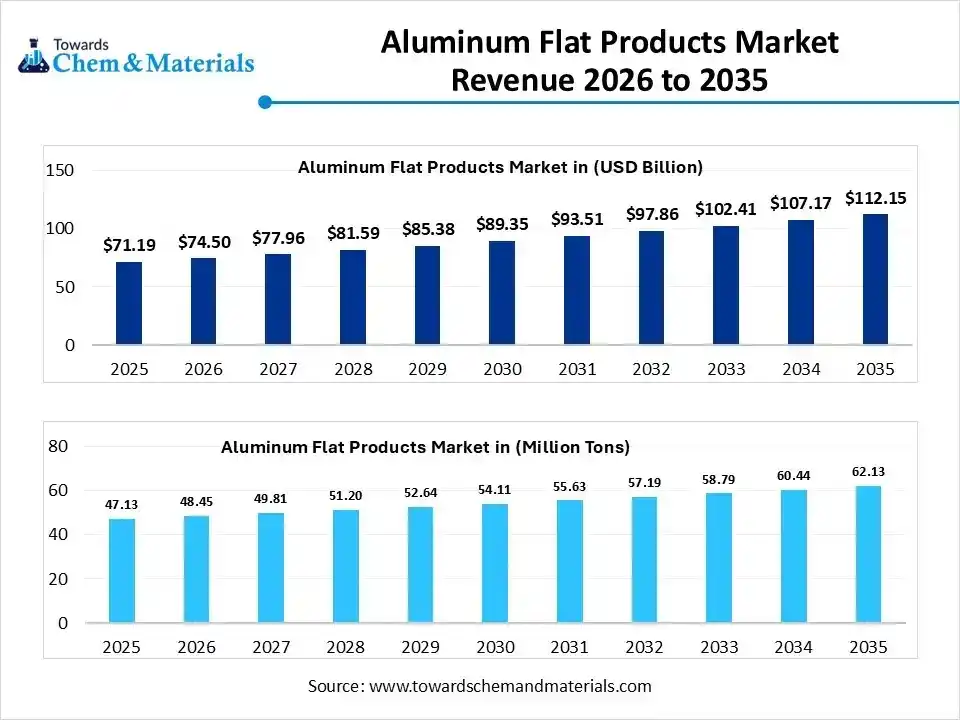

The global aluminum flat products market is entering a transformative era, defined by the dual forces of rapid industrialization and a global shift toward decarbonization. As we look toward the 2026-2035 forecast period, aluminum’s role as a “green metal” has never been more critical. Valued at USD 74.50 billion in 2026, the market is on a trajectory to reach USD 112.15 billion by 2035, growing at a steady compound annual growth rate (CAGR) of 4.65%.

This comprehensive analysis explores the market dynamics, technological shifts, and the competitive landscape of the industry’s most influential players.

Market Overview: The Aluminum Renaissance

The demand for aluminum flat products—encompassing sheets, plates, foils, and circles—is surging. In terms of volume, the market is projected to expand from 47.13 million tons in 2025 to 62.13 million tons by 2035.

Regional Powerhouses

-

Asia Pacific: Currently the undisputed leader, accounting for a 48.6% volume share in 2025. Driven by India’s infrastructure boom and China’s manufacturing prowess, this region remains the center of gravity for production and consumption.

-

North America: Projected to grow at a CAGR of 3.86%, fueled by a massive pivot toward Electric Vehicles (EVs) and sustainable packaging.

-

Europe: Holding a 20.11% volume share in 2025, the European market is at the forefront of “Circular Economy” initiatives, focusing heavily on closed-loop recycling.

Market Dynamics: Drivers and Challenges

Key Growth Drivers

-

Lightweighting in Automotive: To meet stringent fuel efficiency and emission standards, automakers are replacing steel with aluminum. The shift toward EVs is particularly beneficial, as aluminum’s high strength-to-weight ratio helps extend battery range.

-

Packaging Sustainability: The “war on plastic” has redirected consumer brands toward infinitely recyclable aluminum cans and foils. The packaging segment led the market in 2025 with a 39.4% revenue volume share.

-

Infrastructure and Construction: Rapid urbanization in emerging economies requires corrosion-resistant materials for roofing, cladding, and structural components.

Market Challenges

-

Energy Volatility: Primary aluminum smelting is energy-intensive. Fluctuations in energy prices can impact the operating margins of integrated producers.

-

Regulatory Pressures: Increasing carbon taxes (such as the EU’s CBAM) are forcing manufacturers to invest heavily in low-carbon production technologies.

In-Depth Market Segment Insights

By Product Type

-

Sheets [0.2 – 0.6 mm]: This segment dominated in 2025 with a 29.11% volume share. Its versatility across automotive body panels and building facades makes it a market staple.

-

Plates [> 6 mm]: The fastest-growing segment (4.17% CAGR), driven by high-stress applications in aerospace, defense, and maritime engineering.

By Processing Method

-

Cold Rolling: Currently leads with a 58.8% share due to its ability to provide superior surface finish and dimensional precision.

-

Continuous Casting: This is the segment to watch for the fastest growth, as it offers significant energy savings and higher throughput compared to traditional methods.

By Alloy Series

-

3xxx Series: The market leader in 2025 (34.2% share), favored for its excellent formability and corrosion resistance in packaging.

-

6xxx Series: Expected to witness the fastest growth due to its increasing use in high-strength structural components for the automotive and aerospace industries.

Technological Shifts and Startup Ecosystem

The industry is no longer just about rolling metal; it is about digital and chemical evolution.

-

AI and Digital Twins: Manufacturers are using simulation technologies to optimize rolling processes and reduce waste.

-

Low-Carbon Smelting: Technologies like ELYSIS (carbon-free smelting) are moving from labs to industrial-scale production.

-

Startup Innovation: New players are focusing on advanced scrap sorting using AI and laser spectroscopy, allowing for higher-quality secondary aluminum that rivals primary metal.

Competitive Landscape: Top Companies Analysis

Top key players in the aluminum flat products market are Alcoa Corporation, Norsk Hydro ASA, Constellium SE, Novelis Inc., Arconic Corporation, UACJ Corporation, United Company RUSAL, Speira GmbH -Global Forecast 2026 To 2035.

More Insights in Towards Chemical and Materials:

Sustainable Adhesive Market : The global sustainable adhesive market size is calculated at USD 4.19 billion in 2025 and is forecasted to reach around USD 7.17 billion by 2034, accelerating at a CAGR of 6.15% from 2025 to 2034.

Floor Adhesives Market: The global floor adhesives market size was estimated at USD 9.69 billion in 2024 and is predicted to increase from USD 10.25 billion in 2025 to approximately USD 17.1 billion by 2034, expanding at a CAGR of 5.80% from 2025 to 2034.

Water-Based Adhesives Market : The global water-based adhesives market size is calculated at USD 42.42 billion in 2025 and is forecasted to reach around USD 96.40 billion by 2034, accelerating at a CAGR of 9.55% from 2025 to 2034.

Electronic Adhesives Market : The global electronic adhesives market size is calculated at USD 6.32 billion in 2025 and is forecasted to reach around USD 14.01 billion by 2034, accelerating at a CAGR of 9.24% from 2025 to 2034.

Plastic Adhesives Market : The plastic adhesives market size was estimated at USD 17.65 billion in 2024 and is predicted to increase from USD 19.22 billion in 2025 to approximately USD 41.44 billion by 2034, expanding at a CAGR of 8.91% from 2025 to 2034. The North America leads the market due to strong infrastructure growth, while Asia Pacific is the fastest-growing region, fueled by affordable housing and large-scale construction projects. Growing environmental concerns and the need for long-lasting, eco-friendly paints further boost market demand.

Liquid Adhesives Market : The global liquid adhesives market size was estimated at USD 42.15 billion in 2024 and is predicted to increase from USD 43.56 billion in 2025 to approximately USD 58.60 billion by 2034, expanding at a CAGR of 3.35% from 2025 to 2034.

Rubber-Repair Adhesives Market : The global rubber-repair adhesives market size was estimated at USD 1.45 billion in 2024 and is predicted to increase from USD 1.50 billion in 2025 to approximately USD 2.08 billion by 2034, expanding at a CAGR of 3.68% from 2025 to 2034.

Adhesives Market : The global adhesives market size is calculated at USD 68.95 billion in 2024, grew to USD 73.16 billion in 2025 and is predicted to hit around USD 124.77 billion by 2034, expanding at healthy CAGR of 6.11% between 2025 and 2034.

Adhesives and Sealants Market : The global adhesives and sealants market is projected to grow from USD 77.25 billion in 2025 to USD 139.79 billion by 2035, growing at a compound annual growth rate (CAGR) of 6.11% over the forecast period from 2026 to 2035. Key players in the adhesives and sealants market are 3M Company, Ashland Inc., Avery Denison Corporation, H.B. Fuller, Henkel AG, Sika AG, Pidilite Industries, Huntsman, Wacker Chemie AG, RPM International Inc., Dow, Kuraray Co., Ltd.

Frequently Asked Questions (FAQs)

1. What is the expected market size of aluminum flat products by 2035 The global market is projected to reach USD 112.15 billion by 2035, growing from USD 74.50 billion in 2026.

2. Which industry is the largest consumer of aluminum flat products The packaging industry is currently the largest consumer, holding a 39.4% share in 2025. However, the automotive and transportation sector is expected to be the fastest-growing end-user during the forecast period.

3. Why is the Asia Pacific region dominating the market The dominance of the Asia Pacific is due to high production capacities in China and India, coupled with massive investments in infrastructure and a rapidly growing automotive manufacturing base.

4. What are the main benefits of using aluminum over steel in vehicles Aluminum is much lighter than steel, which improves fuel efficiency and extends the range of electric vehicles. It also offers excellent corrosion resistance and is 100% recyclable without losing its properties.

5. What is the difference between cold rolling and hot rolling Hot rolling involves processing the metal at high temperatures, making it easier to shape. Cold rolling is done at or near room temperature, which results in a stronger product with a more precise and smoother surface finish.

Leave a Reply