Market Overview: Europe Adhesives and Sealants

The European adhesives and sealants market is a vital component of the continent’s industrial landscape, serving as a critical enabler for major sectors such as construction, automotive, electronics, and packaging. Its significance is underscored by the ongoing industrial shift towards lightweighting, sustainability, and high-performance material solutions. These materials are no longer just basic fasteners; they are now engineered components that improve structural integrity, reduce weight, and enhance energy efficiency in modern applications.

Download Sample here : https://www.towardschemandmaterials.com/download-sample/6043

Current Market Size and Future Projections

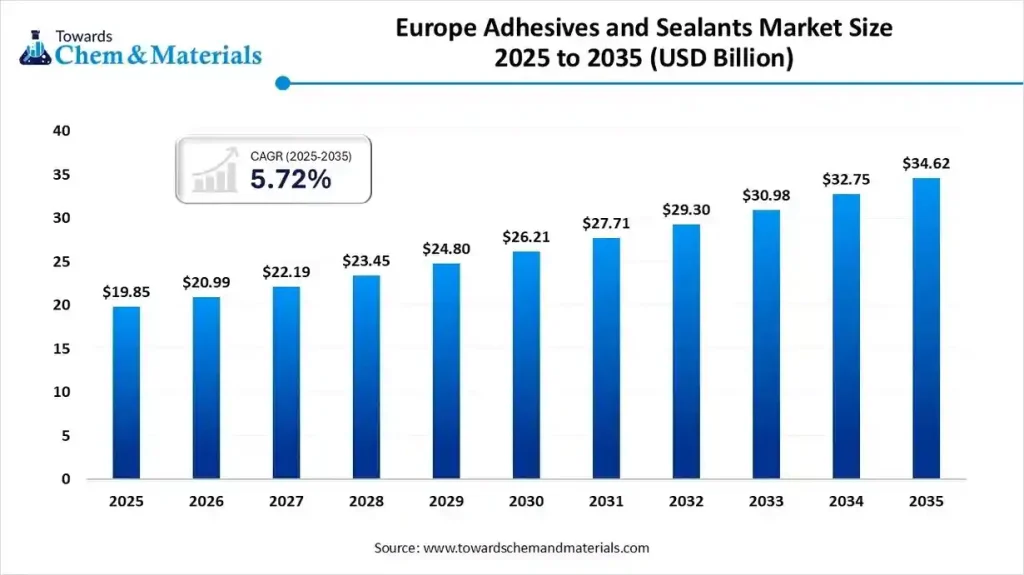

The Europe adhesives and sealants market size is calculated at USD 19.85 billion in 2025. It is poised for substantial growth, projected to increase from USD 20.99 billion in 2026 and reach approximately USD 34.62 billion by 2035.

This impressive expansion is driven by a Compound Annual Growth Rate (CAGR) of 5.72% over the forecast period from 2026 to 2035.

Market Dynamics: Drivers, Trends, and Challenges

The trajectory of the Europe adhesives and sealants market is shaped by a confluence of powerful drivers, technological advancements, and stringent regulatory pressures. Understanding these dynamics is key to grasping the market’s future.

Key Market Drivers

- Growing Construction Industry: The largest consumer of adhesives and sealants, the construction sector is fueled by increasing urbanization, residential renovation, commercial projects, and the critical need for infrastructure repair and retrofitting across aging European assets. The focus on energy-efficient building standards and modern, modular construction techniques heavily relies on advanced sealing and bonding solutions.

- Automotive Sector’s Shift to Lightweighting: The transition to electric vehicles (EVs) and the persistent drive for fuel efficiency in conventional vehicles necessitate the replacement of traditional mechanical fasteners with lightweight, high-strength adhesives. These solutions are essential for battery assembly, structural bonding of composite materials, and reducing overall vehicle weight, thereby extending EV range and improving performance.

- Demand for High-Performance Applications: Across aerospace, electronics, and medical devices, there is a rising need for specialized adhesives offering conductivity, flexibility, rapid curing times, and superior thermal and chemical resistance. This push for high-specification materials is accelerating innovation.

Pivotal Market Trends

- Sustainability and Environmental Regulations: This is arguably the most influential trend. Stringent EU regulations, particularly those stemming from REACH and local initiatives like Germany’s AgBB Scheme for VOC emissions, are forcing a massive shift. The demand for eco-friendly, low-VOC (Volatile Organic Compound), solvent-free, water-borne systems, and bio-based adhesives is at an all-time high, fundamentally redefining product formulations.

- Technological Advancement in Smart Materials: Ongoing innovation is focused on developing “smart adhesives” that can respond to environmental changes, along with advanced systems offering conductivity, flexibility for electronics (IoT, 5G, wearables), and rapid curing technologies.

- Aerospace and Renewable Energy Growth: The increasing production of lightweight, fuel-efficient aircraft and the expansion of renewable energy technologies, such as wind turbines and solar panels, require high-performance adhesives and sealants for assembly, structural integrity, and weather resistance.

- Digitalization and Automation: Manufacturers are integrating Artificial Intelligence (AI) and automation into operations and product development to improve efficiency, material precision, and quality control.

Trade Analysis: Import & Export Statistics

Europe maintains a complex trade profile, both exporting and importing significant volumes.

- Global Adhesives and Sealants Exports: Globally, the world exported 5,649 shipments of adhesives and sealants from June 2024 to May 2025. The United States leads with 4,762 shipments, followed by China (4,111), and Japan (1,695).

- EU Sealant Exports: From March 2024 to February 2025 (TTM), the EU exported 11 shipments of Sealant, showing a 38% growth compared to the preceding year. Major EU export destinations for sealants include Vietnam, Ukraine, and Kazakhstan.

Regulatory Landscape: The EU’s Impact

The regulatory framework is a major market driver, pushing innovation towards safer and more sustainable products.

- REACH Regulation (EC №1907/2006): This is the cornerstone of EU chemicals policy, driving the reformulation of raw materials like isocyanates, solvents, and plasticizers to ensure chemical safety and restrict hazardous substances.

- CLP Regulation (EC №1272/2008): Focuses on the classification, labeling, and packaging of substances and mixtures, ensuring clear hazard communication.

- National Specificity: Countries like Germany enforce strict indoor air quality standards through the AgBB Scheme, which impacts adhesive formulations for construction. France mandates VOC Emission Labelling on construction adhesives, promoting low-emission products. The UK’s post-Brexit UK REACH regulation adds a layer of complexity by requiring separate chemical registration.

For more information, visit the Towards Chemical and Materials website or email the team at sales@towardschemandmaterials.com| +1 804 441 9344

More Insights in Towards Chemical and Materials:

- Sustainable Adhesive Market : The global sustainable adhesive market size is calculated at USD 4.19 billion in 2025 and is forecasted to reach around USD 7.17 billion by 2034, accelerating at a CAGR of 6.15% from 2025 to 2034.

- Floor Adhesives Market: The global floor adhesives market size was estimated at USD 9.69 billion in 2024 and is predicted to increase from USD 10.25 billion in 2025 to approximately USD 17.1 billion by 2034, expanding at a CAGR of 5.80% from 2025 to 2034.

- Water-Based Adhesives Market : The global water-based adhesives market size is calculated at USD 42.42 billion in 2025 and is forecasted to reach around USD 96.40 billion by 2034, accelerating at a CAGR of 9.55% from 2025 to 2034.

- Electronic Adhesives Market : The global electronic adhesives market size is calculated at USD 6.32 billion in 2025 and is forecasted to reach around USD 14.01 billion by 2034, accelerating at a CAGR of 9.24% from 2025 to 2034.

- Plastic Adhesives Market : The plastic adhesives market size was estimated at USD 17.65 billion in 2024 and is predicted to increase from USD 19.22 billion in 2025 to approximately USD 41.44 billion by 2034, expanding at a CAGR of 8.91% from 2025 to 2034. The North America leads the market due to strong infrastructure growth, while Asia Pacific is the fastest-growing region, fueled by affordable housing and large-scale construction projects. Growing environmental concerns and the need for long-lasting, eco-friendly paints further boost market demand.

- Liquid Adhesives Market : The global liquid adhesives market size was estimated at USD 42.15 billion in 2024 and is predicted to increase from USD 43.56 billion in 2025 to approximately USD 58.60 billion by 2034, expanding at a CAGR of 3.35% from 2025 to 2034.

- Rubber-Repair Adhesives Market : The global rubber-repair adhesives market size was estimated at USD 1.45 billion in 2024 and is predicted to increase from USD 1.50 billion in 2025 to approximately USD 2.08 billion by 2034, expanding at a CAGR of 3.68% from 2025 to 2034.

- Adhesives Market : The global adhesives market size is calculated at USD 68.95 billion in 2024, grew to USD 73.16 billion in 2025 and is predicted to hit around USD 124.77 billion by 2034, expanding at healthy CAGR of 6.11% between 2025 and 2034.

- Adhesives and Sealants Market : The global adhesives and sealants market is projected to grow from USD 77.25 billion in 2025 to USD 139.79 billion by 2035, growing at a compound annual growth rate (CAGR) of 6.11% over the forecast period from 2026 to 2035. Key players in the adhesives and sealants market are 3M Company, Ashland Inc., Avery Denison Corporation, H.B. Fuller, Henkel AG, Sika AG, Pidilite Industries, Huntsman, Wacker Chemie AG, RPM International Inc., Dow, Kuraray Co., Ltd.

Segmental Insights

Resin Insights

Which Adhesive Resin Segment Dominated The Europe Adhesives And Sealants Market In 2024?

The acrylic resins segment dominated the Europe adhesives and sealants market with a share of 39.19% in 2025. Acrylic resin–based adhesives are widely used in Europe due to their strong bonding properties, excellent weather resistance, and long-term durability.

These adhesives are extensively applied in various sectors where UV resistance and transparency are critical. Additionally, low-volatile organic compound formulations are increasing in adoption as European regulations push for environmentally friendly and sustainable adhesive solutions.

The epoxy resins segment expects significant growth in the market during the forecast period. Epoxy-based adhesives offer superior mechanical strength, chemical resistance, and thermal stability, making them ideal for structural bonding applications across aerospace, construction, and heavy industries. Their strong adhesion to metals and composites makes them critical in high-performance applications where durability and load-bearing performance are essential.

The polyurethane segment has seen notable growth in the market. Polyurethane adhesives are known for their flexibility, impact resistance, and ability to bond dissimilar materials. Their ability to absorb vibrations and withstand temperature variations supports increasing demand. Growth in green building projects and modular construction across Europe is further driving polyurethane adhesive consumption.

Technology Insights

How Did the Reactive Adhesives Segment Dominated The Europe Adhesives And Sealants Market In 2024?

The reactive adhesives segment dominated the market with a share of 44.32% in 2025. Reactive adhesives, such as moisture-curing polyurethanes and epoxies, dominate high-performance applications where strong and permanent bonding is required. Increasing use of lightweight materials and composites in transportation is pushing demand for reactive adhesives. Their superior bonding strength and long service life make them essential in modern industrial processes.

The hot melt adhesives segment expects significant growth in the Europe adhesives and sealants market during the forecast period. Hot melt adhesives are gaining popularity due to their fast setting time, solvent-free nature, and recyclability advantages. They are widely used in packaging, labelling, woodworking, and hygiene products. The rising preference for environmentally sustainable and energy-efficient manufacturing processes also boosts the adoption of hot melt technologies.

The solvent-borne adhesives segment has seen notable growth in the market. Despite tightening environmental regulations, solvent-borne adhesives continue to have strong demand in applications requiring high initial tack and strong bonding, such as automotive trims and industrial laminates. This segment remains relevant in legacy applications and in industries where performance requirements outweigh environmental concerns.

End-User Industry Insights

Which End-User Industry Segment Dominated The Europe Adhesives And Sealants Market In 2024?

The building and construction segment dominated the market with a share of 47.22% in 2025. The construction industry is the largest consumer of adhesives and sealants in Europe, driven by demand from residential renovation, commercial construction, and infrastructure projects. Growing urbanisation, energy-efficient building requirements, and increasing retrofitting activities across ageing European infrastructure are major growth drivers for this segment.

The aerospace segment expects significant growth in the Europe adhesives and sealants market during the forecast period. In the aerospace industry, adhesives and sealants are essential for bonding lightweight composites, sealing aircraft fuselage sections, and improving fuel efficiency by reducing mechanical fasteners. Increasing production of commercial aircraft and investments in defence fleets are contributing significantly to the growth of this segment.

Country Insights

- Germany 🇩🇪: The largest market in Europe, underpinned by its powerhouse automotive, industrial manufacturing, and electric vehicle production sectors. German manufacturers lead in developing high-performance, sustainable, and low-emission adhesives to comply with the nation’s stringent environmental codes.

- United Kingdom (UK) 🇬🇧: Driven by infrastructure projects, residential construction, and a strong aerospace manufacturing base. Post-Brexit supply chain shifts are encouraging domestic adhesive production, while a focus on green construction accelerates the move to eco-friendly solutions.

- France 🇫🇷: Supported by its significant aerospace and automotive industries, alongside major public investments in sustainable urban development and renovation. This creates strong demand for structural and specialized bonding materials.

Top Companies in the Europe Adhesives and Sealants Market

The European market is highly competitive, dominated by global giants with diversified portfolios and intense focus on R&D for sustainable and high-performance solutions.

Henkel AG & Co. KGaA

- About: Headquartered in Düsseldorf, Germany, Henkel is a true global leader, holding a dominant position in the adhesives, sealants, and functional coatings market. The company operates globally across three business units: Adhesive Technologies, Beauty Care, and Laundry & Home Care. The Adhesive Technologies division is the clear market leader worldwide.

- Key Products:

- LOCTITE: Adhesives, sealants, and coatings for industrial manufacturing and repair (e.g., threadlockers, gasketing, instant adhesives).

- TEROSON: Sealing, bonding, coating, and reinforcing solutions for automotive body repair and assembly (OEM and MRO).

- BONDERITE: Process solutions for surface treatment and functional coatings.

- Technomelt: Hot melt adhesives for packaging, hygiene, and graphic arts.

- Market Cap (Approximate): Over €30 billion (as of late 2025/early 2026, subject to constant market fluctuation).

Sika AG

- About: A Swiss specialty chemicals company founded in 1910, Sika is a key player in the construction and industrial markets. Sika’s core competencies — sealing, bonding, damping, reinforcing, and protecting — are critical to the market’s value chain. Sika has expanded its market presence dramatically through key acquisitions, notably the MBCC Group.

- Key Products:

- Sikaflex: High-performance polyurethane and hybrid sealants for construction and industrial assembly.

- SikaBond: Adhesives for construction, flooring, and industrial use.

- Sika ViscoCrete: Concrete admixtures (enhancing durability and workability).

- Sikadur: Structural bonding agents and repair materials (epoxy-based).

- Market Cap (Approximate): Over CHF 40 billion (as of late 2025/early 2026, subject to constant market fluctuation).

Arkema (Bostik)

- About: Arkema is a French multinational chemicals company that strategically spun off its specialty chemicals division. Its adhesives business operates globally under the Bostik brand, focusing on smart adhesives and sealants for consumer, construction, and industrial markets. Bostik is known for its focus on sustainable and low-VOC solutions.

- Key Products:

- Bostik Smart Adhesives: Solutions for flexible packaging, hygiene products (diapers), and nonwovens.

- Simson: Specialized sealants and adhesives for transportation and marine applications.

- Adhesives for flooring, tiling, and insulation in the construction sector.

- Market Cap (Approximate): Arkema Group’s market cap is around €7–8 billion (as of late 2025/early 2026, subject to constant market fluctuation).

H.B. Fuller Company

- About: A major global adhesives company headquartered in the U.S. with significant operations across Europe. H.B. Fuller is highly focused on specialty and engineered adhesives for packaging, hygiene, electronics, and automotive industries, with a strong commitment to bio-based and sustainable formulations.

- Key Products:

- Cyberbond: High-performance industrial adhesives, including cyanoacrylates.

- Clarity: Adhesives for the packaging industry.

- Solutions for battery assembly in electric vehicles (EVs).

- Hot melt and water-based adhesives for hygiene and converting.

- Market Cap (Approximate): Around $4 billion (as of late 2025/early 2026, subject to constant market fluctuation).

RPM International Inc.

- About: A U.S.-based holding company with a diverse portfolio of specialty coatings, sealants, and building materials. RPM operates in Europe through brands like Tremco and illbruck, focusing heavily on waterproofing, high-performance sealants, and building envelope solutions for commercial and residential construction.

- Key Products:

- Tremco: Sealants, waterproofing systems, and passive fire control.

- illbruck: Sealants and foams for window and façade sealing in construction.

- Industrial floor coatings and corrosion control products.

- Market Cap (Approximate): Over $12 billion (as of late 2025/early 2026, subject to constant market fluctuation).

Soudal Group

- About: A Belgian-based, independent, family-owned company and one of Europe’s largest manufacturers of sealants, adhesives, and polyurethane foams. Soudal serves the professional construction, industrial assembly, and DIY markets with a comprehensive product range.

- Key Products:

- Polyurethane (PU) Foams for insulation and gap filling.

- Silicone and Hybrid Sealants for construction and sanitary applications.

- Adhesives for flooring and general assembly.

- Market Cap (Approximate): As a privately-held company, a public market capitalization figure is not available.

Wacker Chemie AG

- About: A German-based global chemical company focused on high-tech specialty products, including silicones and polymers, which are crucial raw materials and finished products in the adhesives and sealants industry. WACKER is actively investing in new capacity for sustainable hybrid polymers.

- Key Products:

- SILICONE Elastomers: For high-performance sealants in construction and industrial applications.

- VINNAPAS: Polymer binders and dispersible polymer powders for construction applications (e.g., tile adhesives, self-leveling compounds).

- GENIOSIL STP-E: Silane-terminated polymers for tin-free, low-emission adhesives and sealants.

- Market Cap (Approximate): Around €6–7 billion (as of late 2025/early 2026, subject to constant market fluctuation).

Frequently Asked Questions (FAQs)

1. What is the projected market value of the Europe adhesives and sealants industry by 2035

The Europe adhesives and sealants market is projected to reach approximately USD 34.62 billion by 2035. This growth is driven by a Compound Annual Growth Rate (CAGR) of 5.72% over the forecast period from 2026 to 2035, reflecting sustained demand from construction, automotive, and specialized industrial sectors.

2. Which adhesive resin type holds the largest share in the European market

The acrylic resins segment accounted for the largest revenue share in the Europe adhesives and sealants market, holding 39.19% in 2025. This dominance is attributed to acrylics’ excellent bonding properties, weather resistance, and their extensive use in low-VOC and water-borne formulations, which align with strict European environmental regulations.

3. What is the primary driver of growth in the European automotive adhesives sector

The primary driver is the push for vehicle lightweighting and the accelerating adoption of electric vehicles (EVs). Adhesives and sealants are critical for structural bonding of lightweight composites, improving battery safety and performance through precise assembly, and replacing heavy mechanical fasteners to enhance fuel efficiency and EV range.

4. How does EU regulation impact the development of new adhesive products

European regulations, primarily the REACH Regulation and country-specific standards like Germany’s AgBB Scheme, significantly impact product development by mandating the reduction or elimination of hazardous substances. This forces manufacturers to invest in R&D for sustainable, low-VOC (Volatile Organic Compound), solvent-free, and bio-based adhesive and sealant systems to ensure compliance and gain market acceptance.

5. Which end-user industry is the largest consumer of adhesives and sealants in Europe

The building and construction segment is the largest end-user industry, dominating the market with a revenue share of 47.22% in 2025. This substantial consumption is fueled by ongoing renovation activities, urbanization, commercial construction, and the demand for materials that meet high standards for energy efficiency and weatherproofing.

Immediate Delivery Available | Buy This Premium Research Report@ https://www.towardschemandmaterials.com/price/5638

About Us

Towards Chemical and Materials is a leading global consulting firm specializing in providing comprehensive and strategic research solutions across the chemical and materials industries. With a highly skilled and experienced consultant team, we offer a wide range of services designed to empower businesses with valuable insights and actionable recommendations.

Our Trusted Data Partners

Precedence Research | Statifacts | Towards Packaging | Towards Healthcare | Towards Food and Beverages | Towards Chemical and Materials | Towards Consumer Goods | Nova One Advisor |

For Latest Update Follow Us: https://www.linkedin.com/company/towards-chem-and-materials/

USA: +1 804 441 9344

APAC: +61 485 981 310 or +91 87933 22019

Europe: +44 7383 092 044

Leave a Reply