leads the market with the largest revenue share of over 40.75%. This is primarily due to the vast scale of agriculture in countries like China and India, coupled with government initiatives promoting improved nutrient use efficiency.

- Product Type: Controlled-Release Fertilizers (CRF) are the dominant product segment, securing the largest revenue share at 40.90%. Farmers favor CRFs because their reliable polymer coatings allow for a single, long-lasting application that matches nutrient supply to crop demand, which significantly reduces waste and labor costs.

- Crop Type Focus: The Grains and Cereals segment accounts for the largest revenue share at 46.11%. As foundational global food staples, these crops cover the largest cultivated area and require high, sustained nutrient inputs, making them the largest market for smart fertilizers.

- Application Method: Soil application remains the primary method, commanding 60.57% of the revenue share. This method’s dominance is due to its simplicity, farmer familiarity, and the lack of requirement for specialized or advanced fertigation equipment.

- End-Use Concentration: The Agriculture segment overwhelmingly drives the end-use market, capturing 81.13% of the revenue share, confirming that commercial food production is the core application for this technology.

Smart fertilizers are defined as research-based, advanced nutrients that utilize integrated sensors, biological triggers, or protective coatings to synchronize nutrient release with real-time variables like temperature, soil moisture, and plant demand, effectively creating a responsive crop nutrition system.

For more information, visit the Towards Chemical and Materials website or email the team at sales@towardschemandmaterials.com| +1 804 441 9344

More Insights in Towards Chemical and Materials:

· Organic Fertilizers Market: The global organic fertilizers market size is calculated at USD 13.1 billion in 2025 and is predicted to increase from USD 13.88 billion in 2026 and is projected to reach around USD 23.35 billion by 2035, The market is expanding at a CAGR of 5.95% between 2026 and 2035. North America dominated the organic fertilizers market with a market share of 5.94% the global market in 2025.

· Green Fertilizer Market : The global green fertilizer market size is calculated at USD 4.1 billion in 2025 and is predicted to increase from USD 4.38 billion in 2026 and is projected to reach around USD 7.88 billion by 2035, The market is expanding at a CAGR of 6.75% between 2026 and 2035.

· Liquid Fertilizers Market : The global liquid fertilizers market size was estimated at USD 3.19 billion in 2025 and is predicted to increase from USD 3.33 billion in 2026 and is projected to reach around USD 4.93 billion by 2035, The market is expanding at a CAGR of 4.45% between 2026 and 2035.

· Agriculture Fertilizers Market: The global agriculture fertilizers market size was estimated at USD 231.19 billion in 2025 and is predicted to increase from USD 239.77 billion in 2026 and is projected to reach around USD 332.79 billion by 2035, The market is expanding at a CAGR of 3.71% between 2026 and 2035.

Biofertilizer Market: The global biofertilizer market size is calculated at USD 3.31 billion in 2025 and is predicted to increase from USD 3.73 billion in 2026 and is projected to reach around USD 11.08 billion by 2035, The market is expanding at a CAGR of 12.85% between 2025 and 2035.

2025 Buyer Playbook: What Actually Decides Deals

Major agricultural buyers and distributors in 2025 are shifting their focus from simple price points to a comprehensive value proposition centered on performance, sustainability, and technological integration. Nutrient Use Efficiency (NUE) and digital service packages are now the key deal-closing factors.

- Sustainability Metrics and Biodegradability: Buyers are demanding third-party verification of a product’s environmental profile, moving towards suppliers who offer biodegradable polymer coatings to mitigate microplastic concerns, a trend rapidly accelerating due to anticipated new regulations. Suppliers who meet or exceed these sustainability mandates are securing premium contracts.

- Digital Integration and Agronomic Support: Deals are won by suppliers who bundle their physical products with digital farming tools. This includes providing field-specific nutrient recommendations based on AI analysis of soil data and delivering real-time, in-season nitrogen analysis apps (like Haifa Group’s Croptune™). The supplier’s ability to act as a data partner is now critical.

- Tailored Release Profiles: Buyers no longer accept generic formulas. They demand fertilizers with customized longevity and release patterns (e.g., 4-month, 6-month, or 8-month release) that precisely match the growth cycle and regional climate variability of their target crops, such as corn, rice, or high-value fruits.

Quick Comparison Matrix: Defining Smart Fertilizers

Smart fertilizers are distinguished by their mechanism and environmental impact, offering a clear advantage over traditional and slow-release products:

- Traditional Fertilizers focus on Bulk Nutrient Delivery with Rapid, Uncontrolled Release. This leads to Low Nutrient Use Efficiency (NUE) and a High Environmental Risk from nutrient leaching and runoff.

- Slow-Release Fertilizers (SRF) focus on Gradual Nutrient Delivery achieved through low-solubility chemical compounds. While offering better NUE, their release rate is often dictated solely by water solubility and lacks true responsiveness to dynamic crop needs.

- Controlled-Release Fertilizers (CRF — Smart) focus on Adaptive Nutrient Delivery via Polymer Coatings or Triggers. Their release is governed by temperature and moisture, ensuring the Highest NUE and Lowest Environmental Risk because nutrients are only released as the crop’s metabolic rate and demand increase.

- Nano-Fertilizers (Emerging Smart) focus on Ultra-Efficient Uptake using Nanoparticles or Nano-Composites. Their extremely small size allows for rapid and complete absorption, promising the most significant reduction in applied input volume.

What’s Next (2025–2030 Outlook)

The market’s future will be defined by disruptive innovation at the intersection of nanotechnology and biological science:

- Nano-Fertilizers Drive High-Efficiency Growth: The nano-fertilizers segment will experience the fastest growth, propelled by their ability to deliver nutrients using particles that are readily and completely absorbed by plants. These formulations, such as nano-urea and nano-micronutrients, drastically increase NUE, making them the future ideal for high-intensity, precision agriculture.

- The AI-Managed Fertilizer Plant: The application of Artificial Intelligence in manufacturing and logistics will become the industry standard. AI systems analyze real-time data from the field to not just recommend, but dynamically adjust the coating thickness and composition in the manufacturing plant, ensuring optimal climate-adaptive performance.

- Microbial-Triggered Release Commercializes: A key trend is the emergence of fertilizers designed to release nutrients only when triggered by beneficial microbes in the soil. This innovation perfectly synchronizes nutrient delivery with the plant’s health ecosystem, reducing reliance on conventional chemical triggers and promoting superior soil health.

- Focus on Specialty Crops: While grains and cereals dominate the volume, the fruits and vegetables segment is projected to show the fastest growth rate. This is because high-value crops require precise nutrition to maximize quality, color, and shelf life, making the premium cost of smart fertilizers an acceptable investment for growers.

Why Competition Is Intensifying

Competition is escalating because smart fertilizers represent the premium, high-margin future of the crop nutrition industry, offering a direct solution to global regulatory and environmental pressures.

- The Race for Proprietary Coating Technology: The core competitive advantage lies in the patented polymer and bio-polymer coating technologies that control the release mechanism. Companies are investing heavily in R&D to develop cheaper, more durable, and fully biodegradable coatings before regulators impose strict bans on non-degradable microplastics.

- Regulatory Push for Efficiency: Government bodies are setting aggressive targets for Nutrient Use Efficiency (NUE) and reducing nitrous oxide emissions, making smart fertilizers mandatory for compliance and access to subsidies in key agricultural markets. This regulatory tailwind forces all major players to rapidly pivot their portfolios.

- Vertical Integration and Digital Lock-in: Conglomerates are intensifying competition by vertically integrating smart fertilizer products with their expansive retail networks, digital platforms, and seed/crop protection businesses. They aim to lock in customers by providing a unified, data-driven farming solution, making it difficult for pure-play manufacturers to compete on distribution alone.

How These Leaders Compete

The market leaders compete by leveraging their core strengths in raw material supply, specialty technology, and global reach.

Nutrien Ltd (Canada)

Nutrien, the world’s largest provider of crop inputs and services, competes through scale and retail dominance. They leverage their vast potash and nitrogen production assets to offer proprietary smart fertilizers, bundling them with their expansive Retail network and digital agronomic platforms to provide a complete, end-to-end efficiency solution for farmers. Their focus is on high volume and seamless integration into the grower’s operation.

Yara International ASA (Norway)

Yara positions itself as the sustainability and precision leader. They compete by focusing on a premium portfolio of specialty nitrogen and micronutrient-based smart fertilizers, backed by advanced digital tools that help farmers meet emission reduction targets. Their strategy emphasizes high-tech, low-carbon solutions and global regulatory compliance.

The Mosaic Company (United States)

As a major global producer of phosphate and potash, Mosaic integrates smart coatings and specialized formulations into their core P&K products. Their competitive strategy focuses on delivering high-performance, tailored nutrient combinations for large-scale production of primary crops, primarily utilizing their strong presence in North and South American markets.

CF Industries Holdings, Inc (United States)

Specializing in nitrogen products, CF Industries competes by focusing on Enhanced Efficiency Fertilizers (EEFs) that incorporate urease and nitrification inhibitors. Their long-term strategy includes heavy investment in low-carbon or green ammonia production, positioning them to supply the sustainable, next-generation nitrogen feedstock required for future smart fertilizers.

EuroChem Group AG

EuroChem competes by offering a broad, integrated portfolio across all primary nutrients (NPK). Their strategy involves aggressive global expansion, particularly in emerging markets, with a focus on their own line of high-quality Enhanced Efficiency Fertilizers to capture market share through comprehensive product availability.

K+S AG

A global leader in potash and magnesium products, K+S competes by using its strong mining assets to develop specialty smart fertilizers. They focus on formulations that improve crop quality and stress tolerance, utilizing their expertise in essential secondary nutrients to differentiate their smart products, particularly for high-value applications.

ICL Group Ltd.

ICL is a pioneer in specialty mineral and phosphate products. They compete on advanced technology in Controlled-Release Fertilizers (CRF), notably with their Osmocote product line, and are leaders in water-soluble fertilizers for fertigation. Their strategy involves continuous innovation, like the Optimized Trace Element Availability (OTEA) mechanism, and securing high-value contracts for specialty crops.

Coromandel International Limited

A dominant force in the Indian market, Coromandel leverages its extensive distribution network and deep understanding of local soil and crop requirements. They compete by offering regionally localized and micronutrient-fortified smart fertilizers, which are essential for addressing specific soil deficiencies in the high-volume grains and cereals market of South Asia.

BASF SE and Bayer CropScience AG

These agrochemical giants compete by integrating smart fertilizers into a comprehensive bundled solution that includes seeds, crop protection chemicals, and digital advisory services. Their strength lies in providing farmers with a unified system for yield and health management, where the smart fertilizer acts as a component of a much larger, data-driven prescription.

COMPO EXPERT GmbH

COMPO EXPERT focuses intensely on specialty fertilizers and biostimulants, targeting the high-value horticulture, ornamental, and turf segments. They compete on technical expertise and product purity, offering tailored solutions that maximize quality and performance for non-commodity applications where precision and quality are paramount.

Haifa Group

Haifa Group is a global expert in Controlled Release Fertilizers (CRFs) and water-soluble plant nutrition, utilizing proprietary coating technology like Multicote™ Agri. They compete by providing premium products optimized for advanced irrigation systems and high-tech agriculture, backed by digital tools like the Croptune™ app for real-time nitrogen analysis.

Frequently Asked Questions

1. How does a smart fertilizer differ structurally from a traditional fertilizer?

A smart fertilizer, particularly a Controlled-Release Fertilizer (CRF), differs structurally by having a nutrient core encased in a semipermeable polymer coating or membrane. This coating is the key to its “smart” functionality, as it controls the rate at which water penetrates and dissolves the nutrient, which in turn regulates the nutrient release into the soil. Traditional fertilizers, conversely, are simple chemical compounds that dissolve rapidly and uncontrollably upon contact with water.

2. What role does artificial intelligence play in the smart fertilizers market?

Artificial intelligence (AI) is transforming the smart fertilizers market by moving nutrient management from reactive to predictive. AI algorithms analyze massive datasets from soil sensors, weather satellite imagery, and historical yield data to forecast a crop’s precise nutrient need at specific growth stages. Manufacturers then use this AI-driven insight to tailor the polymer coating thickness and chemical makeup of their smart fertilizers, ensuring the release profile perfectly matches the predicted plant demand, thereby minimizing waste.

3. Which emerging product segment is expected to drive the fastest growth?

The Nano-Fertilizers segment is expected to exhibit the fastest growth within the smart fertilizers market. Nano-fertilizers utilize nutrient particles in the 1–100 nanometer size range. This ultra-small size dramatically enhances a plant’s ability to absorb the nutrients, leading to a much higher Nutrient Use Efficiency (NUE) and requiring significantly lower application volumes compared to even CRFs. This efficiency makes them an ideal solution for resource-constrained precision agriculture.

4. Why is the Asia Pacific region the dominant market for smart fertilizers?

The Asia Pacific region dominates the market due to a combination of scale, population density, and government policy. The sheer volume of agriculture required to feed the enormous populations in countries like China and India makes efficient nutrient use crucial. Furthermore, regional governments are actively promoting the shift to modern farming practices and providing subsidies for specialty coatings and precision products to combat the severe environmental degradation caused by excessive use of traditional, polluting fertilizers.

5. What are the major non-degradable material concerns facing the CRF segment?

The major concern facing the Controlled-Release Fertilizers (CRF) segment is the environmental impact of the polymer coatings, which are often non-biodegradable plastics. As these coatings break down slowly into microplastics, they accumulate in cultivated soil, raising significant environmental and regulatory concerns, mirroring global efforts to curb single-use plastics. In response, leading companies are aggressively researching and commercializing new, fully biodegradable coatings made from materials like starch or cellulose, anticipating future regulatory bans.

Immediate Delivery Available | Buy This Premium Research Report@ https://www.towardschemandmaterials.com/price/5638

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Leave a Reply